Comprehensive Annual Financial Report - Harford County Public ...

Comprehensive Annual Financial Report - Harford County Public ...

Comprehensive Annual Financial Report - Harford County Public ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

HARFORD COUNTY PUBLIC SCHOOLS<br />

NOTES TO FINANCIAL STATEMENTS<br />

June 30, 2012<br />

NOTE 6 - POSTEMPLOYMENT BENEFITS OTHER THAN PENSION BENEFITS (continued)<br />

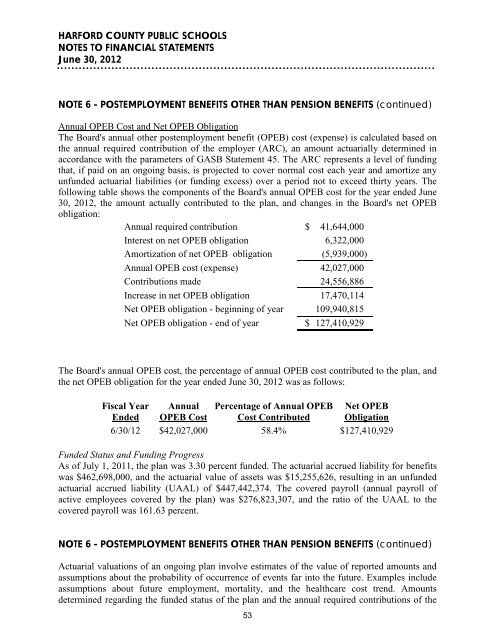

<strong>Annual</strong> OPEB Cost and Net OPEB Obligation<br />

The Board's annual other postemployment benefit (OPEB) cost (expense) is calculated based on<br />

the annual required contribution of the employer (ARC), an amount actuarially determined in<br />

accordance with the parameters of GASB Statement 45. The ARC represents a level of funding<br />

that, if paid on an ongoing basis, is projected to cover normal cost each year and amortize any<br />

unfunded actuarial liabilities (or funding excess) over a period not to exceed thirty years. The<br />

following table shows the components of the Board's annual OPEB cost for the year ended June<br />

30, 2012, the amount actually contributed to the plan, and changes in the Board's net OPEB<br />

obligation:<br />

<strong>Annual</strong> required contribution $ 41,644,000<br />

Interest on net OPEB obligation 6,322,000<br />

Amortization of net OPEB obligation (5,939,000)<br />

<strong>Annual</strong> OPEB cost (expense) 42,027,000<br />

Contributions made 24,556,886<br />

Increase in net OPEB obligation 17,470,114<br />

Net OPEB obligation - beginning of year 109,940,815<br />

Net OPEB obligation - end of year $ 127,410,929<br />

The Board's annual OPEB cost, the percentage of annual OPEB cost contributed to the plan, and<br />

the net OPEB obligation for the year ended June 30, 2012 was as follows:<br />

Fiscal Year <strong>Annual</strong> Percentage of <strong>Annual</strong> OPEB Net OPEB<br />

Ended OPEB Cost Cost Contributed Obligation<br />

6/30/12 $42,027,000 58.4% $127,410,929<br />

Funded Status and Funding Progress<br />

As of July 1, 2011, the plan was 3.30 percent funded. The actuarial accrued liability for benefits<br />

was $462,698,000, and the actuarial value of assets was $15,255,626, resulting in an unfunded<br />

actuarial accrued liability (UAAL) of $447,442,374. The covered payroll (annual payroll of<br />

active employees covered by the plan) was $276,823,307, and the ratio of the UAAL to the<br />

covered payroll was 161.63 percent.<br />

NOTE 6 - POSTEMPLOYMENT BENEFITS OTHER THAN PENSION BENEFITS (continued)<br />

Actuarial valuations of an ongoing plan involve estimates of the value of reported amounts and<br />

assumptions about the probability of occurrence of events far into the future. Examples include<br />

assumptions about future employment, mortality, and the healthcare cost trend. Amounts<br />

determined regarding the funded status of the plan and the annual required contributions of the<br />

53