You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

A <strong>Brief</strong> <strong>DPL</strong> <strong>Tutorial</strong><br />

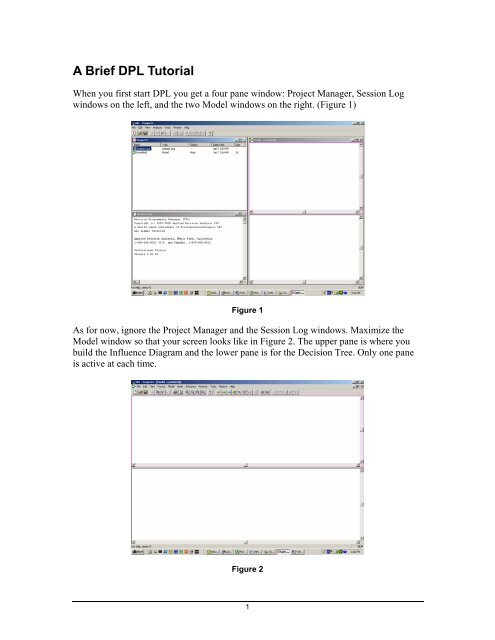

When you first start <strong>DPL</strong> you get a four pane window: Project Manager, Session Log<br />

windows on the left, and the two Model windows on the right. (Figure 1)<br />

Figure 1<br />

As for now, ignore the Project Manager and the Session Log windows. Maximize the<br />

Model window so that your screen looks like in Figure 2. The upper pane is where you<br />

build the Influence Diagram and the lower pane is for the Decision Tree. Only one pane<br />

is active at each time.<br />

Figure 2<br />

1

Policy Tree<br />

You begin creating your <strong>DPL</strong> model by inputting data in the Influence Diagram Pane,<br />

and then perfecting your model by adding and adjusting it in the Decision Tree Pane.<br />

After your decision tree is completed, you can run your analysis (“Analysis/Decision<br />

Analysis”) and <strong>DPL</strong> will create a graphical display of your model – a Policy Tree.<br />

What the Policy Tree does:<br />

♦ Shows the result of your analysis by explicitly displaying every path of the tree.<br />

♦ Fills in the probabilities for each chance event.<br />

♦ Evaluates the Outcome expressions and displays their value under each branch.<br />

♦ Evaluates and displays the Objective Function value in brackets above each<br />

endpoint.<br />

♦ Evaluates and displays the Expected Value of each node, just to the left of each<br />

node, in brackets.<br />

Expected Value<br />

of this node<br />

Get/Pay Value<br />

Objective Function Value<br />

Probability<br />

Figure 3<br />

We will now do a simple example, where there are no uncertainties and we will ignore<br />

the time value of money. You may want to have your copy of <strong>DPL</strong> up and running on<br />

your computer in order to be able to replicate the steps in the examples.<br />

2

Oil field – A<br />

You own a lease to drill for oil. The oilfield will produce 500.000 barrels of oil per year<br />

for two years, at a cost of $13 per barrel. Drilling costs are $2 million. The expected price<br />

of oil over the next two years is constant at $18. Should you drill for oil?<br />

We will now input this data and create our decision tree.<br />

In the Influence Diagram Pane:<br />

♦ Click on the Decision Node icon to create a Decision Node.<br />

♦ Name this node “Drill Decision”.<br />

♦ Click OK<br />

♦ The corresponding decision tree appears automatically in the Decision Tree Pane<br />

In the Decision Tree Pane:<br />

♦ Double-Click on the Decision Node of the decision tree. The Instance Menu<br />

appears. Choose Asymmetric<br />

♦ Double-Click on the “Yes” branch. The Get/Pay menu pops up.<br />

♦ Insert the formula for the profits: -2000+1000*(18-13)<br />

♦ Click OK<br />

Figure 4<br />

3

Running the Analysis<br />

♦ Click “Analysis / Decision Analysis” on the pull down menu<br />

♦ The Decision Analysis Options menu pops up.<br />

♦ Click OK. The Risk Profile is displayed. Close this window.<br />

♦ The Policy Tree is displayed.<br />

Drill_Decision<br />

[3000]<br />

Yes<br />

[3000]<br />

3000<br />

No [0]<br />

Figure 5<br />

We can see that the optimal decision is to drill the well.<br />

Oil field – B<br />

Let’s suppose now that there is price uncertainty only in year 2. In year 2, the expected<br />

price will be either $22, with a 0.30 probability, $18 with a 0.40 probability or $10.What<br />

is your decision now?<br />

To solve this, we must now insert a chance node and compute Year 1 and Year 2 cash<br />

flows separately. We will make the following modifications to the previous model:<br />

In the Influence Diagram Pane:<br />

♦ Click on the Chance Node icon to create a Chance Node.<br />

♦ Name this node “Year2 Price”<br />

♦ Click on the Data tab<br />

♦ Input the 0.30 probability and the 10 price for the “Low” outcome<br />

♦ Input the 0.40 probability and the 18 price for the “Nominal” outcome<br />

♦ Input the 0.30 probability and the 22 price for the “High” outcome<br />

♦ Click OK<br />

In the Decision Tree Pane:<br />

♦ Click anywhere inside the pane to make this the active pane<br />

4

♦ Click on “Node / Add Chance” in the pull down menu.<br />

♦ Choose “Year2 Price”<br />

♦ Attach this chance node to the upper branch of the “Drill Decision” node<br />

♦ Separate the Year 1 and Year 2 production. Double-Click on the “Yes” branch<br />

of<br />

the “Drill Decision” node. The Get/Pay menu pops up.<br />

♦ Change the formula there to: -2000+500*(18-13)<br />

♦ Click OK<br />

♦ Click on any<br />

branch of the “Year2_Price” node. The Get/Pay menu pops up.<br />

♦ Input the Year 2 cash flow formula: 500*(Year2_Price – 13). You can use the<br />

Variable Icon button in the Get/Pay menu to input the Year2 Price variable<br />

instead of typing it in.<br />

At<br />

this point, your screen should look like Figure 6:<br />

Figure 6<br />

After running the analysis, the policy tree shown in Figure 7:<br />

Drill_Decision<br />

[2400]<br />

Year2_Price<br />

Yes<br />

[2400]<br />

500<br />

No [0]<br />

Figure 7<br />

5

You can double-click on the Year2_Price chance node to expand the branches. After<br />

resizing,<br />

the Policy Tree will now look like Figure 8:<br />

Drill_Decision<br />

[2400]<br />

Yes<br />

It is still optimal to drill.<br />

Year2_Price<br />

[2400]<br />

500<br />

No [0]<br />

Figure 8<br />

Low<br />

.300<br />

Nominal<br />

.400<br />

High<br />

.300<br />

[-1000]<br />

-1500<br />

[3000]<br />

2500<br />

[5000]<br />

4500<br />

Note: To resize the contents<br />

of a window pane at any time, use the “ View / Zoom Full”<br />

command, or click on the corresponding icon.<br />

Oil<br />

field – C<br />

Let’s suppose now<br />

that there is price uncertainty in both years of production. Price in<br />

year<br />

1 will be $14, $18 or $22. Price level of year 2 will depend on year 1 prices. The<br />

Year 1 prices will be increased by $4, remain at the same level, or decrease by $6.<br />

Assume that all probabilities are 0.25, 0.50 and 0.25.<br />

We must now insert a second chance node in our model.<br />

But first, go the “Tools /<br />

Options<br />

/ General” pull down menu and change the default probabilities to 0.25, 0.50 and<br />

0.25. Click OK.<br />

In the Influence Diagram<br />

Pane:<br />

♦ Click on the Chance Node icon to create a Chance Node.<br />

rice”<br />

♦ Name this node “Year1 P<br />

♦ Click on the Data tab<br />

♦ Input the 14 price for the “Low” outcome<br />

♦ Input the 18 price for the “Nominal”<br />

outcome<br />

♦ Input the 22 price for the “High” outcome<br />

6

♦ Click OK<br />

In the Decision Tree Pane:<br />

♦ Click anywhere inside the pane to make this the active pane<br />

♦ Click on the “Year 2”<br />

node with the right side of the mouse.<br />

♦ From the menu that appears choose “Detach”. This will separate<br />

this node from<br />

the rest of the tree.<br />

♦ Click on “Node / Add Chance” in the pull down menu.<br />

♦ Choose “Year1 Price”<br />

♦ Attach this chance node to the upper branch of the “Drill Decision” node. You<br />

may want to move nodes around before doing this in order<br />

to make room for this<br />

additional node.<br />

♦ Reattach the “Year 2 Price” node to the end of the “Year 1 Price” node.<br />

♦ Edit “Year 2 Price” by double clicking on the node.<br />

♦ Go to the Data menu and insert the new probabilities and values for each of the<br />

three branches. Ex: The “Low” outcome branch will have a probability of<br />

0.25<br />

and a value of “Year1 Price – 6”, as this outcome has the effect of lowering the<br />

expected oil price, the “Nominal” branch will be simply “Year1 Price”, and the<br />

“High” branch will be “Year1 Price + 4”.<br />

We must<br />

now adjust our formulas to reflect this new situation:<br />

♦ Click on the “Yes” branch of the “Drill Decision”<br />

node. The Get/Pay menu pops<br />

up.<br />

♦ Change the formula there to: -2000 (this leaves only the investment). Click OK<br />

♦ Click on any branch of the “Year1 Price” node. The Get/Pay menu pops up.<br />

♦ Input<br />

the Year 1 cash flow formula: 500*(Year1_Price–13). You can use the<br />

Variable Icon button in the Get/Pay menu to input the Year1 Price variable<br />

instead of typing it in.<br />

At this point, your screen should<br />

look like Figure 9:<br />

7

Figure 9<br />

After running the analysis, the policy tree is as shown in Figure 10:<br />

Drill_Decision<br />

[2750]<br />

Yes<br />

Year1_Price<br />

[2750]<br />

-2000<br />

No [0]<br />

Low<br />

.250<br />

Nominal<br />

.500<br />

High<br />

.250<br />

Year2_Price<br />

[-1250]<br />

500<br />

Year2_Price<br />

[2750]<br />

2500<br />

Year2_Price<br />

[6750]<br />

4500<br />

Figure 10<br />

8<br />

Low<br />

.250<br />

Nominal<br />

.500<br />

High<br />

.250<br />

Low<br />

.250<br />

Nominal<br />

.500<br />

High<br />

.250<br />

Low<br />

.250<br />

Nominal<br />

.500<br />

High<br />

.250<br />

[-4000]<br />

-2500<br />

[-1000]<br />

500<br />

[1000]<br />

2500<br />

[0]<br />

-500<br />

[3000]<br />

2500<br />

[5000]<br />

4500<br />

[4000]<br />

1500<br />

[7000]<br />

4500<br />

[9000]<br />

6500

Substituting a Get/Pay Expression for an Outcome node<br />

We can also set up the model using a Value Node (Outcome node). This has the<br />

advantage of not cluttering up your tree with large quantity of formulas by assigning<br />

them to specific value nodes. In this example we will substitute both “Get/Pay”<br />

expressions for nodes 1 and 2 for an Outcome, or Value node, which we will define in the<br />

Influence Diagram Pane.<br />

To do this we will create another model in this same file (we could also create a new<br />

file).<br />

In the Project Manager Pane:<br />

♦ Press F12 to go to the Project Manager Pane<br />

♦ Click on the current model (untitled)<br />

♦ Right click with your mouse and choose “Rename” to rename the model to<br />

“Model 1”<br />

♦ Right click again and choose “Duplicate” to create a copy of the model. You are<br />

instantly transported to the Model Pane. Press F12 to return to the Project<br />

Manager Pane.<br />

♦ Rename this new model “Model 2”<br />

♦ Right click again on the model and choose “Make Main” 1<br />

♦ Double click on the model to go to the Model Pane<br />

In the Influence Diagram Pane:<br />

♦ Click on the Value Node icon to create a Value Node.<br />

♦ Name this node “Profits”<br />

♦ Click on the Data tab<br />

♦ Key in the formula for the total Profits from both years: 500*(Year1_Price–13)+<br />

500*(Year2_Price–13). This defines profits for both years<br />

♦ Click OK<br />

1 Note that <strong>DPL</strong> will run the model that was last set to “main”.<br />

9

In the Decision Tree Pane:<br />

♦ Click on any branch of the Year1_Price. This will bring up the Get/Pay menu.<br />

♦ Delete the formula in the Get/Pay menu.<br />

♦ Repeat this and delete the Get/Pay formula<br />

for the Year2_Price node also. These<br />

formulas are no longer necessary as they are already specified in the Outcome<br />

Node named “Profits”.<br />

♦ Still in Year2_Price node, clic k on the Variable Icon button<br />

menu and choose “Profits”.<br />

in the Get/Pay<br />

♦ Click OK<br />

At this point, your screen should look like Figure 11:<br />

Figure 11<br />

After running the analysis, the policy tree will be identical<br />

to the one shown in Figure 8.<br />

10

Modeling a Lognormal Distribution with a binomial lattice<br />

Rather than inputting all the expected future prices of an asset, we can assume that prices<br />

will follow a certain distribution, and have the model compute what these values will be.<br />

Let’s assume that a NBI Inc’s current stock price is $100, the volatility is 30% per year,<br />

and that stock prices follow a lognormal distribution. We can model these prices with a<br />

t<br />

binomial lattice, where the up state has a value of u e σ<br />

= and d = 1/u. The probability is<br />

rt<br />

e − d<br />

given by p = . We will create a 5 year model (t=1), where r = 5%.<br />

u−d Open a new <strong>DPL</strong> file. In the Influence Diagram Pane:<br />

♦ Click on the Value Node icon to create a Value Node. We will use these for our<br />

constants.<br />

♦ Name this “u”<br />

♦ Click on the Data tab<br />

♦ Input the formula for u = exp (0.30)<br />

♦ Click Enter and OK<br />

♦ Click on the Value Node icon to create a Value Node.<br />

♦ Name this “d”<br />

♦ Click on the Data tab<br />

♦ Input the formula for d = 1/u<br />

♦ Click Enter and OK<br />

♦ Click on the Value Node icon to create a Value Node.<br />

♦ Name this “r”<br />

♦ Click on the Data<br />

tab<br />

♦ Input the value for r. (0.05)<br />

♦ Click Enter and OK<br />

♦ Click on the Value Node icon to create a Value Node.<br />

♦ Name this “t”<br />

♦ Click on the Data<br />

tab<br />

)<br />

♦ Input the value for t. (1<br />

♦ Click Enter and OK<br />

♦ Click on the Value Node icon to create a Value Node.<br />

♦ Name this “p”<br />

♦ Click on the Data<br />

tab<br />

11

♦ Input the formula for p = [exp(r*t)-d]/(u-d)<br />

♦ Click Enter and OK<br />

♦ Click on the Chance Node icon to create a Chance Node.<br />

♦ Name this node “Yr1”<br />

♦ Modify the outcomes so<br />

♦ Click on the Data tab<br />

♦ Input “p” as the probability<br />

♦ Input $100*u for the “Up” outcome<br />

♦ Input $100*d for the “Down” outcome<br />

♦ Click OK<br />

that we have only two states: “Up” and “Down”<br />

Note that there is no<br />

need to enter the down probability, as the model assumes it is (1-p)<br />

automatically.<br />

We must now create 5 chance nodes that are very similar. The easiest way<br />

to do this is to make a copy of this node and then edit in the modifications. 2<br />

♦ Click on the “Yr1” node<br />

♦ Click “Edit / Copy” and then “Edit / Paste”. A new chance node will appear<br />

♦ Change the name of the new<br />

chance node to “ Yr2”<br />

♦ In the Data tab, replace “100*u” with “Yr1*u” for the “Up” outcome<br />

♦ Replace “100*d” with “Yr1*d” for the “Down” outcome<br />

♦ Click on the “Yr2” node<br />

♦ Click “Edit / Copy” and then “Edit / Paste”. A new chance node will appear<br />

♦ Change the name of the new<br />

chance node to “ Yr3”<br />

♦ In the Data tab, replace “Yr1*u” with “Yr2*u” for the “Up” outcome<br />

♦ Replace “Yr1*d” with “Yr2*d” for the “Down” outcome<br />

Repeat for Chance Nodes “Yr4” and “Yr5”.<br />

In the<br />

Decision Tree Pane:<br />

♦ Click anywhere inside<br />

the pane to make this the active pane<br />

♦ All 5 Chance Nodes are already in place.<br />

♦ Click on any branch of the “Yr1” node. The Get/Pay menu po<br />

♦ Delete the formula there and leave it blank<br />

ps up.<br />

♦ Click OK<br />

♦ Repeat for all chance nodes of the tree except<br />

for the last one (Yr5).<br />

2 Unfortunately this does not work with Student Version 4.0, only with the Full Version<br />

12

At t his point, your screen should look like Figure 12:<br />

The policy tree is shown in Figure 13:<br />

Yr1<br />

[128.403]<br />

Up<br />

.510<br />

Down<br />

.490<br />

Yr2<br />

[164.872]<br />

Yr2<br />

[90.4837]<br />

Up<br />

.510<br />

Down<br />

.490<br />

Yr3<br />

[211.7]<br />

Yr3<br />

[116.183]<br />

Figure 12<br />

Yr4<br />

Up [271.828]<br />

.510<br />

Down<br />

.490<br />

Up<br />

.510<br />

Down<br />

.490<br />

Figure 13<br />

13<br />

Yr4<br />

[149.182]<br />

Yr4<br />

[149.182]<br />

Yr4<br />

[81.8731]<br />

Up<br />

.510<br />

Down<br />

.490<br />

Up<br />

.510<br />

Down<br />

.490<br />

Up<br />

.510<br />

Down<br />

.490<br />

Up<br />

.510<br />

Down<br />

.490<br />

Yr5<br />

[349.034]<br />

Yr5<br />

[191.554]<br />

Yr5<br />

[191.554]<br />

Yr5<br />

[105.127]<br />

Yr5<br />

[191.554]<br />

Yr5<br />

[105.127]<br />

Yr5<br />

[105.127]<br />

Yr5<br />

[57.695]<br />

Up<br />

.510<br />

Down<br />

.490<br />

Up<br />

.510<br />

Down<br />

.490<br />

Up<br />

.510<br />

Down<br />

.490<br />

Up<br />

.510<br />

Down<br />

.490<br />

Up<br />

.510<br />

Down<br />

.490<br />

Up<br />

.510<br />

Down<br />

.490<br />

Up<br />

.510<br />

Down<br />

.490<br />

Up<br />

.510<br />

Down<br />

.490<br />

[448.169]<br />

448.169<br />

[245.96]<br />

245.96<br />

[245.96]<br />

245.96<br />

[134.986]<br />

134.986<br />

[245.96]<br />

245.96<br />

[134.986]<br />

134.986<br />

[134.986]<br />

134.986<br />

[74.0818]<br />

74.0818<br />

[245.96]<br />

245.96<br />

[134.986]<br />

134.986<br />

[134.986]<br />

134.986<br />

[74.0818]<br />

74.0818<br />

[134.986]<br />

134.986<br />

[74.0818]<br />

74.0818<br />

[74.0818]<br />

74.0818<br />

[40.657]<br />

40.657

This tree gives us the distribution of NBI’s stock<br />

five years out. This distribution is<br />

lognormal. We can use this model to calculate the price of options written on this stock.<br />

European<br />

Call Option<br />

Suppose we want to value a European<br />

Call Option on NBI’s stock, with strike price of<br />

180<br />

and 5 years to expiration.<br />

In the Project Manager Pane:<br />

♦ Press F12 to go to the Project Manager Pane<br />

♦ Following the steps explained<br />

previously, create a new model named “European<br />

Call”<br />

♦ Double click on the model to go to the Model Pane<br />

♦ Make this module the “Main” module<br />

In the<br />

Influence Diagram Pane:<br />

♦ Click on the Value Node icon to create a Value Node.<br />

rice”<br />

♦ Name this node “Strike P<br />

♦ Click on the Data tab<br />

♦ Key in 180 for the strike price<br />

♦ Click OK<br />

♦ Click on the Decision Node icon<br />

to create a Decision Node<br />

♦ Name this node “Exercise?”<br />

In the Decision Tree Pane:<br />

♦ Click anywhere inside the pane<br />

to make this the active pane<br />

♦ Click on “Node / Add<br />

Decision” in the pull down menu.<br />

♦ Choose the only option available which is “Exercise?”<br />

♦ Attach this decision node to the “Yr5” chance node<br />

♦ Click on the “Exercise?” node. This will bring up the Ins<br />

♦ Choose “Asymmetric”<br />

tance<br />

Menu<br />

♦ Click on the “Yes” branch of the “Exercise?” node. This will bring up<br />

the<br />

Get/Pay Menu.<br />

♦ Using the Variable Icon button<br />

Strike_Price)/exp(0.05*5)”.<br />

to input the formula “(Yr5 -<br />

3<br />

3 If exercised in year 5, the payoff of the option will be the Year 5 Price less the Strike Price. This<br />

value must be discounted 5 periods at the riskfree rate to arrive at it’s Present Value. If not<br />

exercised, the payoff is zero, which is the automatic assumption of <strong>DPL</strong> trees whenever no<br />

value or formula is provided in the branch.<br />

14

♦ Click on any branch of the “Yr5” node. This will bring up the Get/Pay<br />

menu.<br />

♦ Delete the formula “Yr5” that is there. Click OK<br />

At this point, your model will look like this (Figure 14):<br />

Figure 14<br />

The policy tree will give the result of 15.6892.<br />

American Call Option<br />

We will now value an American<br />

Call Option on the NBI stock, with strike price of 180<br />

and 5 years to expiration.<br />

We will begin by making a copy of the previous file (European Call) which we will<br />

modify for our purposes, basically<br />

by inserting a Decision Node to exercise or not at each<br />

of the 5 time periods. Rename this file “American Call”.<br />

In the Project Manager Pane:<br />

♦ Delete to “Underlying” model and rename the “European<br />

Call” to “American<br />

Call”<br />

♦ Double click on the model to go to the Model Pane<br />

♦ Make this module the “Main” module<br />

In the Influence Diagram Pane:<br />

♦ For convenience, rename the Value Node “ Strike Price” to “X”.<br />

15

♦ Rename the Decision Node “Exercise?” to “ Exercise5?”<br />

♦ Make four copies of this node (Edit/Copy/Paste)<br />

♦ Rename each of these new Decision Nodes “Exercise1”, Exercise2”, “Exercise3”<br />

and “Exercise4?”<br />

In the<br />

Decision Tree Pane:<br />

We will now insert these new nodes at t=1, t=2, t=3 and t= 4.<br />

♦ Click anywhere inside the pane to make this the active pane<br />

♦ Right Click on the “Yr2” node and choose “Detach”. This will separate this node<br />

from the rest of the tree.<br />

♦ Click on “Node / Add<br />

Decision” in the pull down menu.<br />

♦ Choose “Exercise1”<br />

♦ Attach this<br />

decision node to the “Yr1” chance node<br />

e Menu<br />

♦ Click on the “Exercise1” node. This will bring up the Instanc<br />

♦ Choose “Asymmetric”<br />

♦ Click on the “Yes” branch of the “Exercise1?” node. This will bring up the<br />

Get/Pay Menu.<br />

♦ Input the formula “(Yr1-X)/exp(0.05*1)”.<br />

Click OK.<br />

♦ Drag the “Yr2” node and attach it to the lower (“No” ) branch.<br />

♦ Right Click on the “Yr3”<br />

node and choose “Detach”. This will separate this node<br />

from the rest of the tree.<br />

♦ Click on “Node / Add Decision” in the pull down menu.<br />

♦ Choose “Exercise2”<br />

♦ Attach this decision node to the “Yr2” chance node<br />

♦ Click on the “Exercise2” node. This will bring up the Instance Menu<br />

♦ Choose “Asymmetric”<br />

♦ Click on the “Yes” branch of the “Exercise2?” node. This will bring up the<br />

Get/Pay Menu.<br />

♦ Input the formula “(Yr2-X)/exp(0.05*2)”. Click OK.<br />

♦ Drag the “Yr3” node and<br />

attach it to the lower (“No”) branch.<br />

Repeat this procedure for the last two Decision Nodes. (“Exercise3” and “ Exercise4”)<br />

At this point, your model should look somewhat like in Figure 15:<br />

16

Yr1<br />

Up<br />

Down<br />

Exercise1<br />

Yes<br />

(Yr1-X)/exp(0.05*1)<br />

No<br />

Yr2<br />

Up<br />

Down<br />

Exercise2<br />

Yes<br />

(Yr2-X)/exp(0.05*2)<br />

No<br />

Yr3<br />

Up<br />

Down<br />

Yes<br />

(Yr3 - X)/exp(0.05*3)<br />

No<br />

Exercise3<br />

Figure 15<br />

Up<br />

Yr4<br />

Down<br />

Yes<br />

(Yr4-X)/exp(0.05*4)<br />

No<br />

Exercise4<br />

Yr5<br />

Up<br />

Down<br />

Exercise5<br />

Yes<br />

(Yr5-X)/exp(0.05*5)<br />

The policy tree will give the result of 15.6892. Note that this is the same result as with<br />

the European Option. This was expected, because we know that it is never optimal to<br />

exercise American Options early.<br />

Linking <strong>DPL</strong> to a Spreadsheet<br />

♦ You can create a spreadsheet in Excel and then have <strong>DPL</strong> automatically build a<br />

deterministic model from this spreadsheet by linking <strong>DPL</strong> to this spreadsheet.<br />

Then you can edit your <strong>DPL</strong><br />

model to account for chance events and decision<br />

nodes.<br />

♦ Specific <strong>DPL</strong> variables can be linked<br />

to specific spreadsheet cells<br />

♦ Data can be sent both from <strong>DPL</strong> to the spreadsheet and from the spreadsheet to<br />

<strong>DPL</strong>.<br />

♦ In a sensitivity analysis, for example, <strong>DPL</strong> will send a parameter to the<br />

spreadsheet and request an outcome for that particular scenario, which will then<br />

be returned to <strong>DPL</strong> as an outcome value.<br />

In the<br />

Spreadsheet:<br />

♦ Start by<br />

setting up your spreadsheet model.<br />

♦ Only named cells will be linked – you must name all input and output cells.<br />

♦ Spreadsheet must be set up to define one scenario only – <strong>DPL</strong> is the one that will<br />

be doing the sensitivity analysis.<br />

♦ Note that the spreadsheet will function basically as a subroutine of your <strong>DPL</strong><br />

model, or a black box – <strong>DPL</strong> will send data to the<br />

spreadsheet (export link to a<br />

cell with a constant) and get back the result of<br />

a calculation (import link to a cell<br />

with a formula).<br />

Let’s start by building a deterministic model from<br />

a spreadsheet. For this we will use the<br />

spreadsheet<br />

file ChinaOil.xls.<br />

♦ Open a new blank <strong>DPL</strong> model window<br />

17<br />

No

♦ Click on “Tools / Create Model from Excel”.<br />

♦ Choose the “ChinaOil.xls”<br />

spreadsheet.<br />

♦ Click OK. The Influence Diagram of the model appears.<br />

♦ Click on “Format / Arrange Diagram / Left-to-Right” to rearrange the model on<br />

the screen. (Figure 16)<br />

♦ Run the model by clicking on “Analysis / Decision<br />

Analysis” pull down menu.<br />

♦ <strong>DPL</strong> will ask which variable to calculate . Use the Variable Icon button to<br />

♦<br />

choose “NPV”. (Since this is a deterministic model with no decision to make,<br />

there is no decision tree.)<br />

In the Risk Profile graph we can see that the expected value is 88 (on the<br />

horizontal scale), the same<br />

as the spreadsheet. This means that there is 0%<br />

probability that the NPV will be less than 88, and 100% probability that the NPV<br />

will be greater or equal 88.<br />

Adding Uncertainty<br />

OperatingCost<br />

FixedCost<br />

DeclineRate<br />

DevelCost<br />

OilPrice<br />

ProdRate<br />

Figure 16<br />

PSCShare<br />

Reserves<br />

♦ We can now add uncertainties to this deterministic model by changing Value<br />

nodes into Chance nodes.<br />

♦ Let’s begin by inserting an uncertainty in the<br />

Oil Price. We do this by changing<br />

this Value node into a chance node.<br />

♦ Right click on the Oil<br />

Price node. Click on “Change Node Type” and choose<br />

“Chance” to change this node into a Chance node.<br />

♦ When the Node Definition window appears, click OK. You will see that the shape<br />

of this node in the Influence<br />

Diagram pane has changed to a circle.<br />

♦ Double click on the Oil Price node again. The Data window will appear.<br />

18<br />

NPV

♦ The three uncertain outcomes (Low, Nominal, High) have the same original value<br />

of $15. We will now change that to $10, $15 and $25<br />

respectively, to cover the<br />

range of possible oil prices for the problem, while maintaining the default<br />

probabilities for now.<br />

♦ Let’s assume that there is also uncertainty over the level of the reserves. Although<br />

the reserves are estimated to be 90MM Bbl it could be as low as 50 or as high<br />

as<br />

200M.<br />

♦ Right click on the Reserves node. Click on “Change Node Type” and choose<br />

“Chance” to change this node into a Chance node.<br />

♦ When the Node Definition window appears, click OK. You will see that the shape<br />

of this node in the Influence Diagram pane has changed to a circle.<br />

♦ Double click on the Reserves node again. The Data window will appear.<br />

♦ The three uncertain outcomes (Low, Nominal, High) still have the same original<br />

value of 90. We will now change that to 50, 90 and $200 respectively and click<br />

OK.<br />

The influence diagram for the model should look somewhat like Figure 17. Notice the<br />

change in shape (and color) of the two nodes we modified from Value to Chance Nodes.<br />

OperatingCost<br />

FixedCost<br />

DeclineRate<br />

DevelCost<br />

OilPrice<br />

ProdRate<br />

Figure 17<br />

PSCShare<br />

♦ We will now run our analysis again, by clicking on “Analysis/Decision Analysis”<br />

on the pull down menu. We get the Policy Tree shown in Figure 18. We can also<br />

see that the Expected NPV of the project has increased from 88 to 175.8 due to<br />

range of possible values for the uncertain variables that we input.<br />

19<br />

Reserves<br />

NPV

OilPrice<br />

[175.835]<br />

Low<br />

.300<br />

Nominal<br />

.400<br />

High<br />

.300<br />

Reserves<br />

[-31.608]<br />

Reserves<br />

[127.906]<br />

Reserves<br />

[447.183]<br />

Figure 18<br />

Determining the relevant Uncertainties<br />

Low<br />

.300<br />

Nominal<br />

.400<br />

High<br />

.300<br />

Low<br />

.300<br />

Nominal<br />

.400<br />

High<br />

.300<br />

Low<br />

.300<br />

Nominal<br />

.400<br />

High<br />

.300<br />

[-63.029]<br />

-63.029<br />

[-42.9486]<br />

-42.9486<br />

[14.9338]<br />

14.9338<br />

[15.1398]<br />

15.1398<br />

[87.9444]<br />

87.9444<br />

[293.954]<br />

293.954<br />

[174.977]<br />

174.977<br />

[350.058]<br />

350.058<br />

[848.888]<br />

848.888<br />

Attempts to model all uncertainties in a project are time consuming and unnecessary, as<br />

not all uncertainties have a relevant effect on the project’s NPV. <strong>DPL</strong> can help you<br />

determine which uncertainties are relevant by means of a Tornado graph.<br />

♦ Click on “Analysis/Expected Value Tornado Diagram”<br />

♦ In “Value for Sensitivity” choose “Production Rate” and click OK<br />

♦ Enter the low and high values of 0.08 and 0.12.<br />

♦ Click on “Next Value”, choose “Operating Cost” and enter 6 and 11 for the low<br />

and high values.<br />

♦ Click on “Next Value”, choose “Development Cost” and enter 60 and 100 for the<br />

low and high values.<br />

♦ Click on “Next Value”, choose “PSC Share” and enter 0.22 and 0.27 for the low<br />

and high values.<br />

♦ Click on “Run Now”. The Tornado Diagram of Figure 19 indicates that<br />

Operating Cost and Production Rate uncertainties have a much larger impact on<br />

the profitability of the project than Development Costs and PSC Share. This<br />

means you definitely want to model these first two uncertainties, but may pass on<br />

the other less important ones.<br />

20

OperatingCost<br />

ProdRate<br />

DevelCost<br />

PSCShare<br />

Using Utilities<br />

80 100 120 140 160 180 200 220<br />

Figure 19<br />

<strong>DPL</strong> allows for a very simple means of using a utility function to model risk attitudes.<br />

The Strenlar case is a good example of how the risk attitude as modeled by an utility<br />

function can influence the decision making process.<br />

♦ Open the Strenlar1.da file and run the analysis. We get the Policy Tree shown in<br />

Figure 20 that indicates that the optimal alternative for Mr. X is the riskier of<br />

developing the product on his own.<br />

Strenlar_Decision<br />

[3632]<br />

Develop<br />

Lawsuit<br />

[3632]<br />

-200<br />

Technology<br />

Salary [2017.95]<br />

Technology<br />

Cash_Offer [1004.88]<br />

Figure 20<br />

♦ Now suppose Mr. X is risk averse. A good model for this behavior is an<br />

exponential utility function, which can be totally defined by Mr. X risk tolerance,<br />

which we will assume to be 500.<br />

♦ On the pull down menu, go to “Model/Risk Tolerance” and enter the value of 500.<br />

♦ Run the analysis again. We now get a Policy Tree (Figure 21) that clearly<br />

indicates that given that Mr. X is somewhat risk averse, the optimal course of<br />

action in this case is to go with the less risky alternative of accepting a salary in<br />

the firm plus royalties.<br />

21

Strenlar_Decision<br />

[1113.54]<br />

Develop<br />

Lawsuit<br />

[111.508]<br />

-200<br />

Technology<br />

Salary [1113.54]<br />

Technology<br />

Cash_Offer [926.162]<br />

Figure 21<br />

♦ Now suppose Mr. X risk tolerance is lower, maybe 200. On the pull down menu,<br />

go to “Model/Risk Tolerance” and enter the value of 200 and run the analysis<br />

again.<br />

♦ The new Policy Tree (Figure 22) show that such a low risk tolerance (indicating a<br />

very risk averse attitude) Mr. X should go for the alternative with the lowest risk<br />

of all, mainly the upfront cash offer.<br />

Lawsuit<br />

Develop [-84.7736]<br />

-200<br />

Strenlar_Decision<br />

[790.407]<br />

Technology<br />

Salary [659.817]<br />

Technology<br />

Cash_Offer [790.407]<br />

Figure 22<br />

Note: Values inserted in the Node Data are not automatically added to the tree. They<br />

must be specifically invoked from formulas or a “Get/Pay” expression. Values inserted as<br />

“Get/Pay” are automatically included into the tree calculations.<br />

Linking to spreadsheet<br />

♦ Suppose you linked your <strong>DPL</strong> model to a spreadsheet and now you want to add an<br />

additional node link. If you just re-link it will delete your whole <strong>DPL</strong> file<br />

♦ What you want to do is:<br />

♦ Tools/Add linked nodes/From Excel<br />

22

♦ When the window appears, click on the Browse button to re-choose the Excel file to<br />

link<br />

♦ Click “Select”<br />

♦ A new window now appears showing any Excel name that has not yet been linked<br />

♦ Choose the one you want and close all<br />

23