Harnessing Technology to Narrow the Insurance Protection Gap

harnessing-technology-to-narrow-the-insurance-protection-gap

harnessing-technology-to-narrow-the-insurance-protection-gap

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

THE IMPACT OF NEW TECHNOLOGIES ON THE VALUE CHAIN AND ECONOMICS OF INSURANCE<br />

still rely on traditional underwriting data. 17 As part of<br />

this proposition, policyholders may also receive addedvalue<br />

information from <strong>the</strong>ir insurers, e.g. concerning<br />

<strong>the</strong>ir driving behaviour and health condition. Last but<br />

not least, social network insurance groups will come up<br />

with revolutionary new approaches <strong>to</strong> risk transfer and<br />

sharing. These developments are expected <strong>to</strong> address<br />

shortcomings of traditional insurance products such as<br />

a lack of transparency (e.g. on contracts features) and<br />

relevance. The pricing function will be reshaped by big<br />

data and predictive analytics. The ‘law of large numbers’—<br />

which states that <strong>the</strong> larger <strong>the</strong> number of exposure units<br />

independently exposed <strong>to</strong> loss, <strong>the</strong> greater <strong>the</strong> probability<br />

that actual loss experience will equal expected loss<br />

experience—could arguably be replaced by <strong>the</strong> ‘law of<br />

precise data’. 18 In addition, insurers could see organisational<br />

changes as a result of big data. 19 Artificial intelligence<br />

and cognitive computing are expected <strong>to</strong> enable fur<strong>the</strong>r<br />

breakthroughs in risk assessment and anticipation whilst<br />

raising new challenges as far as collective risk pooling and<br />

mutualisation are concerned.<br />

<strong>Insurance</strong> marketing will become more effective, based<br />

on broader, deeper and more frequent client interactions,<br />

as well as a much increased scope for micro market<br />

segmentation and product personalisation.<br />

A more client-centric behaviour as we know it from o<strong>the</strong>r<br />

industries is set <strong>to</strong> finally penetrate <strong>the</strong> world of insurance.<br />

As mentioned before, <strong>the</strong> cus<strong>to</strong>mer’s experience with<br />

insurance will also be greatly enhanced by offering him or<br />

her an improved understanding of <strong>the</strong> individual risk profile,<br />

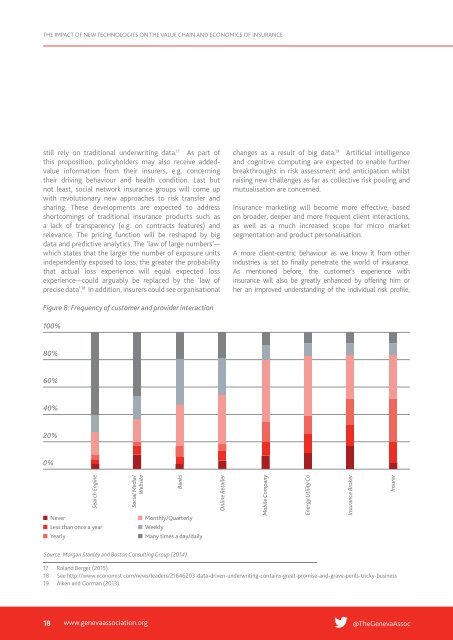

Figure 8: Frequency of cus<strong>to</strong>mer and provider interaction<br />

100%<br />

80%<br />

60%<br />

40%<br />

20%<br />

0%<br />

Search Engine<br />

Never<br />

Less than once a year<br />

Yearly<br />

Social Media/<br />

Website<br />

Banks<br />

Monthly/Quarterly<br />

Weekly<br />

Many times a day/daily<br />

Online Retailer<br />

Mobile Company<br />

Energy Utility Co<br />

<strong>Insurance</strong> Broker<br />

Insurer<br />

Source: Morgan Stanley and Bos<strong>to</strong>n Consulting Group (2014).<br />

17 Roland Berger (2015).<br />

18 See http://www.economist.com/news/leaders/21646203-data-driven-underwriting-contains-great-promise-and-grave-perils-tricky-business<br />

19 Aiken and Gorman (2013).<br />

18 www.genevaassociation.org @TheGenevaAssoc