child support 101/102 - The Gitlin Law Firm

child support 101/102 - The Gitlin Law Firm

child support 101/102 - The Gitlin Law Firm

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

the Supreme Court’s decision stated:<br />

“<strong>The</strong> Supreme Court could have easily decided to refuse to take cert<br />

on this case. <strong>The</strong>y probably accepted cert knowing that there was a<br />

division among the districts and wanting to clear up the issue.<br />

Unfortunately, after accepting cert and reviewing the record, they<br />

learned that there was nothing to state the nature of the depreciation<br />

expense. Being a conservative judiciary, the court did the proper<br />

thing and refused to suggest by way of broad dictum that had the<br />

expense been justified as reasonable and necessary that the expense<br />

would have been allowed.”<br />

By way of example, Nelson held that the <strong>child</strong> <strong>support</strong> payor was not allowed to deduct farm<br />

equipment depreciation from his net income because he failed to show the expense was an<br />

"expenditure for the repayment of debt." It further held that the <strong>child</strong> <strong>support</strong> payor was not allowed<br />

to deduct payments toward farm operating loan principal from his net income because allowing the<br />

deduction would have permitted the payor use of the same deduction twice.<br />

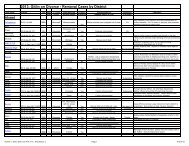

2. Quantification: Attached are two spreadsheets analyzing certain issues according<br />

to the relevant factors in the statutory and case law. <strong>The</strong> first spreadsheet analyzes<br />

the depreciation elements of the cases and the significant factors. <strong>The</strong> second<br />

spreadsheet analyzes the business expense cases (non-depreciation cases) and the<br />

significant factors.<br />

One opinion, Gay on Behalf of Gay v. Dunlap, is divided into two parts because the determination<br />

of one expense was remanded to the trial court. <strong>The</strong> remainder of the expenses were not allowed.<br />

<strong>The</strong> column regarding "Expense Allowed" refers to those cases in which the expense was ultimately<br />

allowed as a deductible reasonable and necessary business expense as an end result. This includes<br />

cases where the expense was allowed at the trial court level and the result was affirmed, and cases<br />

where the trial court did not allow the expense but there was a reversal.<br />

<strong>The</strong> taxpayer type is not always clear from the opinion. Where it appears relatively clear, the<br />

taxpayer type is set forth. It is clear from the spreadsheet that in most cases the taxpayer is a<br />

Schedule C taxpayer. In only one case was the business incorporated: IRMO Heil. It is probably<br />

not coincidental that this is one of the few cases where at least a portion of the expense was allowed<br />

as a reasonable and necessary business expense.<br />

3. Flowchart re Depreciation Cases: <strong>The</strong> IRMO Davis case presents what can be<br />

illustrated via a flow chart regarding depreciation cases. Note, however, that<br />

especially in light of the Illinois Supreme Court’s Minear case as well as the recent<br />

Worrall case, it appears that the law is not at all fixed as to whether there is an<br />

emphasis on proof of a debt repayment schedule.<br />

a. Debt Repayment Schedule: First determine if there is a debt<br />

repayment schedule.<br />

a. If no Generally non-deductible (but issue not<br />

definitely resolved per Minear/ Worrall)<br />

b. If yes Go to step b.<br />

<strong>Gitlin</strong> <strong>Law</strong> <strong>Firm</strong>, P.C. 1-32 www.gitlinlawfirm.com