Audit Committee Handbook - Scottish Government

Audit Committee Handbook - Scottish Government

Audit Committee Handbook - Scottish Government

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

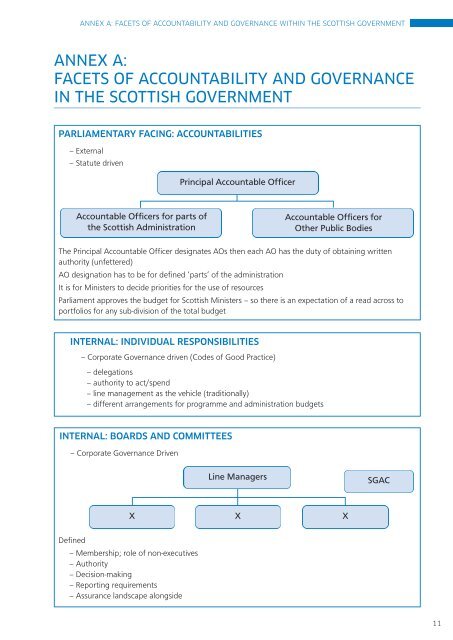

ANNEX A: FACETS OF ACCOUNTABILITY AND GOVERNANCE WITHIN THE SCOTTISH GOVERNMENT<br />

ANNEX A:<br />

FACETS OF ACCOUNTABILITY AND GOVERNANCE<br />

IN THE SCOTTISH GOVERNMENT<br />

PARLIAMENTARY FACING: ACCOUNTABILITIES<br />

– External<br />

– Statute driven<br />

Accountable Officers for parts of<br />

the <strong>Scottish</strong> Administration<br />

Principal Accountable Officer<br />

Accountable Officers for<br />

Other Public Bodies<br />

The Principal Accountable Officer designates AOs then each AO has the duty of obtaining written<br />

authority (unfettered)<br />

AO designation has to be for defined ‘parts’ of the administration<br />

It is for Ministers to decide priorities for the use of resources<br />

Parliament approves the budget for <strong>Scottish</strong> Ministers – so there is an expectation of a read across to<br />

portfolios for any sub-division of the total budget<br />

INTERNAL: INDIVIDUAL RESPONSIBILITIES<br />

– Corporate Governance driven (Codes of Good Practice)<br />

– delegations<br />

– authority to act/spend<br />

– line management as the vehicle (traditionally)<br />

– different arrangements for programme and administration budgets<br />

INTERNAL: BOARDS AND COMMITTEES<br />

– Corporate Governance Driven<br />

Defined<br />

– Membership; role of non-executives<br />

– Authority<br />

– Decision-making<br />

– Reporting requirements<br />

– Assurance landscape alongside<br />

Line Managers SGAC<br />

X X X<br />

11