Exam fm sample questions - Society of Actuaries

Exam fm sample questions - Society of Actuaries

Exam fm sample questions - Society of Actuaries

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

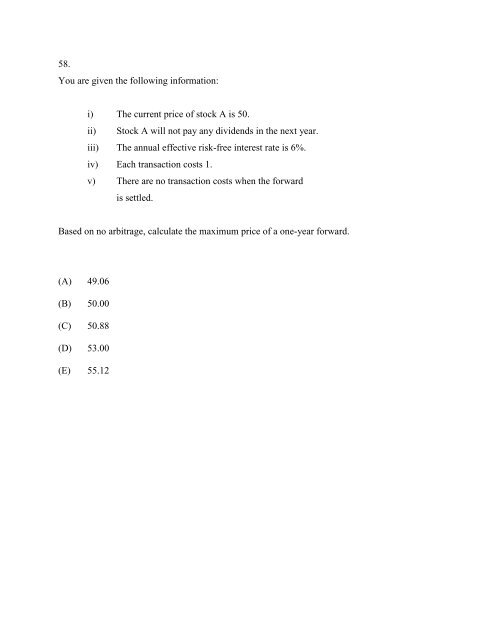

58.<br />

You are given the following information:<br />

i) The current price <strong>of</strong> stock A is 50.<br />

ii) Stock A will not pay any dividends in the next year.<br />

iii) The annual effective risk-free interest rate is 6%.<br />

iv) Each transaction costs 1.<br />

v) There are no transaction costs when the forward<br />

is settled.<br />

Based on no arbitrage, calculate the maximum price <strong>of</strong> a one-year forward.<br />

(A) 49.06<br />

(B) 50.00<br />

(C) 50.88<br />

(D) 53.00<br />

(E) 55.12