ACC 497 Final Exam - Assignment

We specialize in providing you instant exam help to score the marks you have always dreamed. Get online help for the ACC 497 Final Exams 100 Questions with Answers (University of Phoenix).

We specialize in providing you instant exam help to score the marks you have always dreamed. Get online help for the ACC 497 Final Exams 100 Questions with Answers (University of Phoenix).

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

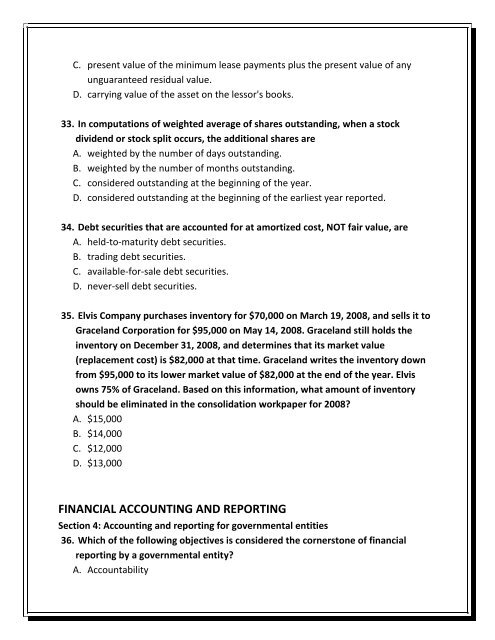

C. present value of the minimum lease payments plus the present value of any<br />

unguaranteed residual value.<br />

D. carrying value of the asset on the lessor's books.<br />

33. In computations of weighted average of shares outstanding, when a stock<br />

dividend or stock split occurs, the additional shares are<br />

A. weighted by the number of days outstanding.<br />

B. weighted by the number of months outstanding.<br />

C. considered outstanding at the beginning of the year.<br />

D. considered outstanding at the beginning of the earliest year reported.<br />

34. Debt securities that are accounted for at amortized cost, NOT fair value, are<br />

A. held-to-maturity debt securities.<br />

B. trading debt securities.<br />

C. available-for-sale debt securities.<br />

D. never-sell debt securities.<br />

35. Elvis Company purchases inventory for $70,000 on March 19, 2008, and sells it to<br />

Graceland Corporation for $95,000 on May 14, 2008. Graceland still holds the<br />

inventory on December 31, 2008, and determines that its market value<br />

(replacement cost) is $82,000 at that time. Graceland writes the inventory down<br />

from $95,000 to its lower market value of $82,000 at the end of the year. Elvis<br />

owns 75% of Graceland. Based on this information, what amount of inventory<br />

should be eliminated in the consolidation workpaper for 2008?<br />

A. $15,000<br />

B. $14,000<br />

C. $12,000<br />

D. $13,000<br />

FINANCIAL <strong>ACC</strong>OUNTING AND REPORTING<br />

Section 4: Accounting and reporting for governmental entities<br />

36. Which of the following objectives is considered the cornerstone of financial<br />

reporting by a governmental entity?<br />

A. Accountability