pdf (5.0 MB) - Metro Group

pdf (5.0 MB) - Metro Group

pdf (5.0 MB) - Metro Group

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

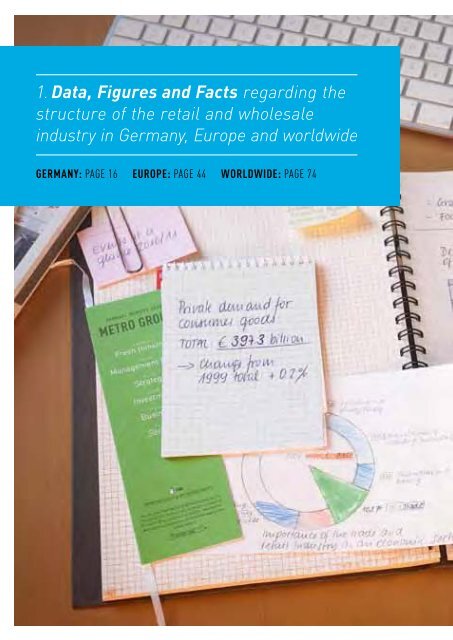

1. Data, Figures and Facts regarding the<br />

structure of the retail and wholesale<br />

industry in Germany, Europe and worldwide<br />

germany: paGE 16 EUROPe: paGE 44 worldwide: paGE 74

1. Data, Figures and Facts

Data, Figures and Facts<br />

p. 016 Germany<br />

Importance of the retail and wholesale<br />

industry as an economic sector<br />

Gross value added in € billion<br />

Public and private<br />

service providers<br />

517.5<br />

17.4 Agriculture and<br />

forestry, fishery<br />

474.7<br />

Manufacturing<br />

(excluding construction)<br />

2009 total: €2,152 bn.<br />

97.8<br />

Construction<br />

and housing<br />

Source: Federal Statistical Office Germany<br />

Financing, leasing and<br />

business service<br />

providers<br />

668.9<br />

158.0<br />

10.2%<br />

218.6 Wholesale<br />

and retail trade<br />

Hotels and restaurants,<br />

transport and communication<br />

The retail and wholesale industry makes a major contribution to the value added.<br />

METro rETail CoMPEnDIUM 2010/2011

p. 017 Germany<br />

Breakdown of private household consumption<br />

expenses in Germany, 1999 – 2009<br />

Private household consumption in percent (nominal)<br />

1. Data, Figures and Facts<br />

1999 2004 2009<br />

16.0<br />

17.5<br />

17.2<br />

Others (e.g. health, education,<br />

personal hygiene, financial services)<br />

23.1<br />

23.7<br />

24.4<br />

Housing, water, energy<br />

16.3<br />

17.0<br />

17.1<br />

Transport and communication<br />

Source: Federal Statistical Office Germany<br />

10.0<br />

5.6<br />

13.9<br />

15.1<br />

9.5<br />

5.4<br />

12.3<br />

14.7<br />

9.3<br />

5.6<br />

11.9<br />

14.4<br />

Leisure time, entertainment and culture<br />

Accomodation and restaurant services<br />

Textiles, furniture, household appliances and others<br />

Food and beverages, tobacco and others<br />

The proportion of expenditure on housing, water and energy has been increasing for several<br />

years at the expense of other consumer goods segments.<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 018 Germany<br />

Development of demand for consumer goods<br />

and the share in private consumption<br />

Market volume in € billion<br />

1993 94 95 96 97 98 99 2000 01 02 03 04 05 06<br />

07 08 09<br />

Sources: FERI, Federal Statistical Office Germany, METRO GROUP; as of July 2010<br />

387 390 390 389 388 394 398 405 401 391 388 385 386 391 396 403 397<br />

39.2<br />

Anteil am privaten Konsum in%<br />

28.2<br />

k Share of private consumption in %<br />

40%<br />

30%<br />

20%<br />

10%<br />

The volume of private demand for consumer goods has largely stagnated at early 1990s<br />

levels. At the same time, the demand for consumer goods as a share of overall private<br />

consumption is sinking.<br />

METro rETail CoMPEnDIUM 2010/2011

p. 019 Germany<br />

Development of private demand for food<br />

and nonfood consumer goods, 1999 – 2009<br />

Change in percent (nominal)<br />

1. Data, Figures and Facts<br />

Food<br />

Nonfood<br />

Total<br />

+ 10%<br />

+ 8%<br />

9.2<br />

+ 6%<br />

+ 4%<br />

+ 2%<br />

0%<br />

– 2%<br />

– 0.2<br />

Sources: BBE, METRO GROUP<br />

– 4%<br />

– 6%<br />

– 8%<br />

– 7.6<br />

With an overall stagnation in private demand for consumer goods, developments have varied<br />

in the food and nonfood segments. An increase in consumer demand for food is counterbalanced<br />

by declines in the nonfood segment.<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 020 Germany<br />

Private demand broken down by<br />

consumer goods groups, 2009<br />

Share in percent<br />

5.2 Games, sports, leisure time<br />

5.4 Furniture<br />

6.0 Tobacco<br />

5.1 Cleaning, hygiene, cosmetics<br />

3.3 Individual demand<br />

3.1 Entertainment electronics,<br />

image and sound carriers<br />

Office supplies,<br />

computers,<br />

telecommunications<br />

DIY, home improvement<br />

8.9<br />

9.6<br />

Total: €397.3 billion<br />

2.3 Electrical appliances,<br />

lamps, lighting fixtures<br />

1.2 Home appliance,<br />

glass, china<br />

Sources: BBE, METRO GROUP<br />

Textiles, garments, shoes<br />

10.8<br />

39.1 Food and beverages<br />

Foods and beverages, with a 40 percent share of private demand, represent the biggest<br />

segment of demand for consumer goods.<br />

METro rETail CoMPEnDIUM 2010/2011

p. 021 Germany<br />

Private demand broken down by<br />

consumer goods groups, 2009<br />

Spending in € billion<br />

Total: €397.3 bn.<br />

Change from 1999 total: – 0.2%<br />

1. Data, Figures and Facts<br />

Food and beverages<br />

155.1<br />

Textiles, garments, shoes<br />

DIY, home improvement<br />

Games, sports,<br />

leisure time<br />

Home appliance,<br />

glass, china<br />

Office supplies, computers,<br />

telecommunications<br />

Tobacco goods<br />

Furniture<br />

Cleaning, hygiene, cosmetics<br />

Accessories<br />

Entertainment electronics,<br />

image and sound carriers<br />

42.9<br />

37.9 35.4<br />

Electrical appliances,<br />

lamps, lighting fixtures<br />

23.6 21.4 20.5 20.4<br />

12.9 12.4<br />

9.2<br />

4.8<br />

Sources: BBE, METRO GROUP<br />

1<br />

+ 9.1<br />

5<br />

– 16.6<br />

5<br />

– 0.6<br />

5<br />

– 4.4<br />

1<br />

+ 12.4<br />

5<br />

– 22.6<br />

5<br />

– 6.2<br />

1<br />

+ 28.9<br />

k Change from 1999 in %<br />

1<br />

+ 2.1<br />

1<br />

+ 5.6<br />

5<br />

– 2.3<br />

5<br />

– 19.5<br />

The individual consumer goods segments show highly uneven development. Significant<br />

declines in demand in areas such as textiles, furniture and home appliance are counterbalanced<br />

by growth in other areas.<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 022 Germany<br />

Trends in private demand for<br />

consumer goods, 2006 – 2009<br />

Food/FMCG¹<br />

Change in percent<br />

Paper towels, sanitary paper 10.3<br />

Washing, cleaning agents 6.5<br />

Food and beverages 4.6<br />

– 0.1 Tobacco<br />

– 1.7 Flowers, plants<br />

Food and beverages<br />

Change in percent<br />

← losers<br />

winners →<br />

Sources: BBE, METRO GROUP<br />

Chilled Food 20.7 1.5<br />

Jams and spreads 15.8 0.8<br />

Eggs 15.5 0.7<br />

Cereals 12.3 0.4<br />

Delicatessen 12.2 2.4<br />

Alcoholic beverages 11.0 13.9<br />

Sweets and confectionery 11.0 7.5<br />

Ice Cream 11.0 1.2<br />

Non-alcoholic beverages 10.1 7.4<br />

Frozen goods 9.9 3.7<br />

Convenience foods 9.4 4.8<br />

Meat, meat products 6.5 18.0<br />

Dairy products 5.9 11.1<br />

Bread, bakery goods 5.3 11.7<br />

Canned goods 4.1 0.7<br />

Home beverages 3.3 3.3<br />

Fish 2.6 1.0<br />

Fats & Oils 0.9 1.8<br />

– 2.2 Fruit, vegetables 8.1<br />

k Share of total consumption in %<br />

¹Fast Moving Consumer Goods (consumer goods für everyday use, e.g. food)<br />

METro rETail CoMPEnDIUM 2010/2011

p. 023 Germany<br />

Nonfood<br />

Change in percent<br />

← losers<br />

winners →<br />

Gardening tools, equipment, furniture 12.6 1.6<br />

Radio, TV, audio 10.9 4.6<br />

Electrical appliances (excluding built-in types) 10.0 3.2<br />

Socks, gloves, accessories 9.6 1.6<br />

Personal hygiene, cosmetics, perfumes 7.9 6.1<br />

Optical products 5.5 1.6<br />

Toys 5.2 2.4<br />

Leather goods, umbrellas 5.1 0.8<br />

Electrical installations 3.8 1.8<br />

Construction materials, building elements, tiles 3.3 3.9<br />

Office machines 2.4 0.7<br />

Stationary 1.8 3.6<br />

Office furniture, equipment 1.6 1.1<br />

Everything for children 1.3 1.3<br />

PC-Computer-Software 1.2 4.3<br />

Books, magazines 0.8 4.4<br />

Fur, leather garments 0.1 0.6<br />

Wood, building elements made from wood 0.0 3.1<br />

– 0.2 Shoes excluding sport shoes 3.4<br />

– 0.6 Glass, china, gifts 1.3<br />

– 0.8 Ladies‘ wear 6.9<br />

– 0.8 Watches, jewellery 1.7<br />

– 1.1 Hardware, metal fittings, tools 0.9<br />

– 1.1 Men‘s underwear, shirts, woollen 1.8<br />

– 1.8 Lamps, lighting fixtures 1.3<br />

– 2.3 Men‘s wear 1.8<br />

– 3.7 Sports and camping 3.2<br />

– 5.5 PC, computer hardware 5.2<br />

– 5.9 Household supplies 1.1<br />

– 5.9 Bathroom ceramics, installations, accessories 1.8<br />

– 6.5 Carpets, flooring 0.8<br />

– 6.6 Paints, varnishes, wallpaper, glue 1.4<br />

– 6.7 Ladies‘ underwear, other ladies‘ wear 0.9<br />

– 6.9 Furniture 9.7<br />

– 7.5 Photography 2.2<br />

– 8.8 Home fabrics, bed linens 1.4<br />

– 8.9 Telecommunications (terminals) 2.5<br />

– 9.7 Car accessories (including radios), car chemicals 1.2<br />

– 10.6 Curtains, decoration, textile fabrics, haberdashery 1.2<br />

– 11.1 Image and sound carriers 1.5<br />

k Share of total consumption in %<br />

1. Data, Figures and Facts<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 024 Germany<br />

Change in consumer prices and<br />

retail prices, 2004 – 2009<br />

Year-on-year price change in percent<br />

→<br />

In detail<br />

2004 2005 2006 2007 2008 2009<br />

3.0%<br />

Source: Federal Statistical Office Germany<br />

2.5%<br />

2.0%<br />

1.5%<br />

1.0%<br />

0.5%<br />

1.7<br />

–0.1<br />

Consumer prices<br />

1.6 1.6<br />

0.7<br />

0.5<br />

2.3<br />

1.9<br />

2.6<br />

Retail prices<br />

0.3<br />

–0.2<br />

In the past, retail prices have often risen more slowly than consumer prices in general. In<br />

2009, retail prices even fell slightly.<br />

METro rETail CoMPEnDIUM 2010/2011

p. 025 Germany<br />

Change in consumer prices<br />

and retail prices, 2009<br />

Change in consumer prices in percent<br />

1. Data, Figures and Facts<br />

1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11.<br />

2.7<br />

1.4<br />

0.4<br />

1.7<br />

1.0<br />

1.7<br />

2.2<br />

– 1.3<br />

– 1.9<br />

– 2.2<br />

– 4.1<br />

10.4 3.9 4.9 30.8 5.6 4.0 13.2 3.1 11.6 0.7 4.4<br />

k Basket weights in %¹<br />

1. Food<br />

2. Alcohol, tobacco<br />

3. Clothing, footwear<br />

4. Rent & utilities<br />

5. Household goods<br />

6. Healthcare<br />

7. Transport<br />

8. Post & telecoms<br />

9. Leisure<br />

10. Education<br />

11. Hotels & restaurants<br />

1<br />

Total < 100 percent because the “other goods and services” category is omitted<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 026 Germany<br />

Purchasing power in Germany<br />

by age group, 2009<br />

Share of total purchasing power in percent<br />

< 25 years<br />

> 65 years<br />

22.1<br />

5.2<br />

11.0<br />

25 – 34 years<br />

55 – 64 years<br />

16.4<br />

21.9<br />

35 – 44 years<br />

23.4<br />

Source: GfK<br />

45 – 54 years<br />

The distribution of purchasing power shows the high importance of consumption by<br />

people over the age of 55. Today, this age group already accounts for almost 40 percent<br />

of all purchasing power. In the coming years, the importance of those aged over 55 will<br />

rise further.<br />

METro rETail CoMPEnDIUM 2010/2011

p. 027 Germany<br />

Development of the financial situation of<br />

the population in Germany, 2001 – 2010<br />

Share in percent<br />

Question: “How would you describe your current financial situation?”<br />

1. Data, Figures and Facts<br />

2001 2008/09 2009/10<br />

2.0<br />

2.0<br />

3.0<br />

“I can afford whatever I want.”<br />

27%<br />

2<strong>5.0</strong><br />

2<strong>5.0</strong><br />

28.0<br />

31%<br />

“I‘m comfortable and can<br />

afford quite a few luxuries.”<br />

Source: GfK European Consumer Study 2009 / 2010 – Trendsensor Konsum<br />

18%<br />

5<strong>5.0</strong><br />

1<strong>5.0</strong><br />

3.0<br />

46.0<br />

21.0<br />

6.0<br />

47.0<br />

18.0<br />

<strong>5.0</strong><br />

23%<br />

“All in all I‘m doing ok.”<br />

“I‘m just barely getting by.”<br />

“I can‘t make ends meet.”<br />

The proportion of Germans with limited disposable income rose between 2001 and 2010. In<br />

comparison to last year, however, the proportion has fallen.<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 028 Germany<br />

The structure of retailing<br />

in Germany<br />

RETAILING<br />

Fast Moving Consumer Goods (FMCG)<br />

Food<br />

Nearfood<br />

General food retailing Specialty/single-line retail Non-stationary retail<br />

Source: METRO GROUP<br />

R Hypermarket<br />

R Large superstores<br />

R Small superstores<br />

R Supermarkets<br />

R Self-service stores<br />

R Discounter<br />

R Chemist‘s<br />

R Beverage stores<br />

R Pet shops<br />

R Specialty stores¹<br />

R Bakeries/butcher‘s etc.<br />

R Other<br />

R (Weekly) markets<br />

R Sales vehicles<br />

R Home delivery<br />

R Mail-order sales<br />

Retailing offers consumers a wide selection of business formats in all sectors.<br />

METro rETail CoMPEnDIUM 2010/2011

p. 029 Germany<br />

RETAILING<br />

1. Data, Figures and Facts<br />

Nonfood<br />

Furniture Electronics 2 Textiles<br />

Home improvement<br />

and diy<br />

Household<br />

goods<br />

Others<br />

R Department stores “Kaufhaus” type<br />

R Specialty centres<br />

R Specialised trade<br />

R Department stores “Warenhaus” type<br />

R Mail-order sales<br />

R Marginal products assortments from suppliers outside the industry<br />

R Other<br />

¹Includes specialty stores for items such as fruit, vegetables, seafood and confectionery<br />

²Consumer electronics, information technology and telecommunication<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 030 Germany<br />

Food supply alternatives<br />

for private households¹<br />

Self-supply<br />

Institutional Supply<br />

Direct sales<br />

Industry/agriculture<br />

Handcrafts<br />

Institutional wholesale<br />

Total supply<br />

Stationary retailing<br />

Institutional retailing<br />

Source: Dr Lademann & Partner<br />

External supply<br />

Mail-order retailing<br />

Itinerant retailing<br />

About half of private household food¹ demand is covered by general retailing.<br />

METro rETail CoMPEnDIUM 2010/2011

p. 031 Germany<br />

R Self-supply<br />

1. Data, Figures and Facts<br />

R Manufacturers, farmers, vintners and purchases from acquaintances<br />

R Bakeries, pastry shops, butcher‘s shops<br />

R C & C wholesale stores, purchases from acquaintances<br />

R General retailing<br />

• Hypermarkets<br />

• Superstores<br />

• Supermarkets<br />

• Neighbourhood stores<br />

• Discounters<br />

• Department stores<br />

R Specialty retailers<br />

• Fruit and vegetable shops<br />

• Delicatessens<br />

• Fishmonger's<br />

• Offlicences<br />

• Sweet shops<br />

• Tobacconist's<br />

• Health food stores<br />

• Chemist's<br />

• Kiosks, vending machines<br />

• Petrol stations<br />

R Mail-order retailing<br />

R Sales vehicles, home delivery and farmer‘s markets<br />

R Restaurants, hotels, cafeterias and snack bars<br />

¹Food and beverages, detergents and cleaning products<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 032 Germany<br />

Market share and sales trends for<br />

food retailing formats, 2004 – 2009<br />

Food retailing formats’ share of FMCG 1<br />

sales in percent<br />

2004 2009<br />

28.2 28.0<br />

Hypermarkets/large-scale superstores<br />

(> 2,500 sqm)<br />

14.5 15.3<br />

13.6 11.0<br />

6.6<br />

4.1<br />

Small scale supermarkets/superstores<br />

(1,000 – 2,499 sqm)<br />

Large supermarkets (400 – 999 sqm)<br />

Small supermarkets (100 – 399 sqm)<br />

37.0<br />

41.6<br />

Discounters<br />

Development of FMCG 1 sales in 2009 compared to 2004 in percent<br />

Source: The Nielsen Company<br />

Hypermarkets/large-scale superstores (> 2,500 sqm) 8.2<br />

Small scale supermarkets/superstores (1,000 – 2,499 sqm) 15.2<br />

– 12.0 Large supermarkets (400 – 999 sqm)<br />

– 32.5 Small supermarkets (100 – 399 sqm)<br />

Discounters 22.5<br />

Food retailing models in total 9.1<br />

The various food retailing formats developed differently in the past 6 years: supermarket<br />

formats lost sales and market share to discounters in particular.<br />

¹Fast Moving Consumer Goods<br />

METro rETail CoMPEnDIUM 2010/2011

p. 033 Germany<br />

Development in the number of food retail<br />

outlets by retailing formats, 2005 – 2010 1<br />

Share of all outlets in food retailing in percent 1<br />

2005 2010<br />

4.7 5.4<br />

10.3 13.0<br />

Hypermarkets/large-scale superstores (> 2,500 sqm)<br />

Small scale supermarkets/superstores (1,000 – 2,499 sqm)<br />

1. Data, Figures and Facts<br />

16.3<br />

14.2<br />

Large supermarkets (400 – 999 sqm)<br />

30.1<br />

21.5<br />

Small supermarkets (100 – 399 sqm)<br />

38.6<br />

45.9<br />

Discounters<br />

Change in number of outlets in 2005 compared to 2010 in percent 1<br />

Source: The Nielsen Company<br />

Hypermarkets/large-scale superstores (> 2,500 sqm) 7.4<br />

Small scale supermarkets/superstores (1,000 – 2,499 sqm) 16.2<br />

– 20.1 Large supermarkets (400 – 999 sqm)<br />

– 34.5 Small supermarkets (100 – 399 sqm)<br />

Discounters 9.5<br />

– 8.0 Food retailing models in total<br />

The number of food retail outlets in Germany has declined by around 8 percent over the past<br />

6 years. In particular, the number of supermarkets has been severely reduced.<br />

1<br />

On 1 January of each year<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 034 Germany<br />

The 10 largest food retailers in<br />

Germany by total sales, 2009<br />

Total sales worldwide and sales in<br />

Germany in € billion¹<br />

Total sales worldwide<br />

Sales in Germany<br />

1.<br />

65.53<br />

2.<br />

54.80<br />

3.<br />

50.91<br />

4.<br />

48.64<br />

5.<br />

42.06<br />

1. METRO GROUP<br />

2. Schwarz <strong>Group</strong><br />

3. REWE <strong>Group</strong>²<br />

4. Aldi ²<br />

5. Edeka <strong>Group</strong><br />

6. Tengelmann²<br />

7. Lekkerland<br />

8. Schlecker²<br />

9. Globus²<br />

10. dm²<br />

34.89<br />

Sources: PlanetRetail, Corporate Information, METRO GROUP<br />

26.51<br />

24.66<br />

23.10<br />

6.<br />

16.71<br />

7.<br />

8. 9. 10.<br />

12.00 6.31<br />

4.98 4.46<br />

6.29 6.72<br />

4.12 3.65 3.21<br />

41% 45% 69% 48% 100% 38% 56% 65% 73% 72%<br />

k Share of sales generated in Germany as percentage of total company sales<br />

The 10 leading German food retailers account for a sales volume of about €306 billion in<br />

2009 with their food and nonfood sales brands, of which about €175 billion was generated in<br />

Germany.<br />

¹Net sales<br />

²Estimates<br />

METro rETail CoMPEnDIUM 2010/2011

p. 035 Germany<br />

Who belongs to whom?<br />

Food retailing in Germany<br />

Totel sales¹ in Germany and the<br />

main sales brands<br />

1. Data, Figures and Facts<br />

Sources: PlanetRetail, Trade Dimensions, company data, METRO GROUP; as of 26th may 2010<br />

1 Edeka <strong>Group</strong> R €42.06 billion<br />

Sales brand<br />

Marktkauf, E center, Aktiv Discount<br />

E aktiv markt<br />

(Neukauf, Comet, Reichelt, Edeka, Kupsch) <br />

Netto, NP, Diska, Treff, Plus, Treff 3000<br />

E C+C Großmarkt<br />

Store format<br />

Hypermarket, superstore<br />

Supermarket<br />

Discounter<br />

Cash+carry<br />

2 REWE <strong>Group</strong>² R €34.89 billion<br />

Sales brand<br />

Toom, Rewe Center, Akzenta<br />

Rewe, Vierlinden, Rewe City, Standa Perfetto,<br />

Kaufpark, Karstadt <br />

Penny, Netto<br />

Toom, B1<br />

ProMarkt<br />

Fegro, Selgros, C-Gro, SB-Handelshof<br />

Atlasreisen, der, Derpart<br />

ITS, Dertour, Jahn, Tjaereborg, Meier's etc.<br />

Store format<br />

Hypermarket, superstore<br />

Supermarket<br />

Discounter<br />

Home improvement centre<br />

Consumer electronics store<br />

Cash+carry<br />

Travel agency<br />

Tour operator<br />

¹Revenues are based on the financial year 2009<br />

² Estimates<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 036 Germany<br />

3 <strong>Metro</strong> <strong>Group</strong> R €26.51 billion<br />

Sales brand<br />

Store format<br />

<strong>Metro</strong> Cash & Carry, C+C Schaper<br />

Cash+carry <br />

Real <br />

Hypermarket <br />

Media Markt, Saturn <br />

Consumer electronics store <br />

Galeria Kaufhof <br />

Department store <br />

Sources: PlanetRetail, Trade Dimensions, company data, METRO GROUP; as of 26th may 2010<br />

4 Schwarz <strong>Group</strong>² R €24.66 billion<br />

Sales brand<br />

Store format<br />

Kaufland, KaufMarkt, Handelshof <br />

Hypermarket, superstore <br />

Lidl <br />

Discounter <br />

5 Aldi² R €23.10 billion<br />

Sales brand<br />

Store format<br />

Aldi Nord, Aldi Süd <br />

Discounter <br />

6 Lekkerland R €6.72 billion<br />

Sales brand<br />

Store format<br />

Lekkerland <br />

Other food wholesale <br />

¹Revenues are based on the financial year 2009<br />

² Estimates<br />

METro rETail CoMPEnDIUM 2010/2011

p. 037 Germany<br />

7 Tengelmann <strong>Group</strong>² R €6.29 billion<br />

Sales brand<br />

Store format<br />

Kaiser’s, Tengelmann <br />

Supermarket <br />

OBI, OBI Gartenparadies <br />

Home improvement centre/garden centre <br />

KiK <br />

Textiles store <br />

1. Data, Figures and Facts<br />

8 Schlecker² R €4.12 billion<br />

Sales brand<br />

Store format<br />

Schlecker, Ihr Platz, Drospa, Ihr Platz Express Chemist’s <br />

Schlecker <br />

Hypermarket <br />

9 Globus² R €3.65 billion<br />

Sales brand<br />

Store format<br />

Globus <br />

Hypermarket <br />

Alpha Tecc <br />

Consumer electronics store <br />

Globus Baumarkt, Hela <br />

Home improvement centre <br />

10 dm² R €3.21 billion<br />

Sales brand<br />

Store format<br />

dm <br />

Chemist’s <br />

© METro AG 2010

Data, Figures and Facts<br />

p. 038 Germany<br />

The 10 largest cash & carry<br />

wholesalers in Germany, 2009<br />

Gross sales in € million<br />

Total volume of top 10: 10,332<br />

6,136<br />

1. <strong>Metro</strong> C&C, C+C Schaper (METRO GROUP)¹<br />

2. Fegro, Selgros (REWE <strong>Group</strong>)<br />

3. E C+C Großmarkt (Edeka <strong>Group</strong>)<br />

4. Handelshof<br />

5. Ratio²<br />

6. Hamberger Großmarkt<br />

7. SB-Zentralmarkt (Brülle & Schmeltzer)<br />

8. Mattfeld<br />

9. Wasgau C+C<br />

10. Frische Paradies<br />

Sources: Trade Dimensions, METRO GROUP<br />

1,584<br />

1,322<br />

536<br />

304<br />

141 126 71 66 46<br />

1. 2. 3. 4. 5. 6. 7. 8. 9. 10.<br />

59.4% 15.3% 12.8% 5.2% 2.9% 1.4% 1.2% 0.7% 0.6% 0.4%<br />

k Share of total volume of top 10<br />

The 10 topselling cash & carry wholesalers in Germany generated a sales volume of more<br />

than €10 billion. The METRO GROup is the market leader with its <strong>Metro</strong> cash & carry sales<br />

division. Following in second and third place are the REWE <strong>Group</strong> with Fegro/Selgros and<br />

the Edeka <strong>Group</strong> with E C+C.<br />

1<br />

Net sales including value added tax composite rate ²Excluding Ratio hypermarket<br />

METro rETail CoMPEnDIUM 2010/2011

p. 039 Germany<br />

The 10 largest hypermarket and superstore<br />

retailers in Germany, 2009<br />

Gross sales in € million<br />

Total volume of top 10: 37,912<br />

1. Data, Figures and Facts<br />

12,250<br />

9,695<br />

6,765<br />

1. Kaufland (Schwarz <strong>Group</strong>)<br />

2. Real (METRO GROUP)¹<br />

3. Marktkauf, E center (Edeka <strong>Group</strong>)<br />

4. Globus<br />

5. Toom, Rewe West (REWE <strong>Group</strong>)<br />

6. Citti, Famila (Bartels-Langness)<br />

7. Hit, AEZ (Dohle <strong>Group</strong>)<br />

8. Famila, Combi (Bünting)<br />

9. V-Markt (Kaes)<br />

10. Ratio²<br />

2,975<br />

Sources: Trade Dimensions, METRO GROUP<br />

1,887<br />

1,480 1,298<br />

835<br />

405 322<br />

1. 2. 3. 4. 5. 6. 7. 8. 9. 10.<br />

32.3% 25.6% 17.8% 7.8% <strong>5.0</strong>% 3.9% 3.4% 2.2% 1.1% 0.8%<br />

k Share of total volume of top 10<br />

The 10 topselling hypermarket and superstore retailers in Germany generated a sales<br />

volume of about €38 billion.<br />

1<br />

Net sales including value added tax composite rate ²Excluding Ratio Cash & Carry<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 040 Germany<br />

The largest discounters in Germany, 2009<br />

Gross sales in € million<br />

Total volume of top 6: 62,632<br />

25,450<br />

1. Aldi Nord, Aldi Süd (Aldi)¹<br />

2. Lidl (Schwarz <strong>Group</strong>)¹<br />

3. Netto (Edeka <strong>Group</strong>)<br />

4. Penny (REWE <strong>Group</strong>)<br />

5. Norma¹<br />

6. Netto (Stavenhagen)²<br />

15,050<br />

10,950<br />

7,683<br />

2,550<br />

1,097<br />

1. 2. 3. 4. 5. 6.<br />

Source: Trade Dimensions<br />

40.6% 24.1% 17.4% 12.3% 3.8% 1.8%<br />

k Share of total volume of top 6<br />

The 6 topselling discounters in Germany generated a sales volume of about €63 billion.<br />

1<br />

Estimate 2<br />

Edeka holds a 25% share<br />

METro rETail CoMPEnDIUM 2010/2011

p. 041 Germany<br />

Chemist‘s in Germany, 2009<br />

Gross sales in € million<br />

Total volume of top 5: 13,766<br />

1. Data, Figures and Facts<br />

4,365<br />

1. Schlecker¹<br />

2. dm<br />

3. Rossmann<br />

4. Müller¹<br />

5. Budnikowsky<br />

3,748<br />

3,093<br />

2,200<br />

1. 2. 3. 4. 5.<br />

360<br />

Source: Trade Dimensions<br />

31.7% 27.2% 22.5% 16.0% 2.6%<br />

k Share of total volume of top 5<br />

The 5 topselling chemist's in Germany generated a sales volume of about €14 billion.<br />

1<br />

Estimate<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 042 Germany<br />

The largest retailers of consumer<br />

electronics stores in Germany, 2009 ¹<br />

Gross sales in € million<br />

Total volume of top 9: 26,688<br />

Sources: Corporate Publications, Planet Retail, Articles from trade magazines<br />

10,837<br />

3,600 3,600<br />

3,146<br />

1,580<br />

1. Media Markt, Saturn (METRO GROUP)²<br />

2. Euronics Deutschland³<br />

2. Expert Deutschland³<br />

4. Electronic Partner Deutschland<br />

5. amazon.com 4<br />

6. pC Spezialist, Microtrend (Synaxon) 5<br />

7. EDA Telering<br />

8. Conrad Electronic 6<br />

9. proMarkt (REWE <strong>Group</strong>)<br />

1. 2. 2. 4. 5. 6. 7. 8. 9.<br />

The 9 topselling consumer electronics businesses or purchasing cooperations in Germany<br />

generated a sales volume of about €27 billion.<br />

1,390<br />

1,060<br />

821 655<br />

¹Only the electronics specialty stores and electronics specialty businesses are considered in this diagram<br />

²Net sales plus estimated value added tax composite rate ³Company statement regarding members’ external sales<br />

4<br />

Estimate for electronics/entertainment (also supplied to other countries) 5<br />

Estimate 6<br />

Sales 2008<br />

METro rETail CoMPEnDIUM 2010/2011

p. 043 Germany<br />

Development of online<br />

retailing¹ sales in Germany<br />

in € billion<br />

1. Data, Figures and Facts<br />

Sources: German E-Commerce and Distance-selling Trade Association, TNS Infratest 2010<br />

1.0<br />

1.8<br />

2.7<br />

3.6<br />

5.2<br />

7.4<br />

Increase 2009 compared<br />

to previous year: 16%<br />

2000 2001 2002 2003 2004 2005 2006² 2007 2008 2009<br />

10.0<br />

10.9<br />

13.4<br />

15.5<br />

1<br />

Only transactions involving material goods; not services, licenses or information<br />

2<br />

Statistical jump because of change in method of data collection<br />

Online retailing in material goods is still recording high annual rates of growth in Germany.<br />

In 2009, sales reached around €15.5 billion; that corresponds to a 16 percent increase on the<br />

previous year.<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 044 Europe<br />

Consumer goods trade<br />

Western Europe<br />

ICELAND<br />

0.3 m. €2.4 bn.<br />

0.0% 0.1%<br />

IRELAND<br />

4.5 m. €28.4 bn.<br />

0.6% 1.0%<br />

GREAT-<br />

BRitAIN<br />

61.6 m. €313.2 bn.<br />

7.6% 11.1%<br />

Belgium<br />

10.7 m. €71.1 bn.<br />

1.3% 2.5%<br />

NethERlANDs<br />

16.6 m. €89.2 bn.<br />

2.0% 3.2%<br />

LuxEMbouRG<br />

0.5 m. €3.8 bn.<br />

0.1% 0.1%<br />

ScandiNAvia<br />

BENElux<br />

GERMANY<br />

82.1 m. €349.2 bn.<br />

10.1% 12.4%<br />

FRANCE<br />

62.3 m. €397.9 bn.<br />

7.7% 14.1%<br />

Austria<br />

8.4 m. €49.9 bn.<br />

1.0% 1.8%<br />

Portugal<br />

10.7 m. €39.7 bn.<br />

1.3% €1.4%<br />

Sources: FERI, IGD, Iceland data of 2008<br />

Spain<br />

44.9 m. €199.7 bn.<br />

5.5% 7.1%<br />

SwitzERlAND<br />

7.6 m. €69.7 bn.<br />

0.9% 2.5%<br />

Italy<br />

59.9 m. €261.9 bn.<br />

7.4% 9.3%<br />

METro rETail CoMPEnDIUM 2010/2011

p. 045 Europe<br />

NorwAY<br />

4.8 m. €39.0 bn.<br />

0.6% 1.4%<br />

SwEDEN<br />

9.3 m. €52.6 bn.<br />

1.1% 1.9%<br />

FinlAND<br />

5.3 m. €33.0 bn.<br />

0.7% 1.2%<br />

1. Data, Figures and Facts<br />

DENMARk<br />

5.5 m. €36.0 bn.<br />

0.7% 1.3%<br />

Consumer goods trade Western Europe<br />

Population<br />

Consumer goods trade<br />

In total 811 million (100%) €2,823 billion (100%) <br />

In Western Europe 395 million (48.7%) €2,037 billion (72.1%) <br />

Approximately 50 percent of the European population lives in<br />

Western Europe. However, their share of European consumer<br />

goods retailing amounts to more than 70 percent.<br />

countRY<br />

in million in € billion<br />

in % in %<br />

Share of consumer goods trade<br />

Share of the European population<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 046 Europe<br />

Consumer goods trade<br />

Eastern Europe<br />

LithuANia<br />

3.3 m. €6.5 bn.<br />

0.4% 0.2%<br />

Estonia<br />

1.3 m. €3.7 bn.<br />

0.2% 0.1%<br />

Latvia<br />

2.3 m. €4.7 bn.<br />

0.3% 0.2%<br />

PolAND<br />

38.1 m. €73.6 bn.<br />

4.7% 2.6%<br />

BelARus<br />

9.6 m. €8.2 bn.<br />

1.2% 0.3%<br />

SlovENia<br />

2.0 m. €8.0 bn.<br />

0.2% 0.3%<br />

Croatia<br />

4.4 m. €9.6 bn.<br />

0.5% 0.3%<br />

CzECh REPublic<br />

10.4 m. €31.8 bn.<br />

1.3% 1.1%<br />

Slovakia<br />

5.4 m. €13.0 bn.<br />

0.7% 0.5%<br />

HuNGARY<br />

10.0 m. €21.2 bn.<br />

1.2% 0.8%<br />

Moldova<br />

3.6 m. €1.5 bn.<br />

0.4% 0.1%<br />

RoMANia<br />

21.3 m. €38.1 bn.<br />

2.6% 1.3%<br />

Bosnia AND<br />

hERzEGoviNA<br />

3.8 m. €3.6 bn.<br />

0.5% 0.1%<br />

BulGARia<br />

7.5 m. €13.5 bn.<br />

0.9% 0.5%<br />

Serbia<br />

9.9 m. €11.4 bn.<br />

1.2% 0.4%<br />

Sources: FERI, IGD, Georgia Dates of 2008<br />

AlbANia<br />

3.2 m. €2.6 bn.<br />

0.4% 0.1%<br />

MACEDonia<br />

2.0 m. €2.1 bn.<br />

0.3% 0.1%<br />

GREECE<br />

11.2 m. €53.8 bn.<br />

1.4% 1.9%<br />

METro rETail CoMPEnDIUM 2010/2011

p. 047 Europe<br />

RussiAN FEDERAtion<br />

140.9 m. €336.2 bn.<br />

17.4% 11.9%<br />

UkRAiNE<br />

45.7 m. €17.5 bn.<br />

5.6% 0.6%<br />

Consumer goods trade Eastern Europe<br />

Population<br />

Consumer goods trade<br />

In total 811 million (100%) €2,823 billion (100%) <br />

In Eastern Europe 416 million (51.3%) €787 billion (27.9%) <br />

At present, Eastern Europe still accounts for less than 30<br />

percent of consumer goods retailing. More than one-third<br />

of the total demand for consumer goods here comes from<br />

Russia, which has by far the biggest retail trade.<br />

countRY<br />

in million in € billion<br />

in % in %<br />

Share of consumer goods trade<br />

Share of the European population<br />

1. Data, Figures and Facts<br />

GeoRGia<br />

4.3 m. €3.4 bn.<br />

0.5% 0.1%<br />

TurkEY<br />

74.8 m. €118.2 bn.<br />

9.2% 4.2%<br />

Cyprus<br />

0.9 m. €5.1 bn.<br />

0.1% 0.2%<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 048 Europe<br />

Comparison of the gross domestic product (GDP) and<br />

private consumption figures for 2009 in Europe<br />

Inhabitants<br />

2009<br />

gdP 2009<br />

nominal<br />

gdP per<br />

inhabitant<br />

Source: FERI<br />

Country in million in € billion in €<br />

Belgium 10.7 337 31,700 <br />

Bulgaria 7.5 33 4,500 <br />

Denmark 5.5 223 40,700 <br />

Germany 82.1 2,407 29,400 <br />

Finland 5.3 171 32,100 <br />

France 62.3 1,907 30,600 <br />

Greece 11.2 238 21,300 <br />

Great Britain 61.6 1,568 25,400 <br />

Ireland 4.5 164 36,200 <br />

Italy 59.9 1,520 25,400 <br />

Croatia 4.4 45 10,300 <br />

Netherlands 16.6 570 34,400 <br />

Norway 4.8 275 57,100 <br />

Austria 8.4 277 33,100 <br />

Poland 38.1 310 8,100 <br />

Portugal 10.7 164 15,300 <br />

Romania 21.3 116 5,400 <br />

Russia 140.9 889 6,300 <br />

Sweden 9.3 288 31,100 <br />

Switzerland 7.6 355 46,900 <br />

Slovakia 5.4 63 11,700 <br />

Spain 44.9 1,051 23,400 <br />

Czech Republic 10.4 137 13,200 <br />

Turkey 74.8 442 5,900 <br />

Ukraine 45.7 80 1,800 <br />

Hungary 10.0 93 9,300 <br />

Highest<br />

Lowest<br />

METro rETail CoMPEnDIUM 2010/2011

p. 049 Europe<br />

Private consumption<br />

2009<br />

nominal<br />

Private<br />

consumption per<br />

inhabitant<br />

in € billion in €<br />

Ratio of private<br />

consumption<br />

to gdP<br />

176 16,500 52.2% Belgium <br />

22 2,900 65.4% Bulgaria <br />

110 20,100 49.2% Denmark <br />

1,410 17,200 58.6% Germany <br />

95 17,700 55.3% Finland <br />

1,112 17,800 58.3% France <br />

172 15,400 72.6% Greece <br />

1,023 16,600 65.2% Great Britain <br />

84 18,600 51.5% Ireland <br />

906 15,100 59.6% Italy <br />

26 5,800 56.9% Croatia <br />

264 15,900 46.3% Netherlands <br />

139 24,100 42.2% Norway <br />

151 18,100 54.6% Austria <br />

191 5,000 61.4% Poland <br />

108 10,100 65.9% Portugal <br />

73 3,400 62.8% Romania <br />

485 3,400 54.6% Russia <br />

140 15,100 48.6% Sweden <br />

206 27,300 58.2% Switzerland <br />

38 7,100 60.5% Slovakia <br />

589 13,100 56.0% Spain <br />

69 6,700 50.6% Czech Republic <br />

316 4,200 71.6% Turkey <br />

53 1,200 66.3% Ukraine <br />

49 4,900 53.1% Hungary <br />

1. Data, Figures and Facts<br />

The figures for the individual European countries (still) differ enormously. For example,<br />

the GDP per capita ranges from approx. €1,800 in Ukraine to around €57,000 in Norway.<br />

Private consumption per capita also varies greatly, with figures (not adjusted for purchasing<br />

power) ranging from €1,200 ukraine to over €27,000 in Switzerland.<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 050 Europe<br />

Gross domestic product EU-15 countries<br />

vs. new EU-12 countries, 1999 – 2009<br />

Growth rates in percent (real)<br />

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009<br />

7.0%<br />

<strong>5.0</strong>%<br />

3.0%<br />

1.0%<br />

New EU-12<br />

4.4<br />

3.0<br />

3.9<br />

2.9<br />

3.0<br />

2.9<br />

1.9<br />

1.2 1.2<br />

5.6<br />

4.7<br />

EU-15<br />

2.2<br />

1.8<br />

6.6<br />

3.0<br />

6.3<br />

2.6<br />

0.5<br />

3.9<br />

– 1.0%<br />

– 3.4<br />

– 3.0%<br />

Source: FERI<br />

– <strong>5.0</strong>%<br />

– 4.3<br />

In recent years, the gross domestic product in the 12 new Eu member states constantly grew at<br />

a faster rate than the average GDp in the core EU-15 countries.<br />

METro rETail CoMPEnDIUM 2010/2011

p. 051 Europe<br />

Gross value added by economic sector<br />

EU-15 countries vs. EU-27 countries, 2009<br />

Gross value added in percent of the GDP<br />

1. Data, Figures and Facts<br />

EU-15 countries<br />

EU-27 countries<br />

29.8 29.1<br />

Company-related financial services<br />

20.5 20.8<br />

Trade, hotels and restaurants,<br />

transport and communication<br />

17.6 18.1<br />

Production industries, including energy<br />

6.2 6.3<br />

1.5 1.6<br />

Construction and housing<br />

Agriculture and forestry, fishing<br />

Source: Eurostat<br />

24.4 24.0<br />

Other services<br />

The distribution of gross value added in the EU-15 countries is different to that of the<br />

EU-27 countries viewed as a whole. The proportion of company-related financial services<br />

and also other miscellaneous services is higher in the EU-15 countries. The trade and<br />

production sectors, however, are slightly lower than average.<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 052 Europe<br />

Breakdown of consumer spending in<br />

private households in Europe, 2008<br />

In percent (nominal)<br />

Germany Italy France<br />

Others (e.g. healthcare, education,<br />

personal hygiene, financial services)<br />

17.3<br />

14.1 1<strong>5.0</strong><br />

Housing, water, energy 24.3<br />

21.2<br />

25.3<br />

Transport and communication<br />

16.6<br />

15.5<br />

6.8<br />

17.4<br />

Leisure time, entertainment, culture<br />

9.4<br />

10.0<br />

9.1<br />

Accomodation and restaurant service<br />

Textiles, furniture, household appliances, etc.<br />

5.7<br />

12.1<br />

15.1<br />

6.2<br />

10.5<br />

Source: Eurostat<br />

Food and beverages, tobacco, etc.<br />

14.6 17.3 16.5<br />

There are considerable differences in how much money private households throughout<br />

Europe spend on the various types of consumer spendings.<br />

METro rETail CoMPEnDIUM 2010/2011

p. 053 Europe<br />

1. Data, Figures and Facts<br />

Great Britain Spain Poland Hungary<br />

16.3<br />

14.6<br />

18.3<br />

13.1<br />

Others (e.g. healthcare,<br />

education, personal hygiene,<br />

financial services)<br />

21.1<br />

17.7<br />

23.7<br />

19.3<br />

Housing, water, energy<br />

17.5<br />

11.6<br />

10.7<br />

14.2<br />

12.5<br />

8.6<br />

7.6<br />

17.7 2.8<br />

8.4<br />

19.4<br />

7.4<br />

5.1<br />

8.3<br />

Transport and communication<br />

Leisure time, entertainment, culture<br />

Accomodation and restaurant service<br />

Textiles, furniture, household<br />

appliances, etc.<br />

10.4<br />

10.5<br />

26.7<br />

27.4<br />

Food and beverages, tobacco, etc.<br />

12.3<br />

16.8<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 054 Europe<br />

Development of retail sales in<br />

Western Europe, 2006 – 2009<br />

Average annual growth (CAGR) in<br />

percent (nominal)<br />

Source: FERI<br />

Eastern Europe Western Europe<br />

Sweden 4.0<br />

Switzerland 3.3<br />

Belgium 3.0<br />

Finland 2.9<br />

Great Britain 2.8<br />

Austria 2.5<br />

France 0.8<br />

Netherlands 0.7<br />

Italy 0.5<br />

Portugal – 0.5<br />

Germany – 0.6<br />

Spain – 1.4<br />

Denmark – 1.4<br />

Ireland – 1.6<br />

Ukraine 2<strong>5.0</strong><br />

Russia 18.9<br />

Romania 13.5<br />

Poland 7.9<br />

Turkey 6.8<br />

Slovakia 2.5<br />

Greece 0<br />

Croatia 0<br />

Hungary – 2.1<br />

Retail sales figures for Western Europe reveal very different growth rates on average for<br />

recent years. In many Eastern European countries, growth rates were high on average for<br />

recent years, despite the retail downturn in 2009. However, retail developments were weak<br />

in Hungary, Croatia and Greece.<br />

METro rETail CoMPEnDIUM 2010/2011

p. 055 Europe<br />

Consumer prices and retail<br />

prices in Europe, 2005 – 2009<br />

Average price increase in percent<br />

1. Data, Figures and Facts<br />

5.1<br />

Consumer prices<br />

Retail prices<br />

3.6<br />

2.8 2.7<br />

1.4<br />

2.3<br />

2.5<br />

2.0<br />

2.0<br />

1.7<br />

1.6<br />

0.1<br />

0.5<br />

Source: FERI<br />

Hungary Poland Spain Great Britain Italy Germany France<br />

– 0.5<br />

In the European countries examined, retail prices increased at a slower rate than consumer<br />

prices in general in recent years.<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 056 Europe<br />

Development of the financial situation<br />

of the population in Europe, 2009<br />

Share in percent<br />

Question: “How would you describe your current financial situation?”<br />

I<br />

E RUS F D A UK PL NL<br />

Source: GfK European Consumer Study 2009 / 2010 – Trendsensor Consumption<br />

0.5 1.1 1.3<br />

14.7 20.4 6.1<br />

52.9<br />

23.4<br />

8.4<br />

52.6<br />

68.0<br />

3.7 2.9 3.0<br />

8.7<br />

64.3<br />

27.5<br />

46.7<br />

30.6<br />

48.2<br />

4.1<br />

13.5<br />

1.3<br />

13.7<br />

65.7 69.5<br />

19.2 21.4 17.2 17.7 15.5 11.4 12.0<br />

6.7 3.2 6.1 5.1 2.6 5.3 3.5<br />

21.7<br />

29.2<br />

38.4<br />

7.5<br />

3.1<br />

“I can afford whatever I want.”<br />

“I‘m comfortable and can afford<br />

quite a few luxuries.”<br />

“All in all I‘m doing ok.”<br />

“I‘m just barely getting by.”<br />

“I can‘t make ends meet.”<br />

Italy, Spain and Russia have the highest proportion of citizens with limited financial means.<br />

METro rETail CoMPEnDIUM 2010/2011

p. 057 Europe<br />

Food retail space density in<br />

Western and Eastern Europe<br />

In sqm per 1,000 citizens<br />

1. Data, Figures and Facts<br />

400 – 600 300 – 400 100 – 300 1 – 100<br />

Sources: sales area: Planet Retail, population: UN<br />

Finland<br />

Norway<br />

Iceland<br />

Sweden<br />

Estonia<br />

Russian<br />

Latvia<br />

Federation<br />

Denmark<br />

Lithuania<br />

Ireland<br />

Netherlands<br />

Poland<br />

Germany<br />

Belarus<br />

Great Britain<br />

Belgium<br />

Czech Republic Slovakia Ukraine<br />

France<br />

Austria<br />

Moldova<br />

Hungary<br />

Switzerland Slovenia<br />

Romania<br />

Croatia<br />

Bulgaria<br />

Georgia<br />

Portugal<br />

Italy<br />

Spain<br />

Turkey<br />

Greece<br />

Bosnia and<br />

Herzegovina<br />

Cyprus<br />

Serbia<br />

Albania Macedonia<br />

The retail space density per inhabitant is highest in Northern and Central Europe. A slight<br />

decrease can be seen in more southerly areas of Europe, while retail space density falls<br />

increasingly sharply towards Eastern Europe.<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 058 Europe<br />

Number of outlets in modern<br />

food retailing (> 400 sqm), 2009<br />

Per million citizens in Europe<br />

> 2,500 sqm<br />

1,000 – 2,500 sqm<br />

400 – 1,000 sqm<br />

439<br />

325<br />

248<br />

213<br />

198<br />

196<br />

194<br />

171<br />

143<br />

116<br />

97<br />

94<br />

9<br />

35<br />

395<br />

Source: The Nielsen Company<br />

23<br />

52<br />

251<br />

8<br />

73<br />

168<br />

3<br />

82<br />

128<br />

10<br />

71<br />

116<br />

26<br />

48<br />

121<br />

A D B NL E F CH GR H PL GB<br />

22<br />

58<br />

114<br />

5<br />

51<br />

114<br />

15<br />

19<br />

109<br />

7<br />

109<br />

23<br />

22<br />

52<br />

23<br />

71<br />

SK<br />

The number and size of outlets in food retailing varies greatly from country to country.<br />

METro rETail CoMPEnDIUM 2010/2011

p. 059 Europe<br />

The 10 largest food retailers<br />

in Europe, 2009¹<br />

Net sales¹ in € billion<br />

Total volume of top 10: 471.34<br />

1. Data, Figures and Facts<br />

Sources: Company information, PlanetRetail, METRO GROUP (average exchange rates for the financial year )<br />

67.65<br />

63.21<br />

54.80 54.37<br />

50.91<br />

1. Carrefour (F)<br />

2. METRO GROUP (D)<br />

3. Schwarz <strong>Group</strong> (D)²<br />

4. Tesco (GB)<br />

5. REWE <strong>Group</strong> (D)²<br />

1. 2. 3. 4. 5. 6. 7. 8. 9. 10.<br />

Note: Figures translated at average exchange rates for the financial year<br />

¹The sales figures relate to each company’s total revenue in Europe (not exclusively food)<br />

²Estimates<br />

42.06<br />

38.43<br />

34.91<br />

6. Edeka <strong>Group</strong> (D)<br />

7. Aldi (D)²<br />

8. Auchan (F)²<br />

9. Leclerc (F)²<br />

10. ITM (Intermarché) (F)²<br />

33.80<br />

31.20<br />

The 10 largest food retailers in Europe (with indication of the home market) posted a total<br />

turnover of more than €470 billion in 2009.<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 060 Europe<br />

Concentration of companies in<br />

European food retailing, 2009<br />

Food sales market share of the top 5<br />

in percent<br />

Source: PlanetRetail<br />

Sweden 88.0<br />

Denmark 84.7<br />

Finland 83.6<br />

Norway 77.5<br />

Belgium 75.3<br />

Luxembourg 72.5<br />

Switzerland 69.3<br />

Austria 66.9<br />

France 63.0<br />

Germany 62.9<br />

Portugal 61.5<br />

Spain 60.5<br />

Ireland 56.9<br />

Netherlands 54.1<br />

Slovakia 53.4<br />

Great Britain 51.7<br />

Hungary 49.6<br />

Czech Republic 46.2<br />

Greece 45.6<br />

Italy 32.9<br />

Ukraine 24.3<br />

Romania 23.5<br />

Russia 21.3<br />

Poland 21.2<br />

The concentration of food retailers in Western European countries is particularly high. In<br />

Germany, the 5 largest companies generate about 63 percent of the total food sales; in<br />

Sweden, the figure is almost 88 percent.<br />

METro rETail CoMPEnDIUM 2010/2011

p. 061 Europe<br />

Source: PlanetRetail<br />

Who belongs to whom?<br />

Food retailing in Europe<br />

1 Carrefour (F) R €67.65 billion<br />

Sales brand Store format With outlets in¹<br />

Carrefour Hypermarket B, BG, E, F, GR, I, PL, RO, RUS, TR <br />

Promocash Cash+carry F<br />

Champion Supermarket B<br />

Shopi Neighbourhood store F<br />

ED Discounter F<br />

Carrefour Petrol station F<br />

GB Supermarket B<br />

Express Neighbourhood store B<br />

Carrefour Marinopoulos Supermarket GR<br />

5’ Marinopoulos Convenience store GR<br />

Dia Discounter E, GR, TR<br />

GS Supermarket I<br />

Di Per Di Convenience store I<br />

Docks Market Cash+carry I<br />

Minipreço Discounter P <br />

Carrefour Express Supermarket E, F, GR, PL, RO, TR<br />

5 minut Convenience store PL<br />

Carrefour City Convenience store E<br />

With European outlets in: France, Belgium, Bulgaria, Greece, Italy, Poland, Portugal, Romania, Russia, Spain,<br />

Turkey<br />

1. Data, Figures and Facts<br />

Only those country operations are shown in which the given company has a share of at least<br />

50 percent.<br />

1<br />

See page 65 for a key to the country abbreviations<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 062 Europe<br />

Who belongs to whom?<br />

Food retailing in Europe<br />

2 <strong>Metro</strong> <strong>Group</strong> (D) R €63.21 billion<br />

Sales brand Store format With outlets in¹<br />

<strong>Metro</strong> Cash & Carry Cash+carry A, BG, D, DK, F, H, HR, I, MD, RO, RUS,<br />

SK, SRB, TR, UA <br />

Makro Cash & Carry Cash+carry B, CZ, E, GB, GR, NL, P, PL <br />

Real Hypermarket D, PL, RO, RUS, TR, UA <br />

Media Markt Consumer electronics store A, B, CH, D, E, GR, H, I, NL, P, PL, RUS,<br />

S, TR <br />

Saturn Consumer electronics store A, B, CH, D, E, F, GR, H, I, L, NL, PL, TR <br />

Galeria Kaufhof Department store D <br />

Galeria Inno Department store B <br />

With European outlets in: Germany, Austria, Belgium, Bulgaria, Croatia, Czech Republic, Denmark, France, Great<br />

Britain, Greece, Hungary, Italy, Luxembourg, Moldova, Netherlands, Poland, Portugal, Romania, Russia, Serbia,<br />

Slovakia, Spain, Sweden, Switzerland, Turkey, Ukraine<br />

Source: PlanetRetail; as of 23th june 2010<br />

3 Schwarz <strong>Group</strong> (D)² R €54.80 billion<br />

Sales brand Store format With outlets in¹<br />

Kaufland, KaufMarkt Hypermarket, superstore BG, CZ, D, HR, PL, RO, SK<br />

Handelshof Superstore D<br />

Mega Cent Discounter D<br />

Lidl Discounter A, B, CH, CZ, D, DK, E, F, FIN, GB, GR, H,<br />

HR, I, IRL, L, M, NL, P, PL, S, SK, SLO <br />

With outlets in: Germany, Austria, Belgium, Bulgaria, Croatia, Czech Republic, Denmark, Finland, France, Great Britain,<br />

Greece, Hungary Ireland, Italy, Luxembourg, Malta, Netherlands, Poland, Portugal, Romania, Slovakia, Slovenia,<br />

Sweden, Spain, Switzerland<br />

1<br />

See page 65 for a key to the country abbreviations ²Some of the figures are estimates<br />

METro rETail CoMPEnDIUM 2010/2011

p. 063 Europe<br />

4 Tesco (GB) R €54.37 billion<br />

Sales brand Store format With outlets in¹<br />

Tesco Supermarket CZ, H, IRL, PL, SK<br />

1. Data, Figures and Facts<br />

Tesco Hypermarket CZ, H, PL, SK<br />

Tesco Superstore GB, IRL<br />

Tesco Extra Hypermarket GB, IRL<br />

Tesco <strong>Metro</strong> Supermarket GB<br />

Tesco Express, One Stop Convenience store CZ, GB, H, IRL, SK<br />

Kipa Hypermarket TR<br />

Kipa Ekspres Convenience store TR<br />

Tesco Homeplus Nonfood store GB<br />

Dobbies Garden centre GB<br />

With outlets in: Great Britain, Czech Republic, Hungary, Ireland, Poland, Slovakia, Turkey<br />

5 REWE <strong>Group</strong> (D)² R €50.91 billion<br />

Sales brand Store format With outlets in¹<br />

Rewe, Akzenta Superstore D<br />

Rewe, Vierlinden, Rewe City,<br />

Rewe Center, Akzenta, Contra,<br />

Kaufpark, Temma Supermarket D<br />

Netto Discounter D<br />

Penny Discounter A, BG, CZ, D, H, I, RO<br />

With European outlets in: Germany, Austria, Bulgaria, Croatia, Czech Republic, France, Hungary, Italy, Poland,<br />

Romania, Russia, Switzerland, Ukraine<br />

rewe <strong>Group</strong> continued R<br />

Only those country operations are shown in which the given company has a share of at least<br />

50 percent.<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 064 Europe<br />

Who belongs to whom?<br />

Food retailing in Europe<br />

REWE <strong>Group</strong> continued<br />

5 REWE <strong>Group</strong> (D)² R €50.91 billion<br />

Sales brand Store format With outlets in¹<br />

Toom, Rewe Center Hypermarket D<br />

Toom, B1 Home improvement centre D<br />

Nahkauf etc. Neighbourhood store D<br />

ProMarkt Consumer electronics store D<br />

SB-Handelshof, Fegro, C-Gro Cash+carry D<br />

Selgros Cash+carry D, PL, RO, RUS<br />

Pro Direst, Aldis Service Plus Food service CH, F<br />

Howeg Food service CH<br />

Atlasreisen, der, Derpart Travel agency D<br />

ITS, Dertour, Jahn, Tjaereborg,<br />

Meier's etc. Tour operator D<br />

Billa Supermarket A, BG, CZ, HR, I, PL, RO, RUS, SK, Ua <br />

Billa Superstore Superstore I <br />

Magnet Superstore A <br />

Standa Supermarket D, I<br />

Merkur, Adeg, Sutterlüty Supermarket A <br />

Bipa Chemist’s A, I, HR<br />

Source: PlanetRetail<br />

Prodega Cash+carry CH<br />

AGM Cash+carry A <br />

With European outlets in: Germany, Austria, Bulgaria, Croatia, Czech Republic, France, Hungary, Italy, Poland,<br />

Romania, Russia, Slovakia, Switzerland, Ukraine<br />

Only those country operations are shown in which the given company has a share of at least<br />

50 percent.<br />

1<br />

See page 65 for a key to the country abbreviations ²Some of the figures are estimates<br />

METro rETail CoMPEnDIUM 2010/2011

p. 065 Europe<br />

6 EDEKA <strong>Group</strong> (D) R €42.06 billion<br />

Sales brand Store format With outlets in¹<br />

Marktkauf, E center Hypermarket, superstore D<br />

E neukauf Superstore D<br />

E aktiv markt (Comet, Reichelt,<br />

Kupsch etc.)<br />

Neighbourhood store, supermarket D<br />

1. Data, Figures and Facts<br />

Nah & Gut Neighbourhood store D<br />

Netto, NP, Diska, Treff, Plus Discounter D<br />

E C+C Großmarkt Cash+carry D<br />

With European outlets in: Germany<br />

7 Aldi (D)² R €38.43 billion<br />

Sales brand Store format With outlets in¹<br />

Aldi Süd Discounter CH, D, GB, GR, H, IRL<br />

Aldi Nord Discounter B, D, DK, E, F, L, NL, P, PL<br />

Hofer Discounter A, SLO<br />

With European outlets in: Germany, Austria, Belgium, Denmark, France, Great Britain, Greece, Hungary, Ireland,<br />

Luxembourg, Netherlands, Poland, Portugal, Slovenia, Spain, Switzerland<br />

Country Abbreviations<br />

A Austria GB Great Britain P Portugal<br />

B Belgium GR Greece Pl Poland<br />

BG Bulgaria H Hungary RO Romania<br />

BIH Bosnia and Herzegovina Hr Croatia RUs Russia<br />

CH Switzerland I Italy S Sweden<br />

CZ Czech Republic IRL Ireland SK Slovakia<br />

D Germany L Luxembourg SLO Slovenia<br />

DK Denmark LT Lithuania SRB Serbia<br />

E Spain LV Latvia Tr Turkey<br />

EST Estonia M Malta Ua Ukraine<br />

F France MD Moldova<br />

Fin Finland NL Netherlands<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 066 Europe<br />

Who belongs to whom?<br />

Food retailing in Europe<br />

Source: PlanetRetail; as of 23th june 2010<br />

8 Auchan (FR)² R €34.91 billion<br />

Sales brand Store format With outlets in¹<br />

Auchan Hypermarket F, H, I, L, PL, RO, RUS, UA <br />

Easy Marché Supermarket F <br />

Chronodrive, Alcampo Drive Food Service (drive-in) E, F <br />

Sma, Simply Market Supermarket F, I <br />

Simply Market Supermarket E, PL <br />

Alcampo Hypermarket E <br />

Aro Rojo Supermarket E <br />

Eurobounta Discounter (nonfood) F <br />

7 d, Aro Rojo Neighbourhood store E <br />

Jumbo Hypermarket P <br />

Pão de Açúcar Superstore P <br />

Box Consumer electronics store P <br />

Radouga Superstore RUS <br />

Atak Discounter RUS <br />

Les Halles d'Auchan Superstore F <br />

Alinéa Furniture store F <br />

With European outlets in: France, Italy, Luxembourg, Poland, Portugal, Romania, Russia, Spain, Ukraine, Hungary<br />

Only those country operations are shown in which the given company has a share of at least<br />

50 percent.<br />

1<br />

See page 65 for a key to the country abbreviations ²Some of the figures are estimates<br />

METro rETail CoMPEnDIUM 2010/2011

p. 067 Europe<br />

9 Leclerc (FR)² R €33.80 billion<br />

Sales brand Store format With outlets in¹<br />

Leclerc Hypermarket E, F, PL, SLO <br />

Leclerc Supermarket F, P, PL <br />

Espace Culturel Music/video store E, F, P, PL <br />

L'Auto Automative service centre F <br />

Brico Jardin Home improvement centre F <br />

Leclerc Petrol stationshop F <br />

With European outlets in: France, Poland, Portugal, Slovenia, Spain<br />

1. Data, Figures and Facts<br />

10 Intermarché (FR)² R €31.20 billion<br />

Sales brand Store format With outlets in¹<br />

Intermarché Supermarket B, E, F, P, PL <br />

Ecomarché Supermarket (small) B, F, P <br />

Le Relais des Mousquetaires Neighbourhood store F <br />

Bricomarché Home improvement centre F, P, PL <br />

Veti Textiles store F, P <br />

Stationmarché/Roady Garages F, P <br />

Culture et Loisirs Music/video store F <br />

Restaumarché Restaurant F <br />

InterEx Supermarket BIH, RO, SRB <br />

Netto Discounter F <br />

With European outlets in: France, Belgium, Bosnia and Herzegovina, Poland, Portugal, Romania, Serbia, Spain<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 068 Europe<br />

The 9 largest consumer electronics<br />

stores in Europe, 2009<br />

Gross sales 1 in € million<br />

Total volume of top 9: 81,314<br />

Sources: Corporate publications, Planet Retail, articles from trade magazines<br />

23,414<br />

12,779<br />

11,593<br />

9,136<br />

6,873<br />

1. Media Markt and Saturn (METRO GROUP)<br />

2. Euronics<br />

3. DSG International<br />

4. Expert²<br />

5. KESA Electricals<br />

6. Electronic Partner<br />

7. Amazon.com³<br />

8. Fnac (ppR <strong>Group</strong>) 4<br />

9. EDA Telering²<br />

5,148<br />

4,300 4,194 3,877<br />

1. 2. 3. 4. 5. 6. 7. 8. 9.<br />

¹Net sales including value added tax composite rate ²Without Spain ³Estimates electronics/entertainment<br />

4<br />

Excluding books<br />

The 9 largest consumer electronics store operators by sales volume in Europe (with<br />

indication of the home market) reported a total turnover of more than €80 billion in 2009.<br />

METro rETail CoMPEnDIUM 2010/2011

p. 069 Europe<br />

The 10 largest department<br />

stores in Europe, 2009<br />

Net sales 1 2009 in € million<br />

Total Volume of top 10: 42,454<br />

1. Data, Figures and Facts<br />

Sources: Verdict Global Department Store Retailing 2010,<br />

Corporate information, METRO GROUP<br />

10,758<br />

9,667<br />

4,904<br />

4,095<br />

3,539<br />

¹Only department stores ²Net sales 2008 ³Estimate<br />

1. Marks & Spencer (GB)<br />

2. El Corte Inglés (E) 1, 2<br />

3. Argos (GB)<br />

4. Karstadt (D) 3<br />

5. Galeria Kaufhof/Inno (METRO GROUP) (D)<br />

6. Debenhams (GB)<br />

7. Galeries Lafayette (F) 2, 3<br />

8. John Lewis (GB)<br />

9. Manor (CH) 3<br />

10. Stockmann (FIN)<br />

2,214 2,166 2,065 1,977<br />

1. 2. 3. 4. 5. 6. 7. 8. 9. 10.<br />

1,069<br />

The 10 largest department store operators (with indication of the home market)<br />

reported a total turnover of more than €40 billion in 2009.<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 070 Europe<br />

Share of sales accounted for by private labels<br />

in the European food retail sector 1 , 2009<br />

Share of sales in percent<br />

Source: The Nielsen Company<br />

Switzerland 46.2 – 0.4<br />

Great Britain 42.5 – 1.1<br />

Germany 31.7 0.7<br />

Spain 31.4 5.5<br />

Slovakia 29.7 3.0<br />

Austria 28.0 0.9<br />

France 27.7 2.4<br />

Belgium 26.6 – 0.6<br />

Portugal 2<strong>5.0</strong> 3.9<br />

Netherlands 24.8 3.3<br />

Czech Republic 23.6 0.8<br />

Denmark 21.5 0.5<br />

Hungary 19.6 3.3<br />

Italy 14.6 1.5<br />

Poland 13.9 2.0<br />

Greece 12.2 1.9<br />

Turkey 11.5 4.2<br />

k Variation of sales share of own brands 2007-2009 in %-pts.<br />

In most European countries, private labels accounted for a growing share of sales of fastmoving<br />

consumer goods 1 in the food retail sector in the past 3 years.<br />

¹Fast Moving Consumer Goods (FMCG) excluding fresh produce<br />

METro rETail CoMPEnDIUM 2010/2011

p. 071 Europe<br />

European comparison of Internet<br />

users and online shoppers<br />

Diameter corresponds to average<br />

annual online spending per online<br />

shopper<br />

1. Data, Figures and Facts<br />

k Percentage Internet user 1<br />

100<br />

75<br />

50<br />

Spain<br />

Germany<br />

Netherlands<br />

France<br />

Great Britain<br />

Sweden<br />

Italy<br />

Poland<br />

25<br />

Source: Forrester Research, 2010<br />

0 25<br />

50 75 100<br />

k Percentage online shoppers 2<br />

In Sweden, the Netherlands, Germany and the UK, the percentage of Internet users and<br />

online shoppers is above average.<br />

¹Percentage of the total population over the age of 16 who use the Internet<br />

²Internet users who have purchased goods online as a percentage of the total population over the age of 16<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 072 Europe<br />

Store opening hours in Europe<br />

Sources: METRO GROUP, EuroCommerce, Germany: Federal law<br />

Rank<br />

Monday – Friday<br />

Saturday<br />

6 12 18 6 12 18<br />

1 Great Britain 0 – 24 0 – 24<br />

Ireland 0 – 24 0 – 24<br />

Poland 0 – 24 0 – 24<br />

Russia 0 – 24 0 – 24<br />

Sweden 0 – 24 0 – 24<br />

Slovakia 0 – 24 0 – 24<br />

Czech Republic 0 – 24 0 – 24<br />

Ukraine 0 – 24 0 – 24<br />

Hungary 0 – 24 0 – 24 2<br />

2 Portugal 0 – 24 0 – 24<br />

3 Germany 0 – 24 3 0 – 24 3<br />

France 0 – 24 0 – 24<br />

Greece 0 – 24 0 – 24<br />

Norway 0 – 24 0 – 24<br />

Spain 0 – 24 0 – 24<br />

4 Denmark 0 – 24 0 – 17<br />

5 Belgium 5 – 22 5 – 21<br />

6 Italy 5 – 21 5 – 21<br />

Netherlands 6 – 22 6 – 22<br />

7 Austria 6 – 21 6 – 18<br />

8 Finland 7 – 21 7 – 18<br />

1<br />

Stores less than 280 sqm; otherwise 6 hours between 10 am to 6 pm<br />

2<br />

Until 2 pm on December 24, but subject to some local restrictions between 10 pm and 6 am<br />

³In most states; in some cases 6 am to 8/10 pm<br />

METro rETail CoMPEnDIUM 2010/2011

p. 073 Europe<br />

Sunday<br />

6 12 18<br />

Total hours<br />

0 – 24 1 168 Great Britain 1<br />

0 – 24 168 Ireland<br />

0 – 24 168 Poland<br />

0 – 24 168 Russia<br />

0 – 24 168 Sweden<br />

0 – 24 168 Slovakia<br />

0 – 24 168 Czech Republic<br />

0 – 24 168 Ukraine<br />

0 – 24 2 168 Hungary<br />

6 – 24 162 Portugal 2<br />

> 10 Sundays /year 144 Germany 3<br />

— 144 France<br />

> 18 Sundays /year 144 Greece<br />

3 Sundays /year 144 Norway<br />

12 Sundays /year 144 Spain<br />

12 Sundays /year 137 Denmark 4<br />

— 101 Belgium 5<br />

— 96 Italy 6<br />

12 Sundays /year 4 96 Netherlands<br />

— 87 Austria 7<br />

12 – 21 5 81 / 90 Finland 8<br />

Rank<br />

1. Data, Figures and Facts<br />

4<br />

Sunday shopping allowed in Amsterdam, Rotterdam and tourist centres<br />

5<br />

May, June, July, August, November and December only<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 074 Worldwide<br />

Consumer goods world trade<br />

World population, total: 6,829 million people<br />

Consumer goods trade, total: €9,459 billion<br />

NAFta /<br />

North America<br />

458 m. €2.518 bn.<br />

6.7% 26.6%<br />

Central and<br />

South America<br />

430 m. €605 bn.<br />

6.3% 6.4%<br />

Sources: FERI, IGD<br />

METro rETail CoMPEnDIUM 2010/2011

p. 075 Worldwide<br />

Nearly 60 percent of consumer goods retailing focuses on one-fifth<br />

of the world’s population (Europe and North America).<br />

Europe<br />

Share of the<br />

world’s population<br />

Share of global<br />

consumer goods trade<br />

Western Europe 395 million (5.8%) €2,036 billion (21.5%) <br />

Eastern Europe 416 million (6.1%) €787 billion (8.3%) <br />

Europe total 811 million (11.9%) €2,823 billion (29.8%) <br />

1. Data, Figures and Facts<br />

Asia<br />

4,086 m. €3.136 bn.<br />

59.8% 33.2%<br />

Africa<br />

1,009 m. €239 bn.<br />

14.8% 2.5%<br />

Oceania<br />

35 m. €132 bn.<br />

0.5% 1.4%<br />

Continent<br />

in million in € billion<br />

in % in %<br />

Share of global consumer goods trade<br />

Share of the world’s population<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 076 Worldwide<br />

Economic development in Germany,<br />

Europe and the world<br />

GDP (real) in percent<br />

2005 2006<br />

7.2<br />

Western Europe<br />

Eastern Europe<br />

5.4<br />

4.8<br />

3.4<br />

3.1<br />

5.2<br />

3.8<br />

Asia<br />

1.9<br />

World<br />

Source: FERI<br />

Overall, the Asian economy has overcome the financial and economic crisis best. Its development<br />

in 2009 was also stable, unlike every other region.<br />

METro rETail CoMPEnDIUM 2010/2011

p. 077 Worldwide<br />

2007 2008 2009<br />

1. Data, Figures and Facts<br />

7.3<br />

5.8<br />

<strong>5.0</strong><br />

3.7<br />

2.7<br />

2.5<br />

0.5<br />

1.4<br />

– 0.1<br />

– 2.2<br />

– 4.2<br />

– 5.8<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 078 Worldwide<br />

Change in GDP and private consumption<br />

in selected countries, 2009<br />

Real, in percent<br />

– 14 – 12 – 10 – 8 – 6 – 4 – 2 0 2 4 6 8 10 12 14<br />

China<br />

India<br />

3.9<br />

5.7<br />

7.2<br />

8.7<br />

Poland<br />

1.7<br />

2.3<br />

Asia – 0.1 1.3<br />

– 2.5<br />

0.6<br />

France<br />

– 3.6<br />

– 4.9<br />

Spain<br />

– 4.2<br />

– 1.5<br />

Western Europe<br />

– 4.7<br />

– 2.3<br />

Turkey<br />

Source: FERI, as of June 2010<br />

– 10.6<br />

– 4.9<br />

– 4.9<br />

– 5.2<br />

– 5.8<br />

– 5.6<br />

– 7.1<br />

– 7.8<br />

– 7.7<br />

– 3.2<br />

– 1.0<br />

– 0.1<br />

Great Britain<br />

Germany<br />

Japan<br />

Eastern Europe<br />

Romania<br />

Russia<br />

GDP<br />

Private consumption<br />

China and India experienced the greatest economic growth again in 2009, whereas most countries<br />

reported decreases during the financial and economic crisis. private consumption also<br />

increased most in the Asian countries.<br />

METro rETail CoMPEnDIUM 2010/2011

p. 079 Worldwide<br />

The 10 largest food<br />

retailers worldwide<br />

Net sales 2009 in € billion<br />

Total volume of top 10: 811.60<br />

1. Data, Figures and Facts<br />

Sources: Corporate information METRO GROUP, PlanetRetail<br />

289.53<br />

85.93<br />

65.53 64.19<br />

Note: average exchange rates for the financial year<br />

¹Estimates<br />

1. Wal-Mart (USA)<br />

2. Carrefour (F)<br />

3. METRO GROUP (D)<br />

4. Tesco (GB)<br />

5. Schwarz <strong>Group</strong> (D)<br />

6. Costco (USA)<br />

7. Kroger (USA)<br />

8. REWE <strong>Group</strong> (D)<br />

9. Aldi (D) 1<br />

10. Target (USA)<br />

54.80 52.87 52.58 50.91 49.60<br />

1. 2. 3. 4. 5. 6. 7. 8. 9. 10.<br />

45.34<br />

The 10 food retailers with the highest turnover generated total sales around €812 billion.<br />

METRO GROup is the world‘s third largest food retailer. The diagram shows the 10 food<br />

retailers in terms of sales volume (together with their domestic markets).<br />

© METro AG 2010

Data, Figures and Facts<br />

p. 080 Worldwide<br />

Who belongs to whom?<br />

Food retailing worldwide<br />

Source: PlanetRetail; as of 23th june 2010<br />

1 Wal-Mart (USA) R €289.53 billion<br />

Sales brand Store format With outlets in¹<br />

Wal-Mart Supercenter Hypermarket BR, CDN, MEX, PRI, RA, RC, USA <br />

Wal-Mart Discounter (nonfood, large scale) CDN, PRI, USA <br />

Sam’s Club Cash+carry BR, MEX, PRI, RC, USA <br />

Wal-Mart Neighborhood Market Superstore RC, USA <br />

Todo Dia Superstore BR <br />

Bompreço Superstore BR <br />

Big Hypermarket BR <br />

Nacional, Mercadorama Supermarket BR <br />

Maxxi Atacado Cash+carry BR <br />

Hiper Magazine Book trade BR <br />

Asda Wal-Mart Supercentre Hypermarket GB <br />

Asda Superstore GB <br />

Asda Living Discounter (nonfood, large scale) GB <br />

Livin, Seiyu Hypermarket J <br />

Seiyu, Sunny, Seiyu The Food Factory Superstore J <br />

Wakana Fast-food chain J <br />

Aurrerá, Bodega Aurrerá Superstore MEX <br />

Superama Supermarket MEX <br />

Suburbia Textiles store MEX <br />

Vips Restaurant MEX <br />

Wal-Mart continued R<br />

1<br />

See page 89 for a key to the country abbreviations<br />

METro rETail CoMPEnDIUM 2010/2011

p. 081 Worldwide<br />

Wal-Mart continued<br />

1 Wal-Mart (USA) R €289.53 billion<br />

Sales brand Store format With outlets in¹<br />

Amigo Superstore PRI <br />

Hiper Paiz Hypermarket ES, GCA, HN <br />

Despensa Familiar Discounter ES, GCA, HN <br />

La Despensa de Don Juan Supermarket ES <br />

Hipermas Hypermarket CR <br />

Pali Discounter CR, NIC <br />

Mas-x-menos Superstore CR <br />

Supertiendas Paiz Supermarket GCA, HN <br />

ClubCo Cash+carry GCA <br />

Maxi Bodega Supermarket CR, HN, GCA <br />

La Union Supermarket NIC <br />

Changomas Superstore RA <br />

Marketside Supermarket USA <br />

Hiper Lider Hypermarket RCH <br />

aCuenta, Express de Lider Supermarket RCH <br />

Ekono Discounter RCH <br />

Smart Choice Supermarket RC <br />

Best Price Modern Wholesale Cash+carry IND <br />

Super Ahorros Discounter PRI <br />

With outlets in: USA, Argentina, Brazil, Canada, Chile, China, El Salvador, Great Britain, Guatemala, Honduras, India,<br />

Japan, Mexico, Nicaragua, Puerto Rico, Costa Rica<br />

1. Data, Figures and Facts<br />

Only those country operations are shown in which the given company has a share of at least<br />

50 percent.<br />

© METro AG 2010