Harnessing Technology to Narrow the Insurance Protection Gap

harnessing-technology-to-narrow-the-insurance-protection-gap

harnessing-technology-to-narrow-the-insurance-protection-gap

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Case Studies<br />

This section presents a number of case studies which<br />

illustrate <strong>the</strong> impact of technology on <strong>the</strong> spread and<br />

reach of insurance cover. The (small) selection, presented<br />

in alphabetical order, is based on input received from <strong>the</strong><br />

executive and expert interviewees who have contributed <strong>to</strong><br />

this report. The underlying facts and figures were primarily<br />

taken from <strong>the</strong> respective companies’ websites. In addition,<br />

we have endeavoured <strong>to</strong> apply <strong>the</strong> notions of <strong>the</strong> previous<br />

section <strong>to</strong> <strong>the</strong> examples presented.<br />

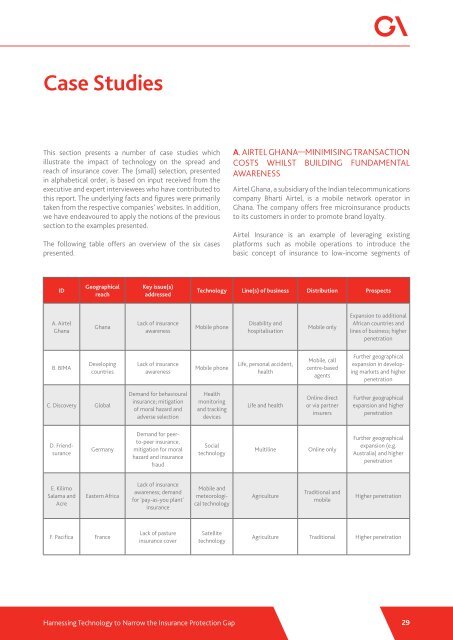

The following table offers an overview of <strong>the</strong> six cases<br />

presented.<br />

A. AIRTEL GHANA—MINIMISING TRANSACTION<br />

COSTS WHILST BUILDING FUNDAMENTAL<br />

AWARENESS<br />

Airtel Ghana, a subsidiary of <strong>the</strong> Indian telecommunications<br />

company Bharti Airtel, is a mobile network opera<strong>to</strong>r in<br />

Ghana. The company offers free microinsurance products<br />

<strong>to</strong> its cus<strong>to</strong>mers in order <strong>to</strong> promote brand loyalty.<br />

Airtel <strong>Insurance</strong> is an example of leveraging existing<br />

platforms such as mobile operations <strong>to</strong> introduce <strong>the</strong><br />

basic concept of insurance <strong>to</strong> low-income segments of<br />

ID<br />

Geographical<br />

reach<br />

Key issue(s)<br />

addressed<br />

<strong>Technology</strong> Line(s) of business Distribution Prospects<br />

A. Airtel<br />

Ghana<br />

Ghana<br />

Lack of insurance<br />

awareness<br />

Mobile phone<br />

Disability and<br />

hospitalisation<br />

Mobile only<br />

Expansion <strong>to</strong> additional<br />

African countries and<br />

lines of business; higher<br />

penetration<br />

B. BIMA<br />

Developing<br />

countries<br />

Lack of insurance<br />

awareness<br />

Mobile phone<br />

Life, personal accident,<br />

health<br />

Mobile, call<br />

centre-based<br />

agents<br />

Fur<strong>the</strong>r geographical<br />

expansion in developing<br />

markets and higher<br />

penetration<br />

C. Discovery Global<br />

Demand for behavioural<br />

insurance; mitigation<br />

of moral hazard and<br />

adverse selection<br />

Health<br />

moni<strong>to</strong>ring<br />

and tracking<br />

devices<br />

Life and health<br />

Online direct<br />

or via partner<br />

insurers<br />

Fur<strong>the</strong>r geographical<br />

expansion and higher<br />

penetration<br />

D. Friendsurance<br />

Germany<br />

Demand for peer<strong>to</strong>-peer<br />

insurance,<br />

mitigation for moral<br />

hazard and insurance<br />

fraud<br />

Social<br />

technology<br />

Multiline<br />

Online only<br />

Fur<strong>the</strong>r geographical<br />

expansion (e.g.<br />

Australia) and higher<br />

penetration<br />

E. Kilimo<br />

Salama and<br />

Acre<br />

Eastern Africa<br />

Lack of insurance<br />

awareness; demand<br />

for 'pay-as-you plant'<br />

insurance<br />

Mobile and<br />

meteorological<br />

technology<br />

Agriculture<br />

Traditional and<br />

mobile<br />

Higher penetration<br />

F. Pacifica France<br />

Lack of pasture<br />

insurance cover<br />

Satellite<br />

technology<br />

Agriculture Traditional Higher penetration<br />

<strong>Harnessing</strong> <strong>Technology</strong> <strong>to</strong> <strong>Narrow</strong> <strong>the</strong> <strong>Insurance</strong> <strong>Protection</strong> <strong>Gap</strong><br />

29