2012 Annual Report - Ballarat Health Services

2012 Annual Report - Ballarat Health Services

2012 Annual Report - Ballarat Health Services

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

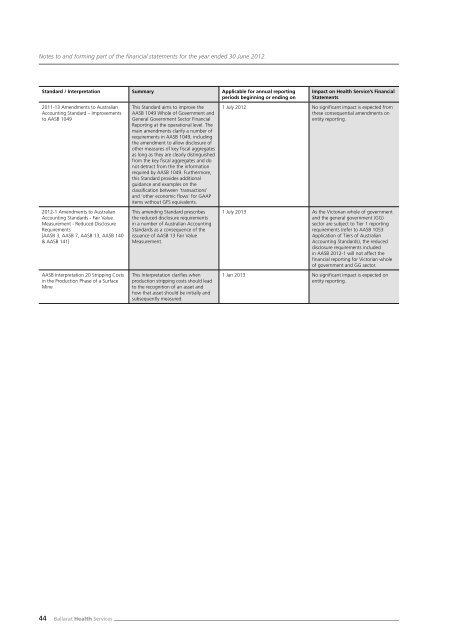

Notes to and forming part of the fi nancial statements for the year ended 30 June <strong>2012</strong>.<br />

Standard / Interpretation Summary Applicable for annual reporting<br />

periods beginning or ending on<br />

2011-13 Amendments to Australian<br />

Accounting Standard – Improvements<br />

to AASB 1049<br />

<strong>2012</strong>-1 Amendments to Australian<br />

Accounting Standards - Fair Value<br />

Measurement - Reduced Disclosure<br />

Requirements<br />

[AASB 3, AASB 7, AASB 13, AASB 140<br />

& AASB 141]<br />

AASB Interpretation 20 Stripping Costs<br />

in the Production Phase of a Surface<br />

Mine<br />

44 <strong>Ballarat</strong> <strong>Health</strong> <strong>Services</strong><br />

This Standard aims to improve the<br />

AASB 1049 Whole of Government and<br />

General Government Sector Financial<br />

<strong>Report</strong>ing at the operational level. The<br />

main amendments clarify a number of<br />

requirements in AASB 1049, including<br />

the amendment to allow disclosure of<br />

other measures of key fi scal aggregates<br />

as long as they are clearly distinguished<br />

from the key fi scal aggregates and do<br />

not detract from the the information<br />

required by AASB 1049. Furthermore,<br />

this Standard provides additional<br />

guidance and examples on the<br />

classifi cation between ‘transactions’<br />

and ‘other economic fl ows’ for GAAP<br />

items without GFS equivalents.<br />

This amending Standard prescribes<br />

the reduced disclosure requirements<br />

in a number of Australian Accounting<br />

Standards as a consequence of the<br />

issuance of AASB 13 Fair Value<br />

Measurement.<br />

This Interpretation clarifi es when<br />

production stripping costs should lead<br />

to the recognition of an asset and<br />

how that asset should be initially and<br />

subsequently measured.<br />

Impact on <strong>Health</strong> Service’s Financial<br />

Statements<br />

1 July <strong>2012</strong> No signifi cant impact is expected from<br />

these consequential amendments on<br />

entity reporting.<br />

1 July 2013 As the Victorian whole of government<br />

and the general government (GG)<br />

sector are subject to Tier 1 reporting<br />

requirements (refer to AASB 1053<br />

Application of Tiers of Australian<br />

Accounting Standards), the reduced<br />

disclosure requirements included<br />

in AASB <strong>2012</strong>-1 will not affect the<br />

fi nancial reporting for Victorian whole<br />

of government and GG sector.<br />

1 Jan 2013 No signifi cant impact is expected on<br />

entity reporting.