Waste Management in Ireland: Benchmarking Analysis and ... - Forfás

Waste Management in Ireland: Benchmarking Analysis and ... - Forfás

Waste Management in Ireland: Benchmarking Analysis and ... - Forfás

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

18<br />

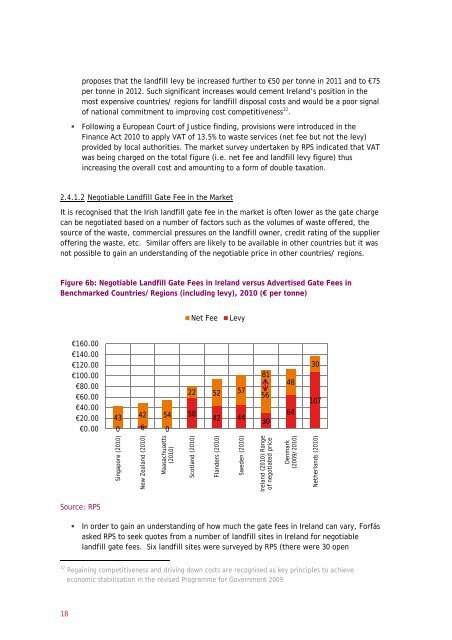

proposes that the l<strong>and</strong>fill levy be <strong>in</strong>creased further to €50 per tonne <strong>in</strong> 2011 <strong>and</strong> to €75<br />

per tonne <strong>in</strong> 2012. Such significant <strong>in</strong>creases would cement <strong>Irel<strong>and</strong></strong>’s position <strong>in</strong> the<br />

most expensive countries/ regions for l<strong>and</strong>fill disposal costs <strong>and</strong> would be a poor signal<br />

of national commitment to improv<strong>in</strong>g cost competitiveness 22 .<br />

Follow<strong>in</strong>g a European Court of Justice f<strong>in</strong>d<strong>in</strong>g, provisions were <strong>in</strong>troduced <strong>in</strong> the<br />

F<strong>in</strong>ance Act 2010 to apply VAT of 13.5% to waste services (net fee but not the levy)<br />

provided by local authorities. The market survey undertaken by RPS <strong>in</strong>dicated that VAT<br />

was be<strong>in</strong>g charged on the total figure (i.e. net fee <strong>and</strong> l<strong>and</strong>fill levy figure) thus<br />

<strong>in</strong>creas<strong>in</strong>g the overall cost <strong>and</strong> amount<strong>in</strong>g to a form of double taxation.<br />

2.4.1.2 Negotiable L<strong>and</strong>fill Gate Fee <strong>in</strong> the Market<br />

It is recognised that the Irish l<strong>and</strong>fill gate fee <strong>in</strong> the market is often lower as the gate charge<br />

can be negotiated based on a number of factors such as the volumes of waste offered, the<br />

source of the waste, commercial pressures on the l<strong>and</strong>fill owner, credit rat<strong>in</strong>g of the supplier<br />

offer<strong>in</strong>g the waste, etc. Similar offers are likely to be available <strong>in</strong> other countries but it was<br />

not possible to ga<strong>in</strong> an underst<strong>and</strong><strong>in</strong>g of the negotiable price <strong>in</strong> other countries/ regions.<br />

Figure 6b: Negotiable L<strong>and</strong>fill Gate Fees <strong>in</strong> <strong>Irel<strong>and</strong></strong> versus Advertised Gate Fees <strong>in</strong><br />

Benchmarked Countries/ Regions (<strong>in</strong>clud<strong>in</strong>g levy), 2010 (€ per tonne)<br />

€160.00<br />

€140.00<br />

€120.00<br />

€100.00<br />

€80.00<br />

€60.00<br />

€40.00<br />

€20.00<br />

€0.00<br />

Source: RPS<br />

43 42 54<br />

0 6 0<br />

S<strong>in</strong>gapore (2010)<br />

New Zeal<strong>and</strong> (2010)<br />

Maasachusetts<br />

(2010)<br />

Net Fee Levy<br />

22 52 57<br />

58<br />

Scotl<strong>and</strong> (2010)<br />

42 44<br />

In order to ga<strong>in</strong> an underst<strong>and</strong><strong>in</strong>g of how much the gate fees <strong>in</strong> <strong>Irel<strong>and</strong></strong> can vary, <strong>Forfás</strong><br />

asked RPS to seek quotes from a number of l<strong>and</strong>fill sites <strong>in</strong> <strong>Irel<strong>and</strong></strong> for negotiable<br />

l<strong>and</strong>fill gate fees. Six l<strong>and</strong>fill sites were surveyed by RPS (there were 30 open<br />

22<br />

Rega<strong>in</strong><strong>in</strong>g competitiveness <strong>and</strong> driv<strong>in</strong>g down costs are recognised as key pr<strong>in</strong>ciples to achieve<br />

economic stabilisation <strong>in</strong> the revised Programme for Government 2009.<br />

Fl<strong>and</strong>ers (2010)<br />

Sweden (2010)<br />

81<br />

56<br />

30<br />

<strong>Irel<strong>and</strong></strong> (2010) Range<br />

of negotiated price<br />

48<br />

64<br />

Denmark<br />

(2009/2010)<br />

30<br />

107<br />

Netherl<strong>and</strong>s (2010)