IFRS in India - jb nagar cpe study circle of wirc of icai

IFRS in India - jb nagar cpe study circle of wirc of icai

IFRS in India - jb nagar cpe study circle of wirc of icai

- No tags were found...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

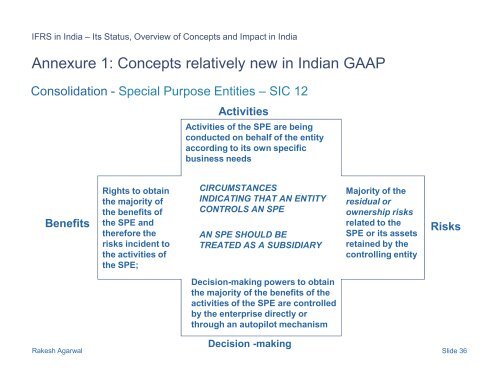

<strong>IFRS</strong> <strong>in</strong> <strong>India</strong> – Its Status, Overview <strong>of</strong> Concepts and Impact <strong>in</strong> <strong>India</strong>Annexure 1: Concepts relatively new <strong>in</strong> <strong>India</strong>n GAAPConsolidation - Special Purpose Entities – SIC 12ActivitiesActivities <strong>of</strong> the SPE are be<strong>in</strong>gconducted on behalf <strong>of</strong> the entityaccord<strong>in</strong>g to its own specificbus<strong>in</strong>ess needsBenefitsRights to obta<strong>in</strong>the majority <strong>of</strong>the benefits <strong>of</strong>the SPE andtherefore therisks <strong>in</strong>cident tothe activities <strong>of</strong>the SPE;CIRCUMSTANCESINDICATING THAT AN ENTITYCONTROLS AN SPEAN SPE SHOULD BETREATED AS A SUBSIDIARYMajority <strong>of</strong> theresidual orownership risksrelated to theSPE or its assetsreta<strong>in</strong>ed by thecontroll<strong>in</strong>g entityRisksDecision-mak<strong>in</strong>g powers to obta<strong>in</strong>the majority <strong>of</strong> the benefits <strong>of</strong> theactivities <strong>of</strong> the SPE are controlledby the enterprise directly orthrough an autopilot mechanismDecision -mak<strong>in</strong>gRakesh Agarwal Slide 36