ANNUAL REPORT 2005 - British Aerosol Manufacturers' Association

ANNUAL REPORT 2005 - British Aerosol Manufacturers' Association

ANNUAL REPORT 2005 - British Aerosol Manufacturers' Association

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

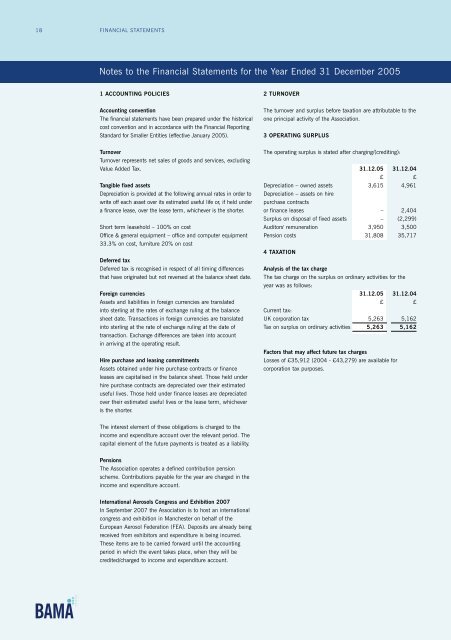

18 FINANCIAL STATEMENTS<br />

Notes to the Financial Statements for the Year Ended 31 December <strong>2005</strong><br />

1 ACCOUNTING POLICIES<br />

2 TURNOVER<br />

Accounting convention<br />

The financial statements have been prepared under the historical<br />

cost convention and in accordance with the Financial Reporting<br />

Standard for Smaller Entities (effective January <strong>2005</strong>).<br />

The turnover and surplus before taxation are attributable to the<br />

one principal activity of the <strong>Association</strong>.<br />

3 OPERATING SURPLUS<br />

Turnover<br />

Turnover represents net sales of goods and services, excluding<br />

Value Added Tax.<br />

Tangible fixed assets<br />

Depreciation is provided at the following annual rates in order to<br />

write off each asset over its estimated useful life or, if held under<br />

a finance lease, over the lease term, whichever is the shorter.<br />

Short term leasehold – 100% on cost<br />

Office & general equipment – office and computer equipment<br />

33.3% on cost, furniture 20% on cost<br />

Deferred tax<br />

Deferred tax is recognised in respect of all timing differences<br />

that have originated but not reversed at the balance sheet date.<br />

Foreign currencies<br />

Assets and liabilities in foreign currencies are translated<br />

into sterling at the rates of exchange ruling at the balance<br />

sheet date. Transactions in foreign currencies are translated<br />

into sterling at the rate of exchange ruling at the date of<br />

transaction. Exchange differences are taken into account<br />

in arriving at the operating result.<br />

Hire purchase and leasing commitments<br />

Assets obtained under hire purchase contracts or finance<br />

leases are capitalised in the balance sheet. Those held under<br />

hire purchase contracts are depreciated over their estimated<br />

useful lives. Those held under finance leases are depreciated<br />

over their estimated useful lives or the lease term, whichever<br />

is the shorter.<br />

The operating surplus is stated after charging/(crediting):<br />

31.12.05 31.12.04<br />

£ £<br />

Depreciation – owned assets 3,615 4,961<br />

Depreciation – assets on hire<br />

purchase contracts<br />

or finance leases – 2,404<br />

Surplus on disposal of fixed assets – (2,299)<br />

Auditors' remuneration 3,950 3,500<br />

Pension costs 31,808 35,717<br />

4 TAXATION<br />

Analysis of the tax charge<br />

The tax charge on the surplus on ordinary activities for the<br />

year was as follows:<br />

31.12.05 31.12.04<br />

£ £<br />

Current tax:<br />

UK corporation tax 5,263 5,162<br />

Tax on surplus on ordinary activities 5,263 5,162<br />

Factors that may affect future tax charges<br />

Losses of £35,912 (2004 - £43,279) are available for<br />

corporation tax purposes.<br />

The interest element of these obligations is charged to the<br />

income and expenditure account over the relevant period. The<br />

capital element of the future payments is treated as a liability.<br />

Pensions<br />

The <strong>Association</strong> operates a defined contribution pension<br />

scheme. Contributions payable for the year are charged in the<br />

income and expenditure account.<br />

International <strong>Aerosol</strong>s Congress and Exhibition 2007<br />

In September 2007 the <strong>Association</strong> is to host an international<br />

congress and exhibition in Manchester on behalf of the<br />

European <strong>Aerosol</strong> Federation (FEA). Deposits are already being<br />

received from exhibitors and expenditure is being incurred.<br />

These items are to be carried forward until the accounting<br />

period in which the event takes place, when they will be<br />

credited/charged to income and expenditure account.