Risk 1 - Hans Buehler

Risk 1 - Hans Buehler

Risk 1 - Hans Buehler

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

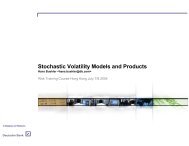

Implied Vol<br />

8346<br />

9737<br />

11128<br />

12519<br />

13910<br />

15301<br />

16692<br />

18083<br />

19474<br />

Modeling <strong>Risk</strong> – Local Volatility<br />

Black & Scholes – Implied Volatility<br />

• Using the BS volatility s BS as a free parameter, we can invert the BS<br />

formula to back out the so-called ―BS implied volatility‖ surface of the<br />

Market<br />

market.<br />

70%<br />

60%<br />

50%<br />

40%<br />

30%<br />

1Y<br />

2Y<br />

3Y<br />

3M<br />

Strike<br />

Example: HSI Mar 25, 2009 @ 13,910<br />

23