Review of prices for the Water Administration Ministerial Corporation

Review of prices for the Water Administration Ministerial Corporation

Review of prices for the Water Administration Ministerial Corporation

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

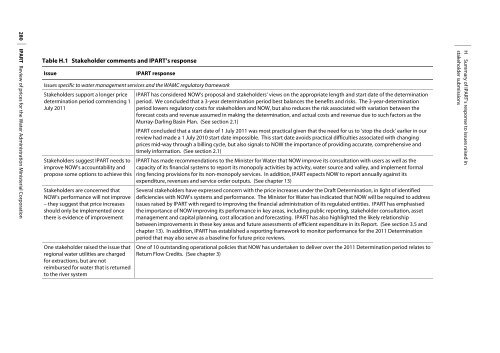

280 IPART <strong>Review</strong> <strong>of</strong> <strong>prices</strong> <strong>for</strong> <strong>the</strong> <strong>Water</strong> <strong>Administration</strong> <strong>Ministerial</strong> <strong>Corporation</strong><br />

Table H.1 Stakeholder comments and IPART’s response<br />

Issue<br />

IPART response<br />

Issues specific to water management services and <strong>the</strong> WAMC regulatory framework<br />

Stakeholders support a longer price<br />

determination period commencing 1<br />

July 2011<br />

Stakeholders suggest IPART needs to<br />

improve NOW’s accountability and<br />

propose some options to achieve this<br />

Stakeholders are concerned that<br />

NOW’s per<strong>for</strong>mance will not improve<br />

– <strong>the</strong>y suggest that price increases<br />

should only be implemented once<br />

<strong>the</strong>re is evidence <strong>of</strong> improvement<br />

One stakeholder raised <strong>the</strong> issue that<br />

regional water utilities are charged<br />

<strong>for</strong> extractions, but are not<br />

reimbursed <strong>for</strong> water that is returned<br />

to <strong>the</strong> river system<br />

IPART has considered NOW’s proposal and stakeholders’ views on <strong>the</strong> appropriate length and start date <strong>of</strong> <strong>the</strong> determination<br />

period. We concluded that a 3-year determination period best balances <strong>the</strong> benefits and risks. The 3-year-determination<br />

period lowers regulatory costs <strong>for</strong> stakeholders and NOW, but also reduces <strong>the</strong> risk associated with variation between <strong>the</strong><br />

<strong>for</strong>ecast costs and revenue assumed in making <strong>the</strong> determination, and actual costs and revenue due to such factors as <strong>the</strong><br />

Murray-Darling Basin Plan. (See section 2.1)<br />

IPART concluded that a start date <strong>of</strong> 1 July 2011 was most practical given that <strong>the</strong> need <strong>for</strong> us to ‘stop <strong>the</strong> clock’ earlier in our<br />

review had made a 1 July 2010 start date impossible. This start date avoids practical difficulties associated with changing<br />

<strong>prices</strong> mid-way through a billing cycle, but also signals to NOW <strong>the</strong> importance <strong>of</strong> providing accurate, comprehensive and<br />

timely in<strong>for</strong>mation. (See section 2.1)<br />

IPART has made recommendations to <strong>the</strong> Minister <strong>for</strong> <strong>Water</strong> that NOW improve its consultation with users as well as <strong>the</strong><br />

capacity <strong>of</strong> its financial systems to report its monopoly activities by activity, water source and valley, and implement <strong>for</strong>mal<br />

ring fencing provisions <strong>for</strong> its non-monopoly services. In addition, IPART expects NOW to report annually against its<br />

expenditure, revenues and service order outputs. (See chapter 13)<br />

Several stakeholders have expressed concern with <strong>the</strong> price increases under <strong>the</strong> Draft Determination, in light <strong>of</strong> identified<br />

deficiencies with NOW’s systems and per<strong>for</strong>mance. The Minister <strong>for</strong> <strong>Water</strong> has indicated that NOW will be required to address<br />

issues raised by IPART with regard to improving <strong>the</strong> financial administration <strong>of</strong> its regulated entities. IPART has emphasised<br />

<strong>the</strong> importance <strong>of</strong> NOW improving its per<strong>for</strong>mance in key areas, including public reporting, stakeholder consultation, asset<br />

management and capital planning, cost allocation and <strong>for</strong>ecasting. IPART has also highlighted <strong>the</strong> likely relationship<br />

between improvements in <strong>the</strong>se key areas and future assessments <strong>of</strong> efficient expenditure in its Report. (See section 3.5 and<br />

chapter 13). In addition, IPART has established a reporting framework to monitor per<strong>for</strong>mance <strong>for</strong> <strong>the</strong> 2011 Determination<br />

period that may also serve as a baseline <strong>for</strong> future price reviews.<br />

One <strong>of</strong> 10 outstanding operational policies that NOW has undertaken to deliver over <strong>the</strong> 2011 Determination period relates to<br />

Return Flow Credits. (See chapter 3)<br />

H Summary <strong>of</strong> IPART’s response to issues raised in<br />

stakeholder submissions