Audit Committee Handbook - Scottish Government

Audit Committee Handbook - Scottish Government

Audit Committee Handbook - Scottish Government

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

12<br />

AUDIT COMMITTEE HANDBOOK: Guidance for audit committee members in the core <strong>Scottish</strong> <strong>Government</strong><br />

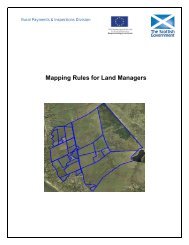

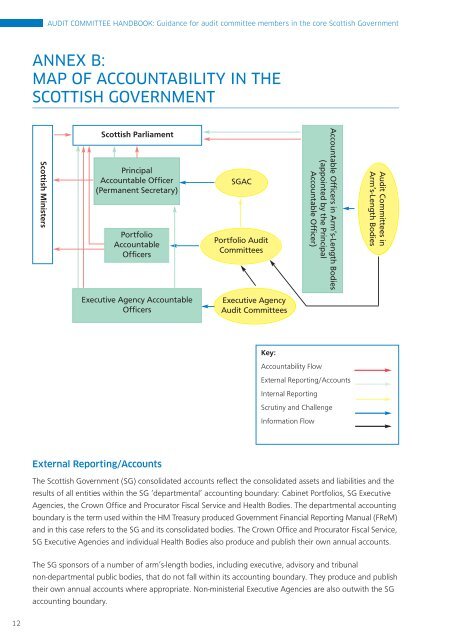

ANNEX B:<br />

MAP OF ACCOUNTABILITY IN THE<br />

SCOTTISH GOVERNMENT<br />

<strong>Scottish</strong> Ministers<br />

<strong>Scottish</strong> Parliament<br />

Principal<br />

Accountable Officer<br />

(Permanent Secretary)<br />

Portfolio<br />

Accountable<br />

Officers<br />

Executive Agency Accountable<br />

Officers<br />

External Reporting/Accounts<br />

SGAC<br />

Portfolio <strong>Audit</strong><br />

<strong>Committee</strong>s<br />

Executive Agency<br />

<strong>Audit</strong> <strong>Committee</strong>s<br />

Accountable Officers in Arm’s-Length Bodies<br />

(appointed by the Principal<br />

Accountable Officer)<br />

Key:<br />

Accountability Flow<br />

External Reporting/Accounts<br />

Internal Reporting<br />

Scrutiny and Challenge<br />

Information Flow<br />

<strong>Audit</strong> <strong>Committee</strong>s in<br />

Arm’s-Length Bodies<br />

The <strong>Scottish</strong> <strong>Government</strong> (SG) consolidated accounts reflect the consolidated assets and liabilities and the<br />

results of all entities within the SG ‘departmental’ accounting boundary: Cabinet Portfolios, SG Executive<br />

Agencies, the Crown Office and Procurator Fiscal Service and Health Bodies. The departmental accounting<br />

boundary is the term used within the HM Treasury produced <strong>Government</strong> Financial Reporting Manual (FReM)<br />

and in this case refers to the SG and its consolidated bodies. The Crown Office and Procurator Fiscal Service,<br />

SG Executive Agencies and individual Health Bodies also produce and publish their own annual accounts.<br />

The SG sponsors of a number of arm’s-length bodies, including executive, advisory and tribunal<br />

non-departmental public bodies, that do not fall within its accounting boundary. They produce and publish<br />

their own annual accounts where appropriate. Non-ministerial Executive Agencies are also outwith the SG<br />

accounting boundary.