ABN AMRO Capital Funding Trust V ABN AMRO Holding N.V.

ABN AMRO Capital Funding Trust V ABN AMRO Holding N.V.

ABN AMRO Capital Funding Trust V ABN AMRO Holding N.V.

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

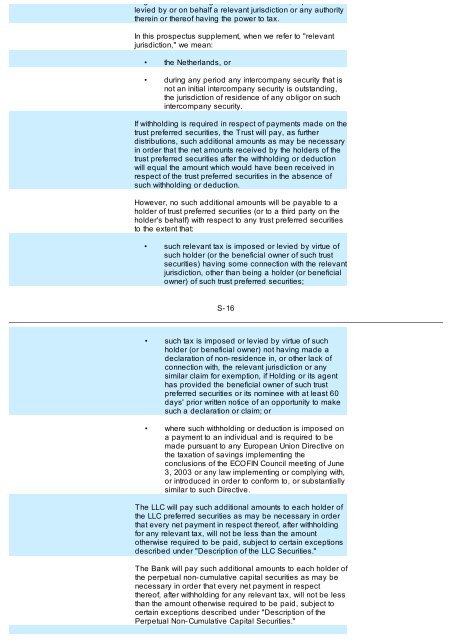

or governmental charges of whatever nature, imposed or<br />

levied by or on behalf a relevant jurisdiction or any authority<br />

therein or thereof having the power to tax.<br />

In this prospectus supplement, when we refer to "relevant<br />

jurisdiction," we mean:<br />

• the Netherlands, or<br />

• during any period any intercompany security that is<br />

not an initial intercompany security is outstanding,<br />

the jurisdiction of residence of any obligor on such<br />

intercompany security.<br />

If withholding is required in respect of payments made on the<br />

trust preferred securities, the <strong>Trust</strong> will pay, as further<br />

distributions, such additional amounts as may be necessary<br />

in order that the net amounts received by the holders of the<br />

trust preferred securities after the withholding or deduction<br />

will equal the amount which would have been received in<br />

respect of the trust preferred securities in the absence of<br />

such withholding or deduction.<br />

However, no such additional amounts will be payable to a<br />

holder of trust preferred securities (or to a third party on the<br />

holder's behalf) with respect to any trust preferred securities<br />

to the extent that:<br />

• such relevant tax is imposed or levied by virtue of<br />

such holder (or the beneficial owner of such trust<br />

securities) having some connection with the relevant<br />

jurisdiction, other than being a holder (or beneficial<br />

owner) of such trust preferred securities;<br />

S- 16<br />

• such tax is imposed or levied by virtue of such<br />

holder (or beneficial owner) not having made a<br />

declaration of non- residence in, or other lack of<br />

connection with, the relevant jurisdiction or any<br />

similar claim for exemption, if <strong>Holding</strong> or its agent<br />

has provided the beneficial owner of such trust<br />

preferred securities or its nominee with at least 60<br />

days' prior written notice of an opportunity to make<br />

such a declaration or claim; or<br />

• where such withholding or deduction is imposed on<br />

a payment to an individual and is required to be<br />

made pursuant to any European Union Directive on<br />

the taxation of savings implementing the<br />

conclusions of the ECOFIN Council meeting of June<br />

3, 2003 or any law implementing or complying with,<br />

or introduced in order to conform to, or substantially<br />

similar to such Directive.<br />

The LLC will pay such additional amounts to each holder of<br />

the LLC preferred securities as may be necessary in order<br />

that every net payment in respect thereof, after withholding<br />

for any relevant tax, will not be less than the amount<br />

otherwise required to be paid, subject to certain exceptions<br />

described under "Description of the LLC Securities."<br />

The Bank will pay such additional amounts to each holder of<br />

the perpetual non- cumulative capital securities as may be<br />

necessary in order that every net payment in respect<br />

thereof, after withholding for any relevant tax, will not be less<br />

than the amount otherwise required to be paid, subject to<br />

certain exceptions described under "Description of the<br />

Perpetual Non- Cumulative <strong>Capital</strong> Securities."