THE INSTITUTE OF CHARTERED ACCOUNTANTS ... - Resourcedat

THE INSTITUTE OF CHARTERED ACCOUNTANTS ... - Resourcedat

THE INSTITUTE OF CHARTERED ACCOUNTANTS ... - Resourcedat

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

PATHFINDER<br />

- File the returns to Corporate Affairs Commission<br />

ii.<br />

The Investment & Securities Acts (ISA) 1999 requires every security dealer to<br />

keep adequate records and account of its transactions from time to time.<br />

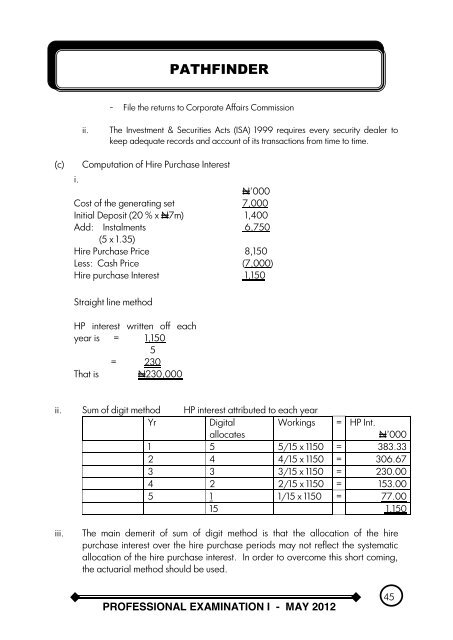

(c)<br />

Computation of Hire Purchase Interest<br />

i.<br />

N’000<br />

Cost of the generating set 7,000<br />

Initial Deposit (20 % x N7m) 1,400<br />

Add: Instalments<br />

6,750<br />

(5 x 1.35)<br />

Hire Purchase Price 8,150<br />

Less: Cash Price (7,000)<br />

Hire purchase Interest 1,150<br />

Straight line method<br />

HP interest written off each<br />

year is = 1,150<br />

5<br />

= 230<br />

That is N230,000<br />

ii. Sum of digit method HP interest attributed to each year<br />

Yr<br />

Digital Workings = HP Int.<br />

allocates<br />

N’000<br />

1 5 5/15 x 1150 = 383.33<br />

2 4 4/15 x 1150 = 306.67<br />

3 3 3/15 x 1150 = 230.00<br />

4 2 2/15 x 1150 = 153.00<br />

5 1 1/15 x 1150 = 77.00<br />

15 1,150<br />

iii.<br />

The main demerit of sum of digit method is that the allocation of the hire<br />

purchase interest over the hire purchase periods may not reflect the systematic<br />

allocation of the hire purchase interest. In order to overcome this short coming,<br />

the actuarial method should be used.<br />

PR<strong>OF</strong>ESSIONAL EXAMINATION I - MAY 2012<br />

45