Research & Development for Ceramic Tiles in the 21st ... - Infotile

Research & Development for Ceramic Tiles in the 21st ... - Infotile

Research & Development for Ceramic Tiles in the 21st ... - Infotile

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

nowadays, <strong>the</strong> sector has a<br />

more or less homogenous<br />

character <strong>in</strong> which <strong>the</strong><br />

different companies tend<br />

to produce very similar materials and<br />

<strong>the</strong>re<strong>for</strong>e compete <strong>for</strong> <strong>the</strong> same market.<br />

This paper proposes two alternative<br />

but compatible road maps that provide<br />

a possible future strategy to diversify<br />

<strong>the</strong> sector’s supply offer by plann<strong>in</strong>g<br />

its R&D+i to: i) achieve significant<br />

production cost sav<strong>in</strong>gs <strong>for</strong> standard<br />

ceramic products, and ii) to develop<br />

new specialised ceramic materials<br />

that meet <strong>the</strong> specific cultural and<br />

practical needs of each particular market<br />

environment. In <strong>the</strong> short term, <strong>the</strong><br />

ideal strategy would be to develop <strong>the</strong><br />

first alternative <strong>in</strong> order to produce<br />

ceramic bodies at significantly lower<br />

fir<strong>in</strong>g temperatures than at present,<br />

<strong>the</strong> immediate effect of which would<br />

be to reduce glaze thickness<br />

and <strong>the</strong> amount and size of<br />

pigment particles, <strong>the</strong>reby<br />

open<strong>in</strong>g <strong>the</strong> way to mass<br />

usage of th<strong>in</strong>-film decorat<strong>in</strong>g<br />

techniques (such as <strong>in</strong>k<br />

jets) and even laser techniques.<br />

In <strong>the</strong> medium and<br />

long term, <strong>the</strong> second alternative<br />

needs to be followed,<br />

to <strong>in</strong>crease <strong>the</strong> overall added<br />

value of ceramic tiles, which<br />

depends on <strong>the</strong> skills and <strong>in</strong>genuity<br />

of researchers and<br />

technicians alike to come up<br />

with a wide-rang<strong>in</strong>g diversity<br />

of ceramic products.<br />

<strong>in</strong>troduction<br />

When one analyses <strong>the</strong> relative significance<br />

of <strong>the</strong> role played by classic<br />

ceramic (CC) materials (traditional<br />

ceramics: floor and wall tiles, bricks,<br />

refractory materials, tableware and ceramic<br />

bathroom fitt<strong>in</strong>gs, etc. that basically<br />

attend primary human needs,<br />

especially home-build<strong>in</strong>g needs) and<br />

advanced ceramic (AC) materials (or<br />

technical ceramics, which apparently<br />

ma<strong>in</strong>ly refers to materials cover<strong>in</strong>g<br />

secondary human needs, e.g.<br />

<strong>in</strong> telecommunications), <strong>the</strong> world of<br />

ceramics seems to be “two headed”,<br />

“tw<strong>in</strong>-moded” and “asymmetrical”. It<br />

is tw<strong>in</strong>-headed <strong>in</strong> <strong>the</strong> sense that researchers<br />

tend to choose to devote<br />

<strong>the</strong>ir professional skills to ei<strong>the</strong>r CC<br />

or AC. It is “tw<strong>in</strong>-moded” <strong>in</strong> <strong>the</strong> sense<br />

that its manufactur<strong>in</strong>g companies, and<br />

even producer countries, also tend to<br />

opt <strong>for</strong> ei<strong>the</strong>r CC or AC. Never<strong>the</strong>less,<br />

<strong>the</strong> sector is also highly asymmetrical,<br />

<strong>in</strong> that <strong>the</strong> number of publications<br />

and concerted research devoted to CC<br />

is much lower than <strong>for</strong> AC, although<br />

turnover <strong>in</strong> economic terms is much<br />

higher worldwide <strong>for</strong> CC than <strong>for</strong> AC.<br />

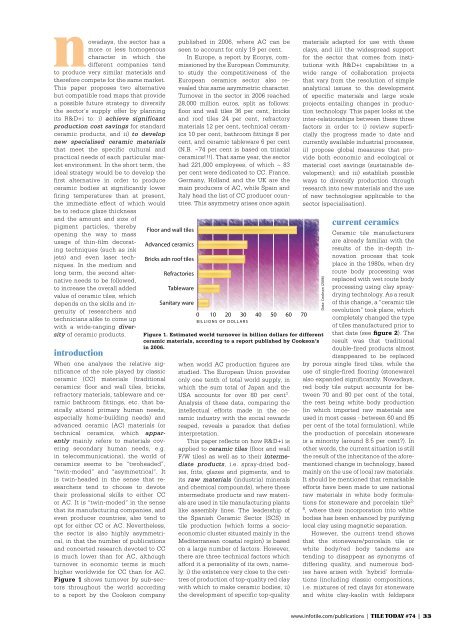

Figure 1 shows turnover by sub-sectors<br />

throughout <strong>the</strong> world accord<strong>in</strong>g<br />

to a report by <strong>the</strong> Cookson company<br />

Floor and wall tiles<br />

Advanced ceramics<br />

Bricks adn roof tiles<br />

published <strong>in</strong> 2006, where AC can be<br />

seen to account <strong>for</strong> only 19 per cent.<br />

In Europe, a report by Ecorys, commissioned<br />

by <strong>the</strong> European Community,<br />

to study <strong>the</strong> competitiveness of <strong>the</strong><br />

European ceramics sector also revealed<br />

this same asymmetric character.<br />

Turnover <strong>in</strong> <strong>the</strong> sector <strong>in</strong> 2006 reached<br />

28,000 million euros, split as follows:<br />

floor and wall tiles 36 per cent, bricks<br />

and roof tiles 24 per cent, refractory<br />

materials 12 per cent, technical ceramics<br />

10 per cent, bathroom fitt<strong>in</strong>gs 8 per<br />

cent, and ceramic tableware 6 per cent<br />

(N.B. ~74 per cent is based on triaxial<br />

ceramics!!!). That same year, <strong>the</strong> sector<br />

had 221,000 employees, of which ~ 83<br />

per cent were dedicated to CC. France,<br />

Germany, Holland and <strong>the</strong> UK are <strong>the</strong><br />

ma<strong>in</strong> producers of AC, while Spa<strong>in</strong> and<br />

Italy head <strong>the</strong> list of CC producer countries.<br />

This asymmetry arises once aga<strong>in</strong><br />

Refractories<br />

Tableware<br />

Sanitary ware<br />

0 10 20 30 40 50 60 70<br />

BILLIONS OF DOLLARS<br />

Figure 1. Estimated world turnover <strong>in</strong> billion dollars <strong>for</strong> different<br />

ceramic materials, accord<strong>in</strong>g to a report published by Cookson’s<br />

<strong>in</strong> 2006.<br />

when world AC production figures are<br />

studied. The European Union provides<br />

only one tenth of total world supply, <strong>in</strong><br />

which <strong>the</strong> sum total of Japan and <strong>the</strong><br />

USA accounts <strong>for</strong> over 80 per cent 1 .<br />

Analysis of <strong>the</strong>se data, compar<strong>in</strong>g <strong>the</strong><br />

<strong>in</strong>tellectual ef<strong>for</strong>ts made <strong>in</strong> <strong>the</strong> ceramic<br />

<strong>in</strong>dustry with <strong>the</strong> social rewards<br />

reaped, reveals a paradox that defies<br />

<strong>in</strong>terpretation.<br />

This paper reflects on how R&D+i is<br />

applied to ceramic tiles (floor and wall<br />

F/W tiles) as well as to <strong>the</strong>ir <strong>in</strong>termediate<br />

products, i.e. spray-dried bodies,<br />

frits, glazes and pigments, and to<br />

its raw materials (<strong>in</strong>dustrial m<strong>in</strong>erals<br />

and chemical compounds), where <strong>the</strong>se<br />

<strong>in</strong>termediate products and raw materials<br />

are used <strong>in</strong> tile manufactur<strong>in</strong>g plants<br />

like assembly l<strong>in</strong>es. The leadership of<br />

<strong>the</strong> Spanish <strong>Ceramic</strong> Sector (SCS) <strong>in</strong><br />

tile production (which <strong>for</strong>ms a socioeconomic<br />

cluster situated ma<strong>in</strong>ly <strong>in</strong> <strong>the</strong><br />

Mediterranean coastal region) is based<br />

on a large number of factors. However,<br />

<strong>the</strong>re are three technical factors which<br />

af<strong>for</strong>d it a personality of its own, namely:<br />

i) <strong>the</strong> existence very close to <strong>the</strong> centres<br />

of production of top-quality red clay<br />

with which to make ceramic bodies, ii)<br />

<strong>the</strong> development of specific top-quality<br />

materials adapted <strong>for</strong> use with <strong>the</strong>se<br />

clays, and iii) <strong>the</strong> widespread support<br />

<strong>for</strong> <strong>the</strong> sector that comes from <strong>in</strong>stitutions<br />

with R&D+i capabilities <strong>in</strong> a<br />

wide range of collaboration projects<br />

that vary from <strong>the</strong> resolution of simple<br />

analytical issues to <strong>the</strong> development<br />

of specific materials and large scale<br />

projects entail<strong>in</strong>g changes <strong>in</strong> production<br />

technology. This paper looks at <strong>the</strong><br />

<strong>in</strong>ter-relationships between <strong>the</strong>se three<br />

factors <strong>in</strong> order to: i) review superficially<br />

<strong>the</strong> progress made to date and<br />

currently available <strong>in</strong>dustrial processes,<br />

ii) propose global measures that provide<br />

both economic and ecological or<br />

material cost sav<strong>in</strong>gs (susta<strong>in</strong>able development);<br />

and iii) establish possible<br />

ways to diversify production through<br />

research <strong>in</strong>to new materials and <strong>the</strong> use<br />

of new technologies applicable to <strong>the</strong><br />

sector (specialisation).<br />

Data: Cookson (2006)<br />

current ceramics<br />

<strong>Ceramic</strong> tile manufacturers<br />

are already familiar with <strong>the</strong><br />

results of <strong>the</strong> <strong>in</strong>-depth <strong>in</strong>novation<br />

process that took<br />

place <strong>in</strong> <strong>the</strong> 1980s, when dry<br />

route body process<strong>in</strong>g was<br />

replaced with wet route body<br />

process<strong>in</strong>g us<strong>in</strong>g clay spraydry<strong>in</strong>g<br />

technology. As a result<br />

of this change, a “ceramic tile<br />

revolution” took place, which<br />

completely changed <strong>the</strong> type<br />

of tiles manufactured prior to<br />

that date (see figure 2). The<br />

result was that traditional<br />

double-fired products almost<br />

disappeared to be replaced<br />

by porous s<strong>in</strong>gle fired tiles, while <strong>the</strong><br />

use of s<strong>in</strong>gle-fired floor<strong>in</strong>g (stoneware)<br />

also expanded significantly. Nowadays,<br />

red body tile output accounts <strong>for</strong> between<br />

70 and 80 per cent of <strong>the</strong> total,<br />

<strong>the</strong> rest be<strong>in</strong>g white body production<br />

(<strong>in</strong> which imported raw materials are<br />

used <strong>in</strong> most cases - between 60 and 85<br />

per cent of <strong>the</strong> total <strong>for</strong>mulation), while<br />

<strong>the</strong> production of porcela<strong>in</strong> stoneware<br />

is a m<strong>in</strong>ority (around 8.5 per cent). In<br />

o<strong>the</strong>r words, <strong>the</strong> current situation is still<br />

<strong>the</strong> result of <strong>the</strong> <strong>in</strong>heritance of <strong>the</strong> a<strong>for</strong>ementioned<br />

change <strong>in</strong> technology, based<br />

ma<strong>in</strong>ly on <strong>the</strong> use of local raw materials.<br />

It should be mentioned that remarkable<br />

ef<strong>for</strong>ts have been made to use national<br />

raw materials <strong>in</strong> white body <strong>for</strong>mulations<br />

<strong>for</strong> stoneware and porcela<strong>in</strong> tile 2-<br />

6 , where <strong>the</strong>ir <strong>in</strong>corporation <strong>in</strong>to white<br />

bodies has been enhanced by purify<strong>in</strong>g<br />

local clay us<strong>in</strong>g magnetic separation.<br />

However, <strong>the</strong> current trend shows<br />

that <strong>the</strong> stoneware/porcela<strong>in</strong> tile or<br />

white body/red body tandems are<br />

tend<strong>in</strong>g to disappear as synonyms of<br />

differ<strong>in</strong>g quality, and numerous bodies<br />

have arisen with ‘hybrid’ <strong>for</strong>mulations<br />

(<strong>in</strong>clud<strong>in</strong>g classic compositions,<br />

i.e. mixtures of red clays <strong>for</strong> stoneware<br />

and white clay-kaol<strong>in</strong> with feldspars<br />

www.<strong>in</strong>fotile.com/publications | Tile Today #74 | 33