Separate Financial Statements 2007 - Indesit

Separate Financial Statements 2007 - Indesit

Separate Financial Statements 2007 - Indesit

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Separate</strong> <strong>Financial</strong> <strong>Statements</strong> as of 31 December <strong>2007</strong><br />

finance the purchase or production of a specific asset are only capitalised if the loans concerned<br />

relate solely to that asset.<br />

Finance leases<br />

Property, plant and equipment held under finance leases, in relation to which <strong>Indesit</strong> Company<br />

S.p.A. has assumed substantially all the risks and rewards of economic, are recognised at fair<br />

value at inception of the lease or, if lower, at the present value of the minimum lease payments,<br />

depreciated over their estimated useful lives and adjusted for any impairment loss determined<br />

on the basis described below. The liability to the lessor is classified among financial payables in<br />

the balance sheet.<br />

Depreciation<br />

Property, plant and equipment are depreciated on a straight-line basis over their estimated<br />

useful lives. Significant parts of plant and machinery with different useful lives are depreciated<br />

separately. Useful lives are monitored on a constant basis, having regard for changes in the<br />

intensity with which these assets are used. Any changes in the depreciation schedules are<br />

applied on a prospective basis.<br />

Carrying amount is verified with reference to the estimated present value of expected future<br />

cash flows and adjusted, where necessary, every time events suggest that the carrying amount<br />

of property, plant and equipment may be impaired, or when there is a marked decrease in their<br />

market value, significant technological changes or evidence of significant obsolescence. The<br />

impairment is reversed if the reasons for recognition cease to apply. Land, whether or not used<br />

for the construction of civil or industrial buildings, is not depreciated since it is deemed to have<br />

an indefinite useful life.<br />

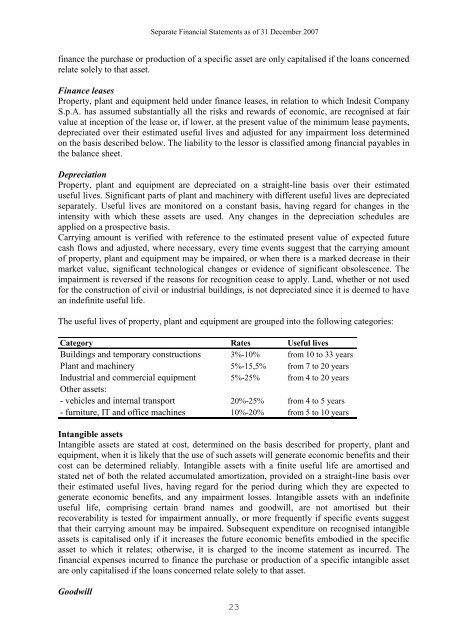

The useful lives of property, plant and equipment are grouped into the following categories:<br />

Category Rates Useful lives<br />

Buildings and temporary constructions 3%-10% from 10 to 33 years<br />

Plant and machinery 5%-15,5% from 7 to 20 years<br />

Industrial and commercial equipment 5%-25% from 4 to 20 years<br />

Other assets:<br />

- vehicles and internal transport 20%-25% from 4 to 5 years<br />

- furniture, IT and office machines 10%-20% from 5 to 10 years<br />

Intangible assets<br />

Intangible assets are stated at cost, determined on the basis described for property, plant and<br />

equipment, when it is likely that the use of such assets will generate economic benefits and their<br />

cost can be determined reliably. Intangible assets with a finite useful life are amortised and<br />

stated net of both the related accumulated amortization, provided on a straight-line basis over<br />

their estimated useful lives, having regard for the period during which they are expected to<br />

generate economic benefits, and any impairment losses. Intangible assets with an indefinite<br />

useful life, comprising certain brand names and goodwill, are not amortised but their<br />

recoverability is tested for impairment annually, or more frequently if specific events suggest<br />

that their carrying amount may be impaired. Subsequent expenditure on recognised intangible<br />

assets is capitalised only if it increases the future economic benefits embodied in the specific<br />

asset to which it relates; otherwise, it is charged to the income statement as incurred. The<br />

financial expenses incurred to finance the purchase or production of a specific intangible asset<br />

are only capitalised if the loans concerned relate solely to that asset.<br />

Goodwill<br />

23