AN ECONOMIC EXPLANATION OF THE NATIONALIZATION OF ELECTORAL POLITICS

n?u=RePEc:gov:wpaper:1602&r=fdg

n?u=RePEc:gov:wpaper:1602&r=fdg

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

14<br />

systems, if we ran an interaction between the output gap and the dummy variable<br />

separating electoral systems, the high correlation between individual fixed effects and<br />

the dummy variable would generate a severe problem of multicollinearity. The<br />

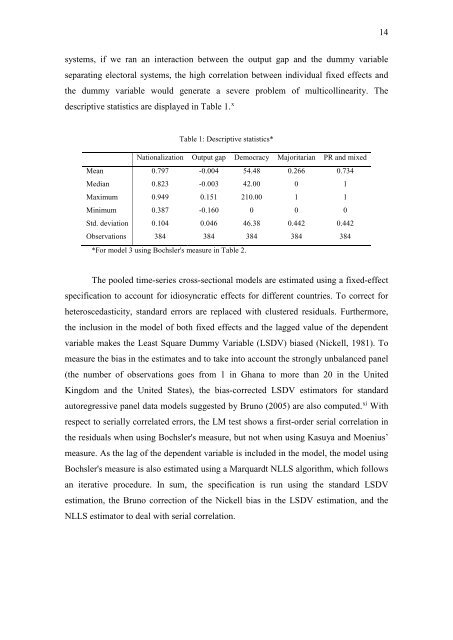

descriptive statistics are displayed in Table 1. x<br />

Table 1: Descriptive statistics*<br />

Nationalization Output gap Democracy Majoritarian PR and mixed<br />

Mean 0.797 -0.004 54.48 0.266 0.734<br />

Median 0.823 -0.003 42.00 0 1<br />

Maximum 0.949 0.151 210.00 1 1<br />

Minimum 0.387 -0.160 0 0 0<br />

Std. deviation 0.104 0.046 46.38 0.442 0.442<br />

Observations 384 384 384 384 384<br />

*For model 3 using Bochsler's measure in Table 2.<br />

The pooled time-series cross-sectional models are estimated using a fixed-effect<br />

specification to account for idiosyncratic effects for different countries. To correct for<br />

heteroscedasticity, standard errors are replaced with clustered residuals. Furthermore,<br />

the inclusion in the model of both fixed effects and the lagged value of the dependent<br />

variable makes the Least Square Dummy Variable (LSDV) biased (Nickell, 1981). To<br />

measure the bias in the estimates and to take into account the strongly unbalanced panel<br />

(the number of observations goes from 1 in Ghana to more than 20 in the United<br />

Kingdom and the United States), the bias-corrected LSDV estimators for standard<br />

autoregressive panel data models suggested by Bruno (2005) are also computed. xi With<br />

respect to serially correlated errors, the LM test shows a first-order serial correlation in<br />

the residuals when using Bochsler's measure, but not when using Kasuya and Moenius’<br />

measure. As the lag of the dependent variable is included in the model, the model using<br />

Bochsler's measure is also estimated using a Marquardt NLLS algorithm, which follows<br />

an iterative procedure. In sum, the specification is run using the standard LSDV<br />

estimation, the Bruno correction of the Nickell bias in the LSDV estimation, and the<br />

NLLS estimator to deal with serial correlation.