Funding of Capital Items - Disability Services Commission

Funding of Capital Items - Disability Services Commission

Funding of Capital Items - Disability Services Commission

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

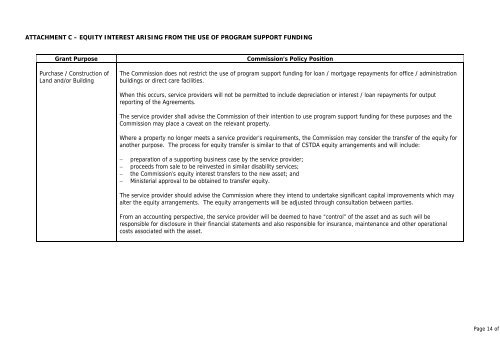

ATTACHMENT C – EQUITY INTEREST ARISING FROM THE USE OF PROGRAM SUPPORT FUNDING<br />

Grant Purpose<br />

Purchase / Construction <strong>of</strong><br />

Land and/or Building<br />

<strong>Commission</strong>’s Policy Position<br />

The <strong>Commission</strong> does not restrict the use <strong>of</strong> program support funding for loan / mortgage repayments for <strong>of</strong>fice / administration<br />

buildings or direct care facilities.<br />

When this occurs, service providers will not be permitted to include depreciation or interest / loan repayments for output<br />

reporting <strong>of</strong> the Agreements.<br />

The service provider shall advise the <strong>Commission</strong> <strong>of</strong> their intention to use program support funding for these purposes and the<br />

<strong>Commission</strong> may place a caveat on the relevant property.<br />

Where a property no longer meets a service provider’s requirements, the <strong>Commission</strong> may consider the transfer <strong>of</strong> the equity for<br />

another purpose. The process for equity transfer is similar to that <strong>of</strong> CSTDA equity arrangements and will include:<br />

−<br />

−<br />

−<br />

−<br />

preparation <strong>of</strong> a supporting business case by the service provider;<br />

proceeds from sale to be reinvested in similar disability services;<br />

the <strong>Commission</strong>’s equity interest transfers to the new asset; and<br />

Ministerial approval to be obtained to transfer equity.<br />

The service provider should advise the <strong>Commission</strong> where they intend to undertake significant capital improvements which may<br />

alter the equity arrangements. The equity arrangements will be adjusted through consultation between parties.<br />

From an accounting perspective, the service provider will be deemed to have “control” <strong>of</strong> the asset and as such will be<br />

responsible for disclosure in their financial statements and also responsible for insurance, maintenance and other operational<br />

costs associated with the asset.<br />

Page 14 <strong>of</strong>

![Heerarka Adeegyada Naafada [PDF 102 kB] - Disability Services ...](https://img.yumpu.com/22096139/1/184x260/heerarka-adeegyada-naafada-pdf-102-kb-disability-services-.jpg?quality=85)

![معايير خدمات الإعاقة [PDF 297 kB] - Disability Services Commission](https://img.yumpu.com/22096120/1/184x260/-pdf-297-kb-disability-services-commission.jpg?quality=85)