Moody's Approach to Rating Obligations Backed ... - Securitization.Net

Moody's Approach to Rating Obligations Backed ... - Securitization.Net

Moody's Approach to Rating Obligations Backed ... - Securitization.Net

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

STRUCTURED FINANCE<br />

Special Report<br />

Moody’s <strong>Approach</strong> <strong>to</strong> <strong>Rating</strong> <strong>Obligations</strong> <strong>Backed</strong> by<br />

International Airline Ticket Receivables: The Sky’s the Limit<br />

AUTHOR:<br />

Susan C. Knapp<br />

Vice President<br />

Senior Credit Officer<br />

(212) 553-1405<br />

CONTACTS:<br />

Maureen R. Coen<br />

Managing Direc<strong>to</strong>r<br />

(212) 553-3831<br />

Martine Nowicki<br />

Vice President<br />

Senior Credit Officer<br />

(212) 553-0831<br />

Client Services<br />

(212) 553-7941<br />

CONTENTS<br />

• Opinion<br />

• Unique Nature of Air Travel Receivables<br />

• Typical Transaction Structure<br />

• Analysis of Risk Fac<strong>to</strong>rs<br />

• Structural and Legal Elements<br />

• Conclusion: Piercing The Sovereign Ceiling is Possible<br />

• Related Research<br />

OPINION<br />

International airline ticket receivables are created every time the purchase of an<br />

airline ticket for international travel is paid for with a credit card at a travel agency, at<br />

an airline ticket office, over the telephone, or through the internet. 1 Structured financings<br />

have been effected in which credit card receivables arising from the future sale<br />

of tickets (that is, ticket sales which are expected <strong>to</strong> be made in the future but which<br />

do not exist <strong>to</strong>day) in one or more jurisdictions on routes flown by a carrier (for<br />

example, Aeromexico, Avianca, and VARIG) are sold <strong>to</strong> a special purpose company<br />

(SPC). These receivables can then be used <strong>to</strong> support a cross-border structured<br />

finance transaction. 2<br />

Properly structured cross-border transactions backed by the sale of future international<br />

airline ticket receivables may exceed the local currency unsecured debt rating 3<br />

of the carrier and the country ceiling for foreign currency bonds of the jurisdiction<br />

where the carrier is domiciled. 4<br />

1 These receivables could be based on travel between the country of domicile of the airline and any international destination and be derived from ticket<br />

sales charged in any jurisdiction. For illustrative purposes throughout this article, it is assumed that the receivables are being created in the United<br />

States for travel between the United States and the host country of the airline.<br />

2 A cross-border structured financing refers <strong>to</strong> a transaction in which an origina<strong>to</strong>r, such as an airline, located in one jurisdiction, transfers assets <strong>to</strong> an<br />

entity in another jurisdiction, usually either a trust or an SPC. The purchaser of the assets then funds this asset purchase with the issuance of debt.<br />

The debt, which is usually secured by the issuer’s interest in the assets, is repaid from the cash flow generated by the assets.<br />

3 The local currency unsecured debt rating of a carrier reflects its ability <strong>to</strong> meet its local currency debt service obligations on a timely basis.<br />

4 Foreign currency country ceilings assess convertibility or transfer risk, measuring the likelihood that governments would impose restrictions on the<br />

repayment of foreign-currency-denominated obligations.<br />

April 9, 1999

Piercing the local currency rating of the carrier can be an issue if the target foreign currency<br />

rating on the airline ticket receivables securitization exceeds the local currency rating of the<br />

carrier. To receive a transaction rating higher than the carrier’s local currency unsecured debt<br />

rating, the laws of the carrier’s domicile must permit the sale of these future ticket receivables <strong>to</strong><br />

be isolated from the carrier’s property in the event of the carrier’s bankruptcy. Another important<br />

fac<strong>to</strong>r <strong>to</strong> be evaluated in determining whether or not a structured financing can exceed the local<br />

currency unsecured debt rating of the carrier is the his<strong>to</strong>rical relationship between the carrier<br />

and the account deb<strong>to</strong>rs, because the account deb<strong>to</strong>rs generally retain the right <strong>to</strong> cancel their<br />

contracts with the carrier if it files for bankruptcy.<br />

It is also possible for a properly structured transaction <strong>to</strong> exceed the country ceiling for foreign<br />

currency bonds of the carrier’s domicile if the receivables are generated electronically outside<br />

the host country of the carrier by entities whose obligation is <strong>to</strong> remit all funds <strong>to</strong> a fiduciary<br />

agent acting on behalf of the bondholders.<br />

UNIQUE NATURE OF AIR TRAVEL RECEIVABLES<br />

A ticket receivable is created every time a ticket purchased at a travel agency or directly through<br />

the airline at an airline ticket office, over the telephone, or through the internet is paid for using a<br />

credit card. 5 Receivables are created in an amount equal <strong>to</strong> the price of the ticket. 6<br />

When ticket purchases are effected at a travel agency, the agency submits periodic (usually<br />

weekly) reports <strong>to</strong> a central clearing agency. In the United States, Airline Reporting Corporation<br />

(ARC) is the clearing agency. ARC was established by its member airlines <strong>to</strong> provide reporting<br />

and settlement services and related services in connection with the sale of transportation<br />

services by authorized travel agencies in the United States on behalf of participating carriers. 7<br />

The reports specify the amount of U.S. dollars owed <strong>to</strong> the carrier pursuant <strong>to</strong> purchases by the<br />

airline’s cus<strong>to</strong>mers paid through the various credit card companies.<br />

ARC electronically invoices the account deb<strong>to</strong>rs, which are the entities that process and settle<br />

the receivables, for the U.S. dollar amounts owed <strong>to</strong> the origina<strong>to</strong>r. The airline electronically<br />

invoices the account deb<strong>to</strong>rs for tickets sold directly through its airline offices, at airport ticket<br />

counters, and for telephone sales of tickets.<br />

For example, American Express and Diners Club are both credit card companies (i.e., card<br />

issuers), and they are also account deb<strong>to</strong>rs. Purchases made on Visa and MasterCard are<br />

processed by, and payment is effected through, a merchant processor hired by the carrier.<br />

When a ticket for travel on an airline is purchased in the United States through the use of a<br />

credit card, a receivable owing by the account deb<strong>to</strong>r is created. ARC determines the settlement<br />

amount owing <strong>to</strong> the carrier and then the receivables are settled by payment directly <strong>to</strong> the<br />

carrier by the credit card company in the case of American Express and Diners Club, or through<br />

a merchant processor in the case of Visa and MasterCard.<br />

TYPICAL TRANSACTION STRUCTURE<br />

A typical transaction structure for a securitization of future international airline ticket receivables<br />

is outlined below. For illustration purposes, the example provided assumes that the airline ticket<br />

purchases are made in the United States.<br />

5 The receivables may also include amounts due <strong>to</strong> other airlines for services provided. For example, if a ticket is issued with flight segments on two<br />

different airlines, the ticket is normally issued in the name of the airline providing the largest share of the transportation. Therefore, the carrier which<br />

issues the ticket owes the other carrier money for the service which it provided. While the trust can benefit from this arrangement, these inter-airline<br />

payments are the responsibility of the originating airline and are settled through IATA (International Air Transportation Association). Depending upon<br />

the direction of the payment flows, this arrangement may have an impact on the analysis of the transaction’s cash flows. It is important <strong>to</strong> note that<br />

any payments owed by the originating airline are not the responsibility of the trust.<br />

6 The securitization of tickets purchased with cash involve a different settlement process and pose different risks than those tickets purchased with<br />

credit cards.<br />

7 In Europe, for example, there is a Billing and Settlement Plan (BSP) in each of the principal markets. For travel agents located in smaller markets,<br />

tickets are processed through the BSP in a neighboring country.<br />

2 •<br />

Moody’s <strong>Approach</strong> <strong>to</strong> <strong>Rating</strong> <strong>Obligations</strong> <strong>Backed</strong> by International Airline Ticket Receivables

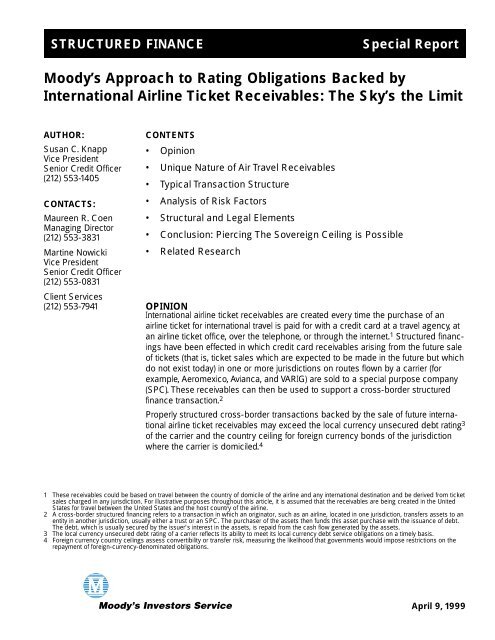

1. The originating airline carrier sells its<br />

future ticket receivables owing from one<br />

or more account deb<strong>to</strong>rs <strong>to</strong> an offshore<br />

(e.g., outside of the carrier’s jurisdiction)<br />

special purpose company (SPC).<br />

2. The SPC issues securities <strong>to</strong> purchase<br />

the receivables. At closing, the carrier<br />

funds a reserve account from the<br />

proceeds of the sale <strong>to</strong> provide credit<br />

support for the transaction and <strong>to</strong> mitigate<br />

the risk that any temporary dip in the<br />

level of receivables generation would<br />

cause an event of default. The origina<strong>to</strong>r<br />

may also unconditionally guarantee the<br />

repayment of the notes.<br />

3. The SPC pledges its right <strong>to</strong> the receivables<br />

<strong>to</strong> a fiduciary agent for the benefit<br />

of the bondholders.<br />

4. Travel agents submit periodic (usually<br />

weekly) reports <strong>to</strong> Airline Reporting<br />

Corporation (ARC). The reports specify<br />

the amount of U.S. dollars owed <strong>to</strong> the<br />

carrier pursuant <strong>to</strong> purchases by the<br />

airline’s cus<strong>to</strong>mers through charges on<br />

the credit card companies.<br />

5. On a daily basis, ARC electronically<br />

invoices the account deb<strong>to</strong>rs for the U.S.<br />

dollar amounts owed <strong>to</strong> the origina<strong>to</strong>r.<br />

The carrier electronically invoices the<br />

account deb<strong>to</strong>rs for tickets sold directly<br />

through its airline offices and at airport<br />

ticket counters.<br />

6. The account deb<strong>to</strong>rs contractually agree<br />

<strong>to</strong> pay amounts owed <strong>to</strong> the origina<strong>to</strong>r<br />

directly <strong>to</strong> the segregated account held<br />

offshore by a fiduciary agent for the<br />

benefit of the bondholders. These<br />

payments are generally made net of<br />

membership dues, chargebacks, and<br />

Travel<br />

Agent<br />

Fiduciary<br />

Figure 1<br />

Transaction Flows<br />

other deductions taken in the normal course of business. The carrier does not receive any<br />

payments directly from the account deb<strong>to</strong>rs until the outstanding balance on the securities<br />

has been fully paid down. All the money flows owed by the account deb<strong>to</strong>rs <strong>to</strong> the carrier<br />

through the ARC settlement process are paid in<strong>to</strong> this segregated account.<br />

7. During each payment period, a fiduciary agent will accumulate funds in the segregated<br />

account until such time as that period’s debt service has been accumulated.<br />

8. As long there is no continuing event of default, a fiduciary agent will remit the receivables<br />

collections in excess of the required amount <strong>to</strong> the origina<strong>to</strong>r until the commencement of the<br />

next payment period. If there is a continuing event of default, generally no funds will be<br />

released <strong>to</strong> the origina<strong>to</strong>r until such breach has been cured.<br />

9. Bondholders receive interest and principal payments on the periodic basis specified in the<br />

transaction documents.<br />

(3)<br />

Merchant<br />

Processor<br />

Pledge of<br />

Assets<br />

(4)<br />

(6)<br />

(5)<br />

Proceeds<br />

(US$)<br />

Bondholders<br />

(2) (2)<br />

(1)<br />

Issuer<br />

Carrier<br />

ARC<br />

AMEX<br />

Carrier<br />

(5) (5)<br />

Bonds<br />

(8)<br />

(9)<br />

(6)<br />

Excess Cash<br />

(7)<br />

Fiduciary<br />

Diners<br />

Club<br />

(6)<br />

Fiduciary<br />

(8)<br />

Excess<br />

Cash<br />

United States<br />

Cayman Islands<br />

Host Country<br />

Moody’s <strong>Approach</strong> <strong>to</strong> <strong>Rating</strong> <strong>Obligations</strong> <strong>Backed</strong> by International Airline Ticket Receivables • 3

ANALYSIS OF RISK FACTORS<br />

In analyzing a transaction backed by international airline ticket receivables, Moody’s considers<br />

various fac<strong>to</strong>rs, including: the sovereign’s ability <strong>to</strong> divert the payments owed <strong>to</strong> the carrier by<br />

the account deb<strong>to</strong>rs 8 ; the financial strength of the carrier and the risk that it will file for bankruptcy;<br />

the carrier’s ability <strong>to</strong> continue <strong>to</strong> operate; the projected levels of debt service coverage<br />

provided by the ticket receivables; the strength of the other transaction participants; any sovereign<br />

risk elements inherent in the transaction; and the legal and structural characteristics of the<br />

transaction.<br />

Sovereign Risk is Limited<br />

In a balance of payments crisis when a government is having difficulty paying its foreign debt<br />

service, the government could adopt desperate measures in an attempt either <strong>to</strong> maximize its<br />

receipt of foreign exchange generated by the entities domiciled within its jurisdiction or <strong>to</strong> prioritize<br />

the distribution of foreign exchange according <strong>to</strong> its assessment of the country’s needs.<br />

These measures could include the implementation of foreign exchange controls <strong>to</strong> limit and<br />

control the outflow of foreign exchange; the imposition of a debt mora<strong>to</strong>rium; the implementation<br />

of a debt rescheduling or writedown; and the requirement that genera<strong>to</strong>rs of foreign<br />

exchange remit all proceeds directly <strong>to</strong> the Central Bank. The probability of any of these events<br />

occurring is reflected in a country’s foreign currency country ceiling for long-term debt. 9<br />

In a sovereign bond default scenario, a sovereign might attempt <strong>to</strong> interfere with an airline ticket<br />

receivable securitization by requiring that the parties <strong>to</strong> the transaction remit all funds arising<br />

from the carrier’s offshore ticket sales back <strong>to</strong> the Central Bank. To the extent that the transaction<br />

structure could not withstand these attempts <strong>to</strong> interfere, the rating assigned could not<br />

pierce the country ceiling.<br />

However, Moody’s believes that the ability of a sovereign <strong>to</strong> interfere with a securitization<br />

based on the sale of future international airline ticket receivables is extremely limited.<br />

Although a government has control over a carrier which is located in its jurisdiction, receivables<br />

related <strong>to</strong> tickets purchased using a credit card are generated and settled through electronic<br />

means outside of the jurisdiction of the carrier. Therefore, the government has no direct control<br />

over the cash flow. This is true because:<br />

• All payments are recorded and effected through the offshore account mechanisms of the<br />

account deb<strong>to</strong>rs – no cash flows back <strong>to</strong> the carrier’s home country unless approved by a<br />

fiduciary agent acting on behalf of the bondholders. This settlement mechanism severely<br />

limits the ability of the carrier’s host government <strong>to</strong> require the repatriation of all ticket<br />

proceeds directly back <strong>to</strong> the host country;<br />

• The account deb<strong>to</strong>rs, which have contractually agreed <strong>to</strong> make all payments <strong>to</strong> an offshore<br />

account held for the benefit of the bondholders, are outside the jurisdiction and control of the<br />

government of the carrier. This fact limits the ability of that government <strong>to</strong> control their<br />

actions; and<br />

• The obligations of the account deb<strong>to</strong>rs <strong>to</strong> remit all U.S. dollar payments <strong>to</strong> a segregated<br />

account held by a fiduciary agent for the benefit of the bondholders are irrevocable and are<br />

assumed under U.S. law. If the account deb<strong>to</strong>rs were <strong>to</strong> redirect the U.S. dollar payments<br />

away from the designated account, this act would cause a breach of contract and could<br />

subject them <strong>to</strong> potential legal action by the bondholders.<br />

8 The account deb<strong>to</strong>rs are the entities which process and settle the receivables. For example, American Express and Diners Club are both credit card<br />

companies (i.e., card issuers) and account deb<strong>to</strong>rs. Purchases made on Visa and MasterCard are processed by and payment is effected through a<br />

merchant processor hired by the carrier.<br />

9 Foreign currency defaults by both sovereign and private sec<strong>to</strong>r borrowers in some of the emerging markets have been relatively common since the<br />

late 1970s. In most of these instances, governments have imposed various payment restrictions on foreign currency debt obligations of issuers in<br />

that country.<br />

4 •<br />

Moody’s <strong>Approach</strong> <strong>to</strong> <strong>Rating</strong> <strong>Obligations</strong> <strong>Backed</strong> by International Airline Ticket Receivables

Although unlikely, the government might also try <strong>to</strong> order the reorganization of the carrier in<strong>to</strong> a<br />

new corporate entity solely for the purpose of disrupting the securitization so that the transaction<br />

documents become unenforceable. To the extent that the bonds carry the guarantee of the<br />

carrier, this risk of reorganization may be limited in achieving its intended purpose; the reorganization<br />

may not be recognized by foreign courts if its sole purpose was <strong>to</strong> interfere with the cash<br />

flows of the transaction.<br />

Generation Risk: Can the Transaction Stay Aloft?<br />

The assets being sold in a future receivables transaction do not exist on the date of the sale.<br />

Therefore, if the carrier goes out of business or if it becomes bankrupt and is not permitted <strong>to</strong><br />

sell future receivables, no further receivables will be generated and inves<strong>to</strong>rs will suffer a loss.<br />

Depending on the laws of the jurisdiction where the carrier is located, even if the carrier stays in<br />

business its bankruptcy may void the transfer of any receivables generated after the filing of the<br />

bankruptcy proceeding. If the carrier’s bankruptcy works <strong>to</strong> void the transfer of future receivables,<br />

the rating assigned <strong>to</strong> the securitization will be constrained by the carrier’s local currency rating.<br />

In addition, the impact of a deterioration in the carrier’s credit quality may have a less obvious<br />

impact. Credit quality deterioration may cause the carrier <strong>to</strong> reduce the service it provides on<br />

certain routes potentially diminishing the amount of receivable generation. Additionally, if the<br />

carrier is unable <strong>to</strong> service its aircraft lease obligations, the lessor may decide <strong>to</strong> repossess the<br />

aircraft. A lessor’s decision <strong>to</strong> repossess aircraft may be affected by fac<strong>to</strong>rs such as its his<strong>to</strong>rical<br />

relationship with the carrier and its ability <strong>to</strong> re-lease the aircraft <strong>to</strong> another entity at that point in<br />

time. For these reasons, it is important <strong>to</strong> assess the credit quality of the airline and how its<br />

credit quality may impact its ability <strong>to</strong> generate, or transfer, sufficient receivables <strong>to</strong> repay all<br />

obligations in accordance with the transaction documents.<br />

Effect of Carrier’s Bankruptcy or Liquidation on the <strong>Securitization</strong><br />

In analyzing an airline ticket future receivables transaction, Moody’s reviews the carrier’s financial<br />

condition <strong>to</strong> assess its credit quality. An understanding of the carrier’s financial condition will<br />

help Moody’s evaluate the likelihood that the airline will file for bankruptcy protection, liquidate its<br />

business, or default on important financial obligations. The occurrence of any of these circumstances<br />

is likely <strong>to</strong> have a material impact on the likelihood that inves<strong>to</strong>rs will be repaid under<br />

the securitization.<br />

Effect of Bankruptcy Laws<br />

The relevant measure of the carrier’s credit quality for purposes of analyzing a future airline<br />

ticket securitization may not be directly related <strong>to</strong> the carrier’s ability <strong>to</strong> pay its local or foreign<br />

currency denominated obligations. Depending upon the bankruptcy law of the jurisdiction where<br />

the carrier is located, the receivables generated after the carrier’s bankruptcy may be able <strong>to</strong> be<br />

transferred. Brazil, Mexico, and Peru are a few of the jurisdictions where a carrier’s bankruptcy<br />

will not prevent receivables generated after the bankruptcy filing <strong>to</strong> be transferred <strong>to</strong> a third party<br />

<strong>to</strong> honor a pre-bankruptcy sale obligation. In these jurisdictions, which tend <strong>to</strong> be civil law jurisdictions,<br />

if the carrier defaults on its debts, it may still continue <strong>to</strong> fly and therefore continue <strong>to</strong><br />

generate and transfer receivables after bankruptcy.<br />

In jurisdictions where the laws permit transfer of receivables, Moody’s evaluates the probability<br />

that the airline might cease operations over the life of the transaction, because if the airline does<br />

not fly, no receivables will be generated. As part of this analysis, Moody’s takes in<strong>to</strong> consideration<br />

the carrier’s importance <strong>to</strong> its host country either as the flag carrier of the country or as a<br />

significant genera<strong>to</strong>r of foreign exchange or local jobs.<br />

In other jurisdictions, where bankruptcy prevents the transfer of future generated receivables the<br />

local currency rating of the carrier, which gives an indication of the carrier’s creditworthiness, will<br />

likely act as a rating ceiling for the transaction, in the absence of other significant protections.<br />

Moody’s <strong>Approach</strong> <strong>to</strong> <strong>Rating</strong> <strong>Obligations</strong> <strong>Backed</strong> by International Airline Ticket Receivables • 5

Satisfaction of Third Party <strong>Obligations</strong><br />

The financial strength of the carrier will probably affect its relationships with the account deb<strong>to</strong>rs<br />

and the amount of service provided. For example, account deb<strong>to</strong>rs generally retain the right <strong>to</strong><br />

cancel their contracts with the carrier if the carrier files for bankruptcy, because they have financial<br />

exposure <strong>to</strong> the carriers. This cancellation could cause a sudden drop in the level of receivables<br />

being generated. If there is a his<strong>to</strong>ry of a long and profitable relationship with the carrier,<br />

the account deb<strong>to</strong>rs may be inclined <strong>to</strong> seek a work-out with the carrier through a closely moni<strong>to</strong>red<br />

period as long as the carrier continues <strong>to</strong> fly. But it is possible that the account deb<strong>to</strong>rs<br />

might start <strong>to</strong> withhold additional cash otherwise payable <strong>to</strong> the carrier in order <strong>to</strong> create a<br />

reserve fund <strong>to</strong> limit their exposure <strong>to</strong> the carrier against higher than anticipated refunds and<br />

chargebacks. The probability of this situation occurring is fac<strong>to</strong>red in<strong>to</strong> Moody’s analysis.<br />

Cash Flow Coverage and Volatility<br />

In assigning a rating <strong>to</strong> a ticket receivable transaction, Moody’s performs a quantitative and<br />

qualitative analysis <strong>to</strong> project the cash flow coverage over the life of the transaction.<br />

From a quantitative perspective, the analysis takes in<strong>to</strong> account his<strong>to</strong>rical levels of receivables<br />

generated by the carrier <strong>to</strong> evaluate any trends, seasonality, and volatility which may have<br />

affected the generation of the receivables in the past and which may continue <strong>to</strong> impact receivables<br />

generation in the future.<br />

From a qualitative perspective, Moody’s considers those micro- and macro-economic fac<strong>to</strong>rs<br />

which can influence travel patterns. The flow of receivables for a particular carrier generally<br />

depends on the volume of <strong>to</strong>urist and business travel on the selected routes, and competition<br />

from other carriers. There are also other relevant fac<strong>to</strong>rs. For instance, an understanding of the<br />

operating his<strong>to</strong>ry of the carrier is important <strong>to</strong> assess the carrier’s ability <strong>to</strong> generate sufficient<br />

receivables <strong>to</strong> make required payments on the securities over the term of the transaction. This<br />

analysis includes an evaluation of the carrier’s domestic operating environment and the international<br />

markets in which it operates, as well as the his<strong>to</strong>rical and projected market shares.<br />

What is the Competitive Environment?<br />

To assess the impact of competition, Moody’s considers which airlines currently compete with<br />

the originating carrier in its domestic and international markets. If the markets are highly<br />

competitive, the likelihood that the carrier will be able <strong>to</strong> compete successfully with the other<br />

participants and maintain or increase its market share will be evaluated. The probability that<br />

there will be new entrants in the market over the life of the transaction is taken in<strong>to</strong> account<br />

when projecting the level of receivables available <strong>to</strong> support payments on the securities. In the<br />

United States, for example, there have been major shifts in market share which have allowed<br />

airlines such as Southwest <strong>to</strong> come in; in some cases these shifts have caused carriers <strong>to</strong> exit.<br />

Because of bilateral agreements overseas, it can be harder <strong>to</strong> shift market share between<br />

various airlines.<br />

Cyclical Risk vs. Event Risk<br />

The international airline industry is cyclical and remains subject not only <strong>to</strong> economic conditions<br />

in its domestic market and general economic conditions worldwide because of the discretionary<br />

nature of air travel, but also <strong>to</strong> event risk (such as natural disasters and civil disturbance).<br />

Cyclical implies increases or decreases in air travel which occur over time. Triggers in the transaction<br />

which specify a minimum acceptable level of receivables can help <strong>to</strong> protect inves<strong>to</strong>rs<br />

from a slow decline in the generation of receivables by accelerating repayment of the bonds if<br />

the amount of receivables generation falls below a certain level, such as three times debt<br />

service coverage.<br />

It is harder <strong>to</strong> mitigate event risk which could cause a sudden drop in air travel (and the generation<br />

of receivables) between two countries. For example, fear of terrorism was a major fac<strong>to</strong>r in<br />

the reduction in airline industry profitability during the Gulf War. However, some of the effects of<br />

6 •<br />

Moody’s <strong>Approach</strong> <strong>to</strong> <strong>Rating</strong> <strong>Obligations</strong> <strong>Backed</strong> by International Airline Ticket Receivables

event risk can be ameliorated if, for example, travel between the two countries includes various<br />

destinations so that an event in one destination might not affect travel <strong>to</strong> another. In the case of<br />

Mexico, a natural disaster in one location (such as a hurricane in Acapulco) might merely result<br />

in the redirection of travelers <strong>to</strong> another Mexican destination, such as Cancún.<br />

Moody’s also looks for any trends that may affect travel between the various markets which are<br />

the subject of the securitization. For example, if the carrier’s receivables generated from ticket<br />

sales in the United States are the subject of the securitization, Moody’s will analyze the his<strong>to</strong>rical<br />

and projected traffic between the United States and the carrier’s home country; whether ticket<br />

sales are driven by <strong>to</strong>urism, business, or some combination of the two; the effect, if any, of<br />

natural disasters and civil disturbances on travel between the two countries; and the macroand<br />

micro-economic trends which could impact air travel generally and between the two countries<br />

specifically.<br />

Adjustments <strong>to</strong> Receivables by Account Deb<strong>to</strong>rs<br />

The account deb<strong>to</strong>rs have the right <strong>to</strong> make adjustments <strong>to</strong> the receivable amounts owed <strong>to</strong> the<br />

originating carrier. These adjustments may result from discount fees payable <strong>to</strong> the account<br />

deb<strong>to</strong>rs, refunds for tickets not used and returned <strong>to</strong> the airline; se<strong>to</strong>ffs, or chargebacks which<br />

are deductions taken as a result of computation errors, unauthorized charges and charges<br />

disputed by the cardholder. Since these adjustments reduce the cashflow <strong>to</strong> the originating<br />

carrier, the his<strong>to</strong>rical level of adjustments is analyzed by Moody’s in determining the sufficiency<br />

of the expected receivables levels and related cash flows.<br />

Potential Impact of Code-Sharing Alliances Cash Flow Volatility<br />

Another fac<strong>to</strong>r which can affect the volatility of cash flow is the existence of code-sharing<br />

alliances between the carrier and one or more international carriers. 10 Code-sharing alliances<br />

may cause the revenues <strong>to</strong> be redistributed. The redistribution of revenues may have a positive<br />

or negative impact on the transaction. For example, if more code-sharing flights are booked<br />

under a partner’s name, it may have a detrimental effect on the level of receivables generated<br />

despite the overall benefit <strong>to</strong> the carrier. This is because the inter-airline receivables would be<br />

settled via IATA and would remain outside the scope of the ARC settlement process and therefore,<br />

outside the scope of the transaction. 11 If the code-sharing arrangement is well established,<br />

it should be easier <strong>to</strong> discern what impact, if any, the arrangement has had on the level of<br />

his<strong>to</strong>rical level of receivables generation.<br />

Seasonality of the Cash Flow<br />

It is also important <strong>to</strong> determine whether or not the cash flows are seasonal <strong>to</strong> assess whether<br />

the transaction’s structure mitigates the risk of a payment disruption. For example, if the securitization<br />

requires that the payments <strong>to</strong> bondholders are made on a monthly basis, but the carrier’s<br />

ability <strong>to</strong> generate receivables is highly seasonal, a payment disruption could be caused by a<br />

temporary decline in receivables flows.<br />

Structural adjustments <strong>to</strong> compensate for seasonality might include the inclusion of a reserve<br />

account, or structuring principal amortization in accordance with expected receivable levels.<br />

Moody’s analyzes his<strong>to</strong>rical and projected volatility of the cash flows in order <strong>to</strong> minimize the<br />

probability of a payment disruption. Volatility risk of the cash flows can be mitigated through<br />

overcollateralization and required minimum coverage levels.<br />

10 All of the major world airlines participate in numerous alliances. These range from simple sharing of capacity on a limited number of routes <strong>to</strong> full<br />

code sharing agreements with antitrust immunity. Some involve equity participation, but most do not.<br />

Originally alliances were of limited scope, usually with smaller airlines, and were intended <strong>to</strong> fill voids in selected markets. More recently, some of the<br />

largest airlines around the world have become involved and the programs are much more comprehensive. The goal is <strong>to</strong> capture high fare travelers<br />

and keep them on the system as long as possible.<br />

11 Fac<strong>to</strong>rs which can influence travelers’ preference for one airline over another in a code-sharing alliance include membership in select frequent flyer<br />

programs, corporate travel contracts with specific airlines, and travel agents’ incentives <strong>to</strong> ticket passengers on one airline versus another.<br />

Moody’s <strong>Approach</strong> <strong>to</strong> <strong>Rating</strong> <strong>Obligations</strong> <strong>Backed</strong> by International Airline Ticket Receivables • 7

Basket of Credit Cards Accepted May Influence Cash Flows<br />

The basket of credit cards which the carrier accepts as a form of payment can also influence<br />

the aggregate level of receivables generated. As mentioned above, receivables are created<br />

when a cardholder uses a credit card <strong>to</strong> purchase an airline ticket. The greater the basket of<br />

credit card companies included in the transaction, the lower the likelihood that consumer preference<br />

for one card over another will have a negative impact on receivables flows.<br />

This flexibility is evaluated by analyzing the percentage of the carrier’s receivables which are<br />

accounted for by sales through those credit cards <strong>to</strong> be included in the securitization. In addition,<br />

Moody’s analyzes the his<strong>to</strong>rical sales patterns for the different credit card companies <strong>to</strong><br />

ensure that the receivables being sold <strong>to</strong> the SPC represent a substantial portion of the carrier’s<br />

eligible receivables.<br />

Strength of Transaction Participants<br />

The principal transaction participants include:<br />

• The airline carrier, as the origina<strong>to</strong>r of the receivables<br />

• The account deb<strong>to</strong>rs, as the obligors of all amounts owing under the receivables<br />

• The credit card companies, which provide a method of payment for the airline services (<strong>to</strong><br />

the extent different from the account deb<strong>to</strong>rs)<br />

• The fiduciary agents involved, such as an indenture trustee<br />

• Any guaran<strong>to</strong>rs<br />

• Any third party providers of credit enhancement<br />

The importance of the carrier as the genera<strong>to</strong>r of the receivables <strong>to</strong> the transaction has already<br />

been discussed. Moody’s analysis of the other participants in the deal focuses on their credit<br />

strength and their ability <strong>to</strong> perform their obligations under the transaction documents. Highly<br />

rated counterparties can reduce the probability of an interruption in payments <strong>to</strong> bondholders<br />

once the carrier has complied with its obligation <strong>to</strong> generate the receivables and provide the<br />

requisite services because of the relatively low risk of payment default associated with highly<br />

rated counterparties.<br />

In the case of the credit card companies, their ability <strong>to</strong> remain competitive with consumers in<br />

the face of alternative methods of payment receives particular attention. If, either through technological<br />

obsolescence or consumer preference, consumers s<strong>to</strong>p purchasing airline tickets with<br />

the credit cards whose receivables have been sold <strong>to</strong> the securitization, there would be an<br />

adverse impact on the generation of receivables.<br />

Transactions have been structured which rely on the generation of receivables sales using Visa<br />

(A1/P1), MasterCard (NR), Diners Club (NR), and American Express (Aa3/P1)/Optima credit<br />

cards. The settlement mechanism for funds due from Visa and MasterCard is through the<br />

merchant processor selected by the carrier. 12 As a result, the carrier is exposed <strong>to</strong> the credit<br />

risk of the merchant processor. The transaction documents should provide for the substitution<br />

of merchant processors if the merchant processor does not perform its functions satisfac<strong>to</strong>rily<br />

or decides <strong>to</strong> exit the merchant processing line of business.<br />

However, the substitute processor must agree <strong>to</strong> abide by the terms of the transaction documents.<br />

In analyzing the risk of the role played by unrated entities, Moody’s considers the entity’s<br />

credit quality, operating his<strong>to</strong>ry, market share, and what percentage of the projected receivables<br />

they account for.<br />

12 The role of a merchant processor is <strong>to</strong> process and settle all ticket purchases which are made using Visa or MasterCard.<br />

8 •<br />

Moody’s <strong>Approach</strong> <strong>to</strong> <strong>Rating</strong> <strong>Obligations</strong> <strong>Backed</strong> by International Airline Ticket Receivables

Moody’s reviews the carrier’s his<strong>to</strong>rical relationship with each credit card company and the<br />

his<strong>to</strong>rical level of adjustments <strong>to</strong> receivables (chargebacks, refunds, discount fees, and se<strong>to</strong>ffs),<br />

in addition <strong>to</strong> assessing their financial strength. Both of these fac<strong>to</strong>rs can affect the cash flows<br />

available <strong>to</strong> repay bondholders. In the first instance, the adjustments can make the cash flows<br />

more volatile. In the second instance, if the credit card company should file for bankruptcy, there<br />

may be outstanding amounts due the carrier which may remain unpaid.<br />

Finally, Moody’s analyzes the credit quality of other participants, such as guaran<strong>to</strong>rs and other<br />

providers of credit support and fiduciary agents, <strong>to</strong> ensure that the probability that they will<br />

perform their duties is consistent with the rating on the transaction.<br />

STRUCTURAL AND LEGAL ELEMENTS<br />

Important structural elements which are assessed include: ownership of the SPC; allocation of<br />

funds between the different parties <strong>to</strong> the transaction; the SPC’s ability <strong>to</strong> issue additional debt in<br />

the future and under what conditions; the existence of performance triggers; covenants at the<br />

level of both the carrier and the SPC; events of default; the existence and terms of any corporate<br />

guarantees; and the existence and terms of other credit enhancement from a third party provider.<br />

For example, the existence of performance triggers can alert inves<strong>to</strong>rs <strong>to</strong> nascent problems and,<br />

depending on the terms of the transaction, can allow an early amortization of the transaction.<br />

Important protections <strong>to</strong> inves<strong>to</strong>rs in this type of securitization include the carrier’s obligation <strong>to</strong>:<br />

maintain specified minimum levels of collections on receivables; maintain a specified minimum<br />

number of weekly flights <strong>to</strong> and from those markets relevant <strong>to</strong> the transaction; comply with all<br />

transaction documents; maintain satisfac<strong>to</strong>ry relations with the account deb<strong>to</strong>rs; and compliance<br />

by the carrier with any specific financial and operational covenants. Other features which<br />

can enhance inves<strong>to</strong>r protection include the existence of early amortization events which can<br />

provide for an accelerated repayment of the securities if certain events occur.<br />

Moody’s assesses the enforceability of each party’s rights and obligations under the governing<br />

law of each transaction document, including submission <strong>to</strong> the jurisdiction of foreign courts,<br />

where appropriate; a waiver of sovereign immunity, if applicable; validity of the bondholders’<br />

security interest in the collateral.<br />

CONCLUSION: PIERCING THE CEILING IS POSSIBLE<br />

In Moody’s opinion, the ability of most sovereigns <strong>to</strong> interfere with the cash flow of a transaction<br />

backed by airline ticket receivables is extremely limited. These transactions are structured so<br />

that the receivables are generated electronically outside of the sovereign jurisdiction and by entities<br />

(the account deb<strong>to</strong>rs) also outside of the sovereign jurisdiction and whose obligation <strong>to</strong><br />

remit all funds <strong>to</strong> an offshore fiduciary agent acting on behalf of the bondholders is assumed<br />

under a foreign law. As a result, these cross-border structured finance transactions which<br />

depend on the settlement of international airline ticket receivables for payment of principal and<br />

interest frequently can often “pierce the country ceiling” and achieve a rating higher than the<br />

foreign currency country ceiling of the domicile of the carrier.<br />

These transactions may also achieve a rating higher than the unsecured local currency rating of<br />

the carrier if certain conditions exist, such as the ability <strong>to</strong> isolate the future receivables from the<br />

estate of the carrier in the event of its bankruptcy or the presence of specific regulations which<br />

limit a carrier’s ability <strong>to</strong> file for bankruptcy in its host country, and a qualitative assessment of the<br />

carrier’s his<strong>to</strong>rical relationship with the account deb<strong>to</strong>rs which indicates that the bankruptcy of<br />

the carrier would not result in an au<strong>to</strong>matic termination of its contracts with the account deb<strong>to</strong>rs.<br />

Moody’s <strong>Approach</strong> <strong>to</strong> <strong>Rating</strong> <strong>Obligations</strong> <strong>Backed</strong> by International Airline Ticket Receivables • 9

RELATED RESEARCH<br />

• “VARIG”, S.A. (Viacao Aerea Rio-Grandense) – RG Receivables Company, Ltd. – Moody’s<br />

Structured FInance, New Issue Report, April 3, 1998.<br />

• “Moody’s <strong>Approach</strong> <strong>to</strong> Structured Finance Transactions: Piercing the Foreign Currency<br />

Country Ceiling,” Moody’s Structured FInance, August 1997.<br />

• “Structured Finance Transactions <strong>Backed</strong> by Future Receivables,” Moody’s Structured<br />

Finance, February 27, 1998<br />

• “Structured Finance and Energy Project <strong>Rating</strong>s Demonstrate Stability Despite Sovereign<br />

<strong>Rating</strong> Actions,” Moody’s Structured Finance, Oc<strong>to</strong>ber 1998.<br />

10 •<br />

Moody’s <strong>Approach</strong> <strong>to</strong> <strong>Rating</strong> <strong>Obligations</strong> <strong>Backed</strong> by International Airline Ticket Receivables

Moody’s <strong>Approach</strong> <strong>to</strong> <strong>Rating</strong> <strong>Obligations</strong> <strong>Backed</strong> by International Airline Ticket Receivables • 11

© Copyright 1999 by Moody’s Inves<strong>to</strong>rs Service, Inc., 99 Church Street, New York, New York 10007.<br />

All rights reserved. ALL INFORMATION CONTAINED HEREIN IS COPYRIGHTED IN THE NAME OF MOODY’S INVESTORS SERVICE, INC. (“MOODY’S”), AND NONE OF SUCH INFORMATION MAY BE<br />

COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY<br />

SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT. All information<br />

contained herein is obtained by MOODY’S from sources believed by it <strong>to</strong> be accurate and reliable. Because of the possibility of human or mechanical error as well as other fac<strong>to</strong>rs, however, such information<br />

is provided “as is” without warranty of any kind and MOODY’S, in particular, makes no representation or warranty, express or implied, as <strong>to</strong> the accuracy, timeliness, completeness, merchantability or<br />

fitness for any particular purpose of any such information. Under no circumstances shall MOODY’S have any liability <strong>to</strong> any person or entity for (a) any loss or damage in whole or in part caused by, resulting<br />

from, or relating <strong>to</strong>, any error (negligent or otherwise) or other circumstance or contingency within or outside the control of MOODY’S or any of its direc<strong>to</strong>rs, officers, employees or agents in connection with<br />

the procurement, collection, compilation, analysis, interpretation, communication, publication or delivery of any such information, or (b) any direct, indirect, special, consequential, compensa<strong>to</strong>ry or incidental<br />

damages whatsoever (including without limitation, lost profits), even if MOODY’S is advised in advance of the possibility of such damages, resulting from the use of or inability <strong>to</strong> use, any such information.<br />

The credit ratings, if any, constituting part of the information contained herein are, and must be construed solely as, statements of opinion and not statements of fact or recommendations <strong>to</strong> purchase, sell<br />

or hold any securities. NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY<br />

SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER. Each rating or other opinion must be weighed solely as one<br />

fac<strong>to</strong>r in any investment decision made by or on behalf of any user of the information contained herein, and each such user must accordingly make its own study and evaluation of each security and of each<br />

issuer and guaran<strong>to</strong>r of, and each provider of credit support for, each security that it may consider purchasing, holding or selling. Pursuant <strong>to</strong> Section 17(b) of the Securities Act of 1933, MOODY’S<br />

hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred s<strong>to</strong>ck rated by MOODY’S have, prior <strong>to</strong><br />

assignment of any rating, agreed <strong>to</strong> pay <strong>to</strong> MOODY’S for appraisal and rating services rendered by it fees ranging from $1,000 <strong>to</strong> $1,500,000.<br />

12 •<br />

Moody’s <strong>Approach</strong> <strong>to</strong> <strong>Rating</strong> <strong>Obligations</strong> <strong>Backed</strong> by International Airline Ticket Receivables