e very rigorous. “You definitely need the auditors to come in and kick the tyres very hard,” says Velisarios Kattoulas, chief executive <strong>of</strong> Singapore-based Poseidon Research, which helps conduct M&A due diligence investigations. “You need the lawyers to do the same – and beyond that you need somebody to come in and give a candid assessment <strong>of</strong> the management team,” he adds. “You have to ask: ‘Can I trust these people, and do they have the wherewithal to execute either their business plan or the business plan that we’re looking to impose on them?’ ” Striking a balance While sometimes deals seem too good to be true, experts advise treating M&A transactions on a case-by-case basis. “While a healthy dose <strong>of</strong> scepticism is important, don’t go overboard,” says Nick Gronow, senior managing director at FTI Consulting and a member <strong>of</strong> the <strong>Institute</strong>. “It is unreasonable to expect that everything in a target company is perfect. In fact, if it is, that is probably a warning sign.” China has an undeveloped M&A market and, sadly, the country is best known for the scandalous reverse mergers in the U.S. and Canada such as Sino-Forest and AutoChina. <strong>Hong</strong> <strong>Kong</strong> barely makes the global M&A radar, though the British-owned city banking icon HSBC is notable for its botched acquisition <strong>of</strong> U.S. sub-prime lender Household. Daimler-Benz (Germany) and Chrysler Corporation (U.S.), 1998, US$36 billion Imposing German management culture even on a weak and demoralized American company was bound to fail — and so it did. Sold first to a private equity group and then to Fiat, Chrysler has fared better under Italian control. AOL Corporation (U.S.) and Time Warner (U.S.), 2000, US$164 billion <strong>The</strong> New York Times described the marriage <strong>of</strong> a flashy Internet company and a venerable publisher as a “trail <strong>of</strong> despair.” It resulted in job losses in the thousands, the decimation <strong>of</strong> pensions, legal investigations and accounting frauds. “While a healthy dose <strong>of</strong> scepticism is important, don’t go overboard. It is unreasonable to expect that everything in a target company is perfect. In fact, if it is, that is probably a warning sign.” And if acquirers end up exaggerating the potential missteps, they could miss out on a lucrative deal. A Shanghai real estate developer courted by a multinational was rumoured to be mired in legal scandal. An investigation by Poseidon Research revealed that while two executives <strong>of</strong> the Shanghai developer were the subjects <strong>of</strong> lawsuits, neither the company nor any key personnel had been involved in corruption or other criminal acts. “Inflammatory assertions were unconfirmed,” its report concluded. On the other hand, CPAs should not be silent if a deal might not be in the best interests <strong>of</strong> the acquirer. “Raise the issues with the advisers to the company on the deal,” Clipsham at Mazars advises. “If concerns persist and SOUR no action has been taken, concerns should be formally documented and circulated to all board members.” If you are that dissenting voice, make sure your objections are noted, Yeo at BDO emphasizes: “Your discussions with the board should be documented and filed for internal recording purposes.” Don’t always expect your advice to be heeded. It later emerged that Cathie Lesjak, HP’s CFO, was opposed to the Autonomy deal. “I can’t support it,” Fortune quoted an unnamed HP executive as hearing her say at a board meeting in 2011. She reportedly advised: “I don’t think it’s a good idea. I dont think we're ready. I think it’s too expensive.” HSBC (U.K.) and Household Finance Corporation (U.S.), 2003, US$15 billion Within four years HSBC had racked up write-downs <strong>of</strong> more than the purchase price as poor Americans defaulted on mortgages, credit cards, personal loans and car finance. Knight Vinke, an activist investor, is pressing HSBC to sell it <strong>of</strong>f. Alcatel (France) and Lucent Technologies (U.S.), 2006, US$13.4 billion This technology tie-up has ended with the combined entity on the verge <strong>of</strong> “penny stock” status. Alcatel-Lucent has failed even to capitalize on its massive Bell Laboratories patent portfolio, considered one <strong>of</strong> the jewels in the crown. DEALS Bank <strong>of</strong> America Corporation (U.S.) and Merrill Lynch & Co. (U.S.), 2008, US$81 billion Bank <strong>of</strong> America recently paid out US$2.43 billion in a legal settlement over accusations that it misled investors about the acquisition <strong>of</strong> Merrill Lynch. <strong>The</strong> bank has also struggled with losses on mortgage assets related to the purchase. Sources: Accenture, Bloomberg, Economist Intelligence Unit, company and stock exchange reports A PLUS January 2013 23

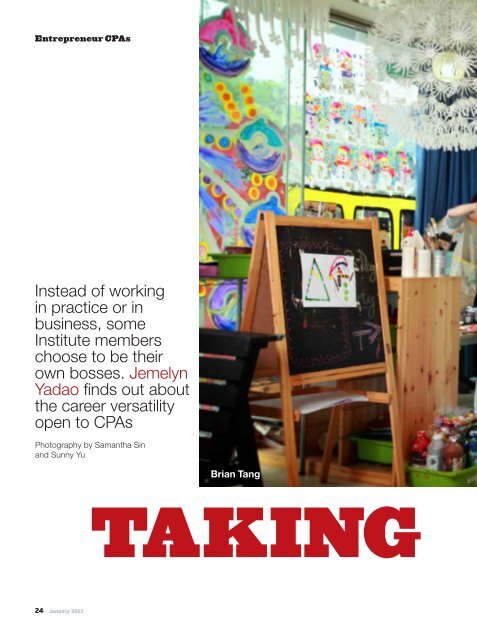

Entrepreneur CPAs Instead <strong>of</strong> working in practice or in business, some <strong>Institute</strong> members choose to be their own bosses. Jemelyn Yadao finds out about the career versatility open to CPAs Photography by Samantha Sin and Sunny Yu 24 January 2013 Brian Tang TAKING