Risk 1 - Hans Buehler

Risk 1 - Hans Buehler

Risk 1 - Hans Buehler

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

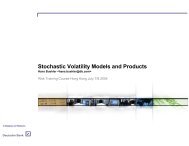

Modeling <strong>Risk</strong> – Basics<br />

Black & Scholes<br />

• For this particular choice, the SDE has the analytical solution<br />

S<br />

BS<br />

1 2 <br />

( t)<br />

= F(<br />

t)exp<br />

s<br />

BSW<br />

( t)<br />

s<br />

BS<br />

t<br />

2 <br />

which allows computing vanilla option prices and, indeed, many more<br />

option prices analytically.<br />

The famous Black&Scholes formula for the value of an European call is:<br />

FV( T,Stoday)<br />

: =<br />

DF( T)<br />

= DF( T)<br />

E<br />

<br />

<br />

<br />

S<br />

BS<br />

( T)<br />

K<br />

F(T)N ( d<br />

<br />

<br />

<br />

<br />

) KN(<br />

d<br />

<br />

) <br />

d<br />

<br />

=<br />

ln( F(<br />

T) / K)<br />

<br />

s<br />

BS<br />

T<br />

1<br />

2<br />

s 2<br />

BS<br />

T<br />

7