current business statistics - Bureau of Economic Analysis

current business statistics - Bureau of Economic Analysis

current business statistics - Bureau of Economic Analysis

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

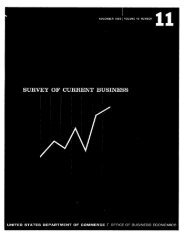

Bank Reserves and Bank Credit<br />

Billion $ (Ratio scale)<br />

40<br />

25 —<br />

600<br />

500<br />

400<br />

360<br />

320<br />

280<br />

240<br />

220<br />

120<br />

100<br />

80<br />

60<br />

50<br />

40<br />

BANK CREDIT<br />

Total<br />

Other<br />

$ecurities<br />

-U.S. G wernment<br />

Serurities<br />

1968 1969 1970 1971<br />

Seasonally Adjusted<br />

U.S. Department <strong>of</strong> Commerce, <strong>Bureau</strong> <strong>of</strong> <strong>Economic</strong> <strong>Analysis</strong><br />

GHART 1<br />

1972<br />

Data: FRB<br />

the BUSINESS SITUATION<br />

72-2-1<br />

JL HE monetary authorities have<br />

moved in recent months to achieve a<br />

more stimulative credit policy and<br />

conditions in money and credit markets<br />

have eased considerably. The Federal<br />

Reserve's open market committee,<br />

which formulates monetary policy,<br />

voted on November 16 u to promote<br />

somewhat greater growth in monetary<br />

and credit aggregates,"• and on December<br />

14 "to promote the degree <strong>of</strong> ease in<br />

bank reserves and money market conditions<br />

essential to greater growth in<br />

monetary aggregates over the months<br />

ahead." These positions have a clearly<br />

more stimulative thrust than the positions<br />

taken in late September and October,<br />

when the committee set policy for<br />

"moderate growth in monetary and<br />

credit aggregates."<br />

The <strong>current</strong> stance <strong>of</strong> monetary<br />

policy was confirmed at mid-February<br />

by the Federal Reserve chairman.<br />

He stated that the Federal Reserve<br />

intends to see that supplies <strong>of</strong> money<br />

and credit are sufficient to finance the<br />

accelerated growth <strong>of</strong> national output<br />

expected this year, and that the Reserve<br />

has no intention <strong>of</strong> allowing the<br />

economic recovery to falter for want <strong>of</strong><br />

money or credit.<br />

Rates and yields<br />

The <strong>current</strong> decline in short-term<br />

rates began last August, when the New<br />

<strong>Economic</strong> Policy was introduced, and<br />

gathered momentum in December and<br />

January. By mid-February most shortterm<br />

rates had declined roughly 2<br />

percentage points from their highs <strong>of</strong><br />

last summer. The Treasury bill yield<br />

and the Federal funds rate were well<br />

below 3% percent and the rates on prime<br />

commercial paper and bankers' acceptances<br />

were below 4 percent. On<br />

February 15, the commercial banks 7<br />

prime loan rate was cut further to 4%<br />

percent. This rate has been reduced \%<br />

percentage points (in six steps) from<br />

last summer and is at its lowest level<br />

since the early 1960's. The decline in<br />

short-term rates has been sufficiently<br />

strong to carry through to consumer<br />

loan rates, which tend to be rather slow<br />

to respond to changes in overall credit<br />

conditions. In early February several<br />

major banks on the West Coast announced<br />

further cuts <strong>of</strong> about.% percentage<br />

point on most categories <strong>of</strong><br />

consumer loan rates.<br />

In long-term markets, yields have<br />

declined only modestly from last summer's<br />

highs. By early February, yields<br />

on long-term U.S. Government securities<br />

had declined less than % percentage<br />

point, yields on corporate Aaa bonds<br />

about % percentage point, and municipal<br />

yields about % point. The decline in<br />

long-term yields had for the most part<br />

ended by early November, and the<br />

small declines that occurred thereafter<br />

have been erased by the moderate upturn<br />

in rates associated with the news<br />

inlate January that the estimated budget<br />

deficit for fiscal 1972 is now much<br />

larger than had been expected. Market<br />

participants were apparently expecting<br />

a deficit in the unified budget in the