Risk 1 - Hans Buehler

Risk 1 - Hans Buehler

Risk 1 - Hans Buehler

SHOW LESS

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

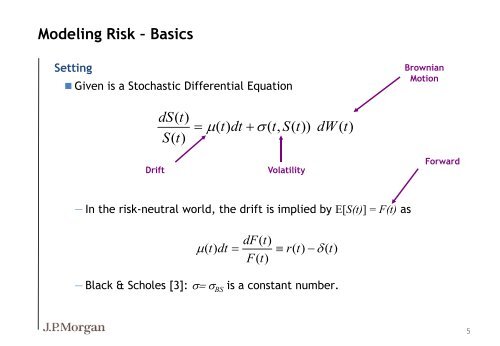

Modeling <strong>Risk</strong> – Basics<br />

Setting<br />

• Given is a Stochastic Differential Equation<br />

Brownian<br />

Motion<br />

dS(<br />

t)<br />

S(<br />

t)<br />

= (<br />

t)<br />

dt s ( t,<br />

S(<br />

t))<br />

dW ( t)<br />

Drift<br />

Volatility<br />

Forward<br />

— In the risk-neutral world, the drift is implied by E[S(t)] = F(t) as<br />

dF(<br />

t)<br />

( t)<br />

dt = r(<br />

t)<br />

<br />

( t)<br />

F(<br />

t)<br />

— Black & Scholes [3]: s= s BS is a constant number.<br />

5