01.10.2010 Corporate presentation - TAURON Polska Energia

01.10.2010 Corporate presentation - TAURON Polska Energia

01.10.2010 Corporate presentation - TAURON Polska Energia

- No tags were found...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

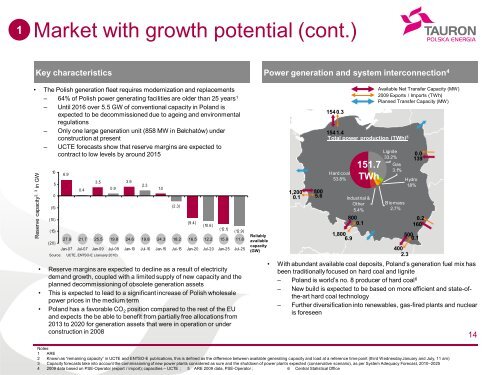

Reserve capacity 2, 3 in GW1Market with growth potential (cont.)Key characteristics Power generation and system interconnection 4• The Polish generation fleet requires modernization and replacements– 64% of Polish power generating facilities are older than 25 years 1– Until 2016 over 5.5 GW of conventional capacity in Poland isexpected to be decommissioned due to ageing and environmentalregulations– Only one large generation unit (858 MW in Bełchatów) underconstruction at present– UCTE forecasts show that reserve margins are expected tocontract to low levels by around 20151050(5)(10)(15)(20)6.90.43.50.93.92.31.0(2.3)(9.4)(10.6)(12.1)(12.9)27.9 21.7 25.5 19.8 24.6 19.8 24.3 18.2 16.5 12.2 15.9 11.8Jan-07 Jul-07 Jan-09 Jul-09 Jan-10 Jul-10 Jan-15 Jul-15 Jan-20 Jul-20 Jan-25 Jul-25Source: UCTE, ENTSO-E (January 2010)• Reserve margins are expected to decline as a result of electricitydemand growth, coupled with a limited supply of new capacity and theplanned decommissioning of obsolete generation assets• This is expected to lead to a significant increase of Polish wholesalepower prices in the medium term• Poland has a favorable CO 2 position compared to the rest of the EUand expects the be able to benefit from partially free allocations from2013 to 2020 for generation assets that were in operation or underconstruction in 2008Reliablyavailablecapacity(GW)1,2000.18005.6154 0.3154 1.4Total power production (TWh) 5Hard coal53.8%8000.1151.7TWhIndustrial &Other5.4%Available Net Transfer Capacity (MW)2009 Exports / Imports (TWh)Planned Transfer Capacity (MW)Lignite33.2%Gas3.1%Biomass2.7%1,800 5006.90.14002.3Hydro1.8%0.01390.2160• With abundant available coal deposits, Poland’s generation fuel mix hasbeen traditionally focused on hard coal and lignite– Poland is world’s no. 8 producer of hard coal 6– New build is expected to be based on more efficient and state-ofthe-arthard coal technology– Further diversification into renewables, gas-fired plants and nuclearis foreseen14Notes:1 ARE2 Known as ―remaining capacity‖ in UCTE and ENTSO-E publications, this is defined as the difference between available generating capacity and load at a reference time point (third Wednesday January and July, 11 am)3 Capacity forecasts take into account the commissioning of new power plants considered as sure and the shutdown of power plants expected (conservative scenario), as per System Adequacy Forecast, 2010–20254 2009 data based on PSE-Operator (export / import); capacities – UCTE ; 5 ARE 2009 data, PSE-Operator ; 6 Central Statistical Office