Guide to the General Index of Financial Information ... - New Learner

Guide to the General Index of Financial Information ... - New Learner

Guide to the General Index of Financial Information ... - New Learner

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>General</strong> <strong>Information</strong>Who can use <strong>the</strong> GIFI?All corporations—except for insurance corporations—canfile using <strong>the</strong> GIFI.Insurance corporationsThe GIFI does not currently meet <strong>the</strong> reporting needs <strong>of</strong>insurance corporations involved in underwriting(life insurers, deposit insurers, or property and casualtyinsurers). The GIFI does not include items specific <strong>to</strong> <strong>the</strong>insurance industry. You should continue <strong>to</strong> submit a papercopy <strong>of</strong> your financial statements along with your T2 returnand schedules.Non-resident corporationsYou can use <strong>the</strong> GIFI when you report in unconsolidatedCanadian funds. Do not use <strong>the</strong> GIFI if you are filing undersection 115 <strong>of</strong> <strong>the</strong> Income Tax Act only because you disposed<strong>of</strong> taxable Canadian property or because you are atreaty-based exempt corporation.Partnerships or joint ventures (alsoco-ownerships, co-tenancies)Use <strong>the</strong> GIFI <strong>to</strong> report your own financial statementinformation, but not <strong>the</strong> financial statement information <strong>of</strong>partnerships or joint ventures you may be involved in.For paper-filed returns, send financial statement informationfor a partnership or joint venture, with your return.For returns filed using <strong>the</strong> Corporation Internet Filingservice, send <strong>the</strong> financial statement information for apartnership or joint venture <strong>to</strong> your tax centre. Include acover letter with your name, Business Number, and yourtaxation year-end. Identify <strong>the</strong> financial statements attachedas those <strong>of</strong> partnerships or joint ventures in which you havean investment. Request <strong>the</strong>se statements be included in <strong>the</strong>file <strong>of</strong> your corporation.Inactive corporationsUse <strong>the</strong> GIFI <strong>to</strong> file your balance sheet information. Youmay have an income statement <strong>to</strong> file. If so, use <strong>the</strong> GIFI <strong>to</strong>file this information.First year after incorporationYou may be filing for <strong>the</strong> first year after incorporation. If so,complete two balance sheets: an opening and a closing. Ifyou are not using a s<strong>of</strong>tware package approved by us <strong>to</strong>complete this information, and you are using <strong>the</strong> GIFI-Shortform, write “opening” in <strong>the</strong> <strong>to</strong>p right-hand corner <strong>of</strong> <strong>the</strong>appropriate balance sheet. If you are using <strong>the</strong> GIFIschedules, <strong>the</strong> T2SCH100, Balance Sheet <strong>Information</strong>, is for<strong>the</strong> closing balance sheet information and <strong>the</strong> T2SCH101,Opening Balance Sheet <strong>Information</strong>, is for <strong>the</strong> opening balancesheet information.Deferred expense statementsYou may be involved in exploration and development thathas not yet generated significant sales revenue, and youmay have capitalized deferred expenditures. If so, do notuse <strong>the</strong> GIFI <strong>to</strong> itemize <strong>the</strong>se expenditures. You shouldreport <strong>the</strong> aggregate deferred expenditures as balance sheetinformation. As well, you have <strong>to</strong> report “0” in <strong>the</strong> requiredfields on your income statement information (see “Validitycheck items” on this page).Reporting in Canadian fundsReport your financial statement information in Canadianfunds even if you are a Canadian branch <strong>of</strong> a foreigncorporation.Reporting negative amountsIf you are using a s<strong>of</strong>tware package, it will show you how<strong>to</strong> mark items as negative amounts. If you do not use as<strong>of</strong>tware package, you should mark negative amountsusing brackets ( ) or a minus sign “–”.Reporting in dollarsReport your financial statement amounts in actual dollars;do not report cents (for example, report cash <strong>of</strong> $10,500.75as 10501 at line 1001 – Cash). Do not report amounts inthousands (000) or millions <strong>of</strong> dollars.Reporting unconsolidated financialstatement informationReport your financial statement information for each legalentity (unconsolidated). Include all unincorporatedbranches or divisions within that legal corporate entity.Reporting multiple lines <strong>of</strong> businessYou may have multiple lines <strong>of</strong> business. For moreinformation on how <strong>to</strong> report this type <strong>of</strong> situation using<strong>the</strong> GIFI, see Appendix B on page 26.Using <strong>the</strong> GIFI1. Select <strong>the</strong> items usually reported on your balance sheetfrom items in <strong>the</strong> 1000 <strong>to</strong> 3849 range.2. Select <strong>the</strong> items usually reported on your incomestatement from items in <strong>the</strong> 8000 <strong>to</strong> 9970 range.NoteItems 9370 <strong>to</strong> 9899 relate specifically <strong>to</strong> farming incomeand expenses.3. Select <strong>the</strong> items usually reported on your extraordinaryitems and income taxes from items in <strong>the</strong> 9975 <strong>to</strong> 9999range.Validity check itemsThe GIFI information has <strong>to</strong> balance. We use <strong>the</strong> followingrules <strong>to</strong> verify <strong>the</strong> information you provide.www.cra.gc.ca 5

■ <strong>to</strong>tal assets = <strong>to</strong>tal liabilities + <strong>to</strong>tal shareholder equity■ <strong>to</strong>tal revenue – <strong>to</strong>tal expenses = net non-farming income■ <strong>to</strong>tal farm revenue – <strong>to</strong>tal farm expenses = net farmincomeYou have <strong>to</strong> provide certain line items so that we can verify<strong>the</strong> above equations. Each GIFI must include:Balance sheetItem 2599 – Total assetsItem 3499 – Total liabilitiesItem 3620 – Total shareholder equityNon-farming income and expensesItem 8299 – Total revenueItem 9368 – Total expensesand/orFarming income and expensesItem 9659 – Total farm revenueItem 9898 – Total farm expensesWhen reporting a breakdown <strong>of</strong> retained earningsItem 3849 – Retained earnings/deficit endExtraordinary items and income taxesItem 9999 – Net income/loss after taxesand extraordinary itemsThe amount <strong>of</strong> a required item may be NIL. If so, enter “0”.NoteThese required fields do not represent <strong>the</strong> minimumnumber <strong>of</strong> items that need <strong>to</strong> be GIFI-coded and filedwith <strong>the</strong> CRA. These are codes that must be included,along with all <strong>the</strong> o<strong>the</strong>r GIFI codes needed <strong>to</strong> represent acorporation’s financial statements.For an example <strong>of</strong> how <strong>to</strong> use <strong>the</strong> GIFI, see page 8How <strong>to</strong> select GIFI itemsThe GIFI consists <strong>of</strong> items you find on a balance sheet andincome statement. The balance sheet section consists <strong>of</strong>items pertaining <strong>to</strong> assets, liabilities, and shareholderequity. Items specific <strong>to</strong> retained earnings are included inthis area as well. The income statement section consists <strong>of</strong>items you find under revenue, cost <strong>of</strong> sales, and expenses.Due <strong>to</strong> <strong>the</strong> specific reporting needs <strong>of</strong> <strong>the</strong> agricultureindustry, we have provided a separate section for farmingrevenue and expenses. A section for extraordinary items andincome taxes is listed after <strong>the</strong> farming section. For acomplete listing <strong>of</strong> GIFI items, see Appendix A on page 12.We have fur<strong>the</strong>r divided <strong>the</strong> GIFI in<strong>to</strong> blocks <strong>of</strong> itemswithin <strong>the</strong>se sections. The item at <strong>the</strong> start <strong>of</strong> each block ishighlighted. This item represents <strong>the</strong> generic term for itemswithin <strong>the</strong> block. You may not find <strong>the</strong> item that is an exact,or close match <strong>to</strong> <strong>the</strong> item on your financial statements. Ifso, use <strong>the</strong> generic item.NoteThe generic item at <strong>the</strong> start <strong>of</strong> each block does notrepresent <strong>the</strong> <strong>to</strong>tal <strong>of</strong> <strong>the</strong> items in <strong>the</strong> block.Assuming that you will prepare <strong>the</strong> GIFI from your ownfinancial statements, use <strong>the</strong> following process when youselect GIFI items:■ try <strong>to</strong> select an exact match from <strong>the</strong> GIFI items on yourfinancial statements;■ if you cannot find an exact match, select <strong>the</strong> mostappropriate item; or■ if you cannot find an appropriate item, select <strong>the</strong> genericitem.Example8760 Business taxes, licences, and memberships8761 Memberships8762 Business taxes8763 Franchise fees8764 Government feesIf your income statement usually shows an account for“business charges”, you could use item 8760 <strong>to</strong> report thisamount.Reporting an amount that combinestwo or more itemsAn amount in your financial statement information maycombine two or more GIFI items. To report this amount,determine which item is <strong>the</strong> greater or greatest amount andchoose <strong>the</strong> most appropriate GIFI item.ExampleCash and term depositsIf cash is <strong>the</strong> greater amount, report in GIFI item 1001 – Cash.If term deposits is <strong>the</strong> greater amount, report in GIFIitem 1181 – Canadian term deposits.ExampleRent, taxes, and insuranceYou could report this in 8911 – Real estate rental, 8762 –Business taxes, or 8690 – Insurance, depending on whichamount is <strong>the</strong> greatest.Completing <strong>the</strong> notes checklistThe notes checklist is included with <strong>the</strong> GIFI in all CRAapproved s<strong>of</strong>tware packages. Complete <strong>the</strong> notes checklistwhen you use <strong>the</strong> GIFI <strong>to</strong> report your financial statementinformation. It should be completed from <strong>the</strong> perspective <strong>of</strong><strong>the</strong> person who prepared or reported on <strong>the</strong> financialstatements. A copy <strong>of</strong> <strong>the</strong> notes checklist is on <strong>the</strong> nextpage.Part 1 – Accounting practitioner informationAnswer <strong>the</strong>se two questions concerning <strong>the</strong> accountingpractitioner who reported on, or prepared <strong>the</strong> financialstatements <strong>of</strong> <strong>the</strong> corporation. Indicate whe<strong>the</strong>r <strong>the</strong>accounting practitioner has a pr<strong>of</strong>essional designation andwhe<strong>the</strong>r <strong>the</strong> practitioner is connected <strong>to</strong> <strong>the</strong> corporation byticking ei<strong>the</strong>r <strong>the</strong> Yes or No box for each question.6www.cra.gc.ca

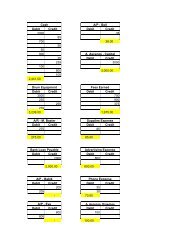

Notes <strong>to</strong> <strong>the</strong> financial statementsYou may have prepared notes <strong>to</strong> <strong>the</strong> financial statements. Ifso, include <strong>the</strong>m with <strong>the</strong> GIFI. If you file electronically,you must include <strong>the</strong> notes with your transmission. Yours<strong>of</strong>tware package should enable you <strong>to</strong> transfer <strong>the</strong> notes <strong>to</strong><strong>the</strong> file you are transmitting, without re-keying.NotesYou cannot include tables and graphs in <strong>the</strong> notes if youare filing electronically. You must convert this type <strong>of</strong>information <strong>to</strong> plain text.You may choose <strong>to</strong> report on <strong>the</strong> GIFI breakdowns <strong>of</strong>items such as capital assets or investments shown in <strong>the</strong>notes.ExampleYour balance sheet shows fixed assets <strong>of</strong> $31,500, with a breakdown found in <strong>the</strong> notes.Cost Accumulated amortization NetLand $ 10,000 $ 10,000Buildings $ 20,000 $ 3,000 $ 17,000Furniture and fixtures $ 5,000 $ 500 $ 4,500Total $ 35,000 $ 3,500 $ 31,500Using <strong>the</strong> GIFI, you could report <strong>the</strong> information from <strong>the</strong> notes as follows:GIFI Code Item Amount1600 Land 10,0001680 Buildings 20,0001681 Accumulated amortization <strong>of</strong> buildings (3,000)1787 Furniture and fixtures 5,0001788 Accumulated amortization <strong>of</strong> furniture and fixtures (500)2008 Total tangible capital assets 35,0002009 Total accumulated amortization <strong>of</strong> tangible capital assets (3,500)Example – Using <strong>the</strong> GIFIThe following example represents a typical set <strong>of</strong> financialstatements.■ Part 1 shows <strong>the</strong> item and amount reported on <strong>the</strong>financial statement, and <strong>the</strong> corresponding GIFI code andname.■ Part 2 shows just <strong>the</strong> GIFI codes and amountsrepresenting what <strong>the</strong> CRA receives ei<strong>the</strong>r electronicallyor on paper if you use a s<strong>of</strong>tware package <strong>to</strong> report yourfinancial statement information.NoteThis example is only a guideline. It is not meant <strong>to</strong>dictate what <strong>to</strong> put on your statements or how <strong>to</strong> file.Example 1Part 1Item description $ Amount GIFI code and nameBalance SheetAssetsCash 2,540 1001 CashAccounts receivable(net <strong>of</strong> allowance for 1060 Accounts receivable*doubtful accounts <strong>of</strong> $25) 331 or1060 Accounts receivable1061 Allowance for doubtful accountsInven<strong>to</strong>ry 8,947 1120 Inven<strong>to</strong>riesPrepaid expenses 1,813 1484 Prepaid expenses13,631 1599 Total current assetsFixed assets (note 2) 49,803 2008 Total tangible capital assetsInvestment (note 3) 1,000 2242 Shares in Canadian related corporations64,434 2599 Total assets* You could choose <strong>to</strong> show <strong>the</strong> net amount <strong>of</strong> accounts receivable or accounts receivable and allowance for doubtfulaccounts.8www.cra.gc.ca

Item description $ Amount GIFI code and nameLiabilitiesBank indebtedness 5,000 2600 Bank overdraftAccounts payable 6,797 2621 Trade payablesCurrent portion <strong>of</strong> bank loan liability 5,104 2920 Current portion <strong>of</strong> long term liability16,901 3139 Total current liabilitiesBank loan 64,634 3143 Chartered bank loanDue <strong>to</strong> shareholders, unsecuredwith no fixed terms 29,900 3260 Due <strong>to</strong> shareholder(s)/direc<strong>to</strong>r(s)94,534 3450 Total long term liabilities111,435 3499 Total liabilitiesShareholder Equity1500 common shares 1,500 3500 Common sharesDeficit (48,501) 3600 Retained earnings/deficit(47,001) 3620 Total shareholder equityStatement <strong>of</strong> Income and Retained EarningsRevenuePr<strong>of</strong>essional services 191,396 8000 Trade sales <strong>of</strong> goods and services8299 Total revenueExpensesAdvertising 675 8521 AdvertisingAmortization 15,708 8670 Amortization <strong>of</strong> tangible assetsAssociation dues 1,575 8761 MembershipsBank charges and interest 8,564 8710 Interest and bank chargesBusiness taxes 5,789 8762 Business taxesInsurance and licences 3,988 8690 Insurance*Office 3,137 8810 Office expensesPr<strong>of</strong>essional fees 975 8860 Pr<strong>of</strong>essional feesRent 45,703 8911 Real estate rentalRepairs and maintenance 1,255 8960 Repairs and maintenanceSupplies 37,591 9130 SuppliesTelephone and utilities 5,512 9225 Telephone and telecommunications*Travel and education 360 9200 Travel expenses*Wages and benefits 55,118 9060 Salaries and wages*185,950 9368 Total expensesNet income before taxes 5,446 9369 Net non-farming incomeIncome taxes 1,400 9990 Current income taxesNet income (loss) 4,046 9999 Net income/loss after taxes and extraordinary itemsRetained EarningsNet income (loss) 4,046 3680 Net income/lossDeficit, beginning <strong>of</strong> year (52,547) 3660 Retained earnings/deficit – startDeficit, end <strong>of</strong> year (48,501) 3849 Retained earnings/deficit – end* First item in two-item amount is greater (see “Reporting an amount that combines two or more items” on page 6).Notes <strong>to</strong> financial statementsNote 1. Basis <strong>of</strong> PresentationThe financial statements have been prepared by management in accordance with accounting principles generally acceptedin Canada and using his<strong>to</strong>ric cost as <strong>the</strong> basis <strong>of</strong> presentation.www.cra.gc.ca 9

Part 2 – GIFI code and amount sent <strong>to</strong> <strong>the</strong> CRAGIFI code Amount GIFI code Amount1001 2540 3680 40461060 331 3660 (52547)or 3849 (48501)1060 356 8000 1913961061 25 8299 1913968521 6751120 8947 8670 157081484 1813 8761 15751599 13631 8710 85648762 57892008 49803 8690 39882242 1000 8810 31372599 64434 8860 9752600 5000 8911 457032621 6797 8960 12552920 5104 9130 375913139 16901 9225 55123143 64634 9200 3603260 29900 9060 551183450 94534 9368 1859503499 111435 9369 54463500 1500 9990 14003600 (48501) 9999 40463620 (47001)Bolded amounts show items for which we need <strong>to</strong> verify accounting equations (see “Validity check items” on page 5).Notes checklistGIFI codeValue095 1097 2198 3099 No value is needed for question 99, since <strong>the</strong> answer <strong>to</strong> question 198 is “3.”101 1102 2103 2104 2105 2106 2107 2108 2109 No value is needed for question 109, as <strong>the</strong> answer <strong>to</strong> question 108 is “No.”In this example, all Parts <strong>of</strong> <strong>the</strong> Notes Checklist need <strong>to</strong> be completed because <strong>the</strong> accounting practitioner who prepared <strong>the</strong>financial statements has a pr<strong>of</strong>essional designation and is not connected <strong>to</strong> <strong>the</strong> corporation.Notes <strong>to</strong> <strong>the</strong> financial statementsIf you file a paper return, attach <strong>the</strong> notes <strong>to</strong> <strong>the</strong> financial statements <strong>to</strong> this GIFI listing. If you file electronically, include<strong>the</strong>m in <strong>the</strong> transmission.www.cra.gc.ca 11

Appendix A – Complete Listing <strong>of</strong> <strong>the</strong> GIFIThe following is a complete list <strong>of</strong> <strong>the</strong> GIFI items. Some<strong>of</strong> <strong>the</strong> items include more detail as <strong>to</strong> <strong>the</strong> type <strong>of</strong>information you could report in <strong>the</strong> item.Example1001 CashYou can use this item <strong>to</strong> report bank drafts, bank notes,cheques, coins, currency, money orders, postal notes, andpost-dated cheques, as well as cash.9012 Road costsYou could use this item <strong>to</strong> report snow removal as well asroad costs.Balance Sheet <strong>Information</strong>AssetsCurrent assets1000 Cash and deposits1001 Cashbank drafts, bank notes, cheques, coins, currency, moneyorders, postal notes, and post-dated cheques1002 Deposits in Canadian banks and institutions –Canadian currency1003 Deposits in Canadian banks and institutions –foreign currency1004 Deposits in foreign banks – Canadian currency1005 Deposits in foreign banks – foreign currency1006 Credit union central deposits1007 O<strong>the</strong>r cash like instrumentsgold bullion and silver bullion1060 Accounts receivableclaims, dividends, royalties, and subsidies receivable1061 Allowance for doubtful accounts1062 Trade accounts receivable1063 Allowance for doubtful trade accounts receivable1064 Trade accounts receivable from related parties1065 Allowance for doubtful trade accounts receivablefrom related parties1066 Taxes receivableGST/HST, income tax refunds, and tax creditsreceivable1067 Interest receivable1068 Holdbacks receivable1069 Leases receivable1070 Allowance for doubtful amounts contained inleases receivable1071 Accounts receivable from employees1072 Allowance for doubtful accounts receivable fromemployees1073 Amounts receivable from members <strong>of</strong> NPOsthis item is intended for corporations that are non-pr<strong>of</strong>i<strong>to</strong>rganizations – <strong>to</strong> report amounts receivable frommembers1120 Inven<strong>to</strong>ries1121 Inven<strong>to</strong>ry <strong>of</strong> goods for salefinished goods1122 Inven<strong>to</strong>ry parts and supplies1123 Inven<strong>to</strong>ry propertiesthis item is intended for companies whose primaryactivities are real estate, subdividing, or construction,and who have real estate held for sale1124 Inven<strong>to</strong>ry <strong>of</strong> aggregates1125 Work in progressgoods in process1126 Raw materials1127 Inven<strong>to</strong>ry <strong>of</strong> securitiesthis item is intended for companies such as brokers,s<strong>to</strong>ckbrokers, financial institutions, or investmentcompanies that hold securities for sale1180 Short-term investmentsshort-term marketable securities1181 Canadian term depositsshort-term bearer deposit notes, collateral deposits, andguaranteed investment certificates1182 Canadian shares1183 Canadian bondsbond coupons, bond deposits, corporate bonds,government bonds, and debentures shown current1184 Canadian treasury bills1185 Securities purchased under resale agreements1186 O<strong>the</strong>r short-term Canadian investments1187 Short-term foreign investmentsall types <strong>of</strong> foreign investment shown current1240 Loans and notes receivable1241 Demand loans receivableamounts such as call loans, day loans, or demand loans1242 O<strong>the</strong>r loans receivable1243 Notes receivable1244 Mortgages receivableItems 1300 <strong>to</strong> 1303 – current amounts due fromshareholders/direc<strong>to</strong>rs, such as advances, loans, or notes1300 Due from shareholder(s)/direc<strong>to</strong>r(s)1301 Due from individual shareholder(s)1302 Due from corporate shareholder(s)due from parent company1303 Due from direc<strong>to</strong>r(s)1360 Investment in joint venture(s)/partnership(s)current investment or equity in joint venture(s),partnership(s), and syndicate(s)1380 Due from joint venture(s)/partnership(s)current amounts due from jointventure(s)/partnership(s), or syndicate(s), such asadvances, loans, or notes12www.cra.gc.ca

Items 1400 <strong>to</strong> 1403 – Related parties can refer <strong>to</strong> affiliate,associated, and subsidiary corporations.NoteCurrent investment in a parent company should bereported at item 1400. However, item 1302 should beused for current due from a parent company.1400 Due from/investment in related parties1401 Demand notes from related partiesamounts due from related parties such as call loans, dayloans, or demand loans1402 Interest receivable from related parties1403 Loans/advances due from related parties1460 Cus<strong>to</strong>mers’ liability under acceptancesthis item is for financial institutions – any amountreported in this item should be equal <strong>to</strong> <strong>the</strong> amountreported in <strong>the</strong> Liabilities section as “acceptances”(i.e., Item 2940 – Bankers’ acceptances)1480 O<strong>the</strong>r current assets1481 Future (deferred) income taxesincome taxes applicable <strong>to</strong> future years, and reserve forincome taxes, shown current1482 Accrued investment income1483 Taxes recoverable/refundable1484 Prepaid expenses1485 Drilling advances1486 Security/tender deposits1599 Total current assetsCapital assetsItems 1600 <strong>to</strong> 2179 – capital assets – Throughout <strong>the</strong> GIFI,depreciation is referred <strong>to</strong> as amortization <strong>of</strong> tangible assets,depletion is referred <strong>to</strong> as amortization <strong>of</strong> natural resource assets,and amortization is referred <strong>to</strong> as amortization <strong>of</strong> intangibleassets.Items 1600 <strong>to</strong> 2009 – tangible capital assets – Item 2008 –Total tangible capital assets, represents <strong>the</strong> sum <strong>of</strong> all tangiblecapital assets reported, and item 2009 – Total accumulatedamortization <strong>of</strong> tangible capital assets, represents <strong>the</strong> sum <strong>of</strong> all<strong>the</strong> accumulated amortization <strong>of</strong> <strong>the</strong> tangible capital assetsreported, within items 1600 <strong>to</strong> 1922.When reporting this breakdown, <strong>the</strong> net final amount <strong>of</strong> <strong>the</strong>tangible capital assets is not <strong>to</strong> be shown anywhere on <strong>the</strong> GIFI.However, if your financial statements show an amount for “fixedassets (net)” for which <strong>the</strong>re is no breakdown, this could bereported in Item 2008 – Total tangible capital assets.1600 Land1601 Land improvementslandscaping1602 Accumulated amortization <strong>of</strong> land improvements1620 Depletable assetscosts for mine-stripping, well drilling, or waste removal1621 Accumulated amortization <strong>of</strong> depletable assets1622 Petroleum and natural gas properties1623 Accumulated amortization <strong>of</strong> petroleum andnatural gas properties1624 Mining properties1625 Accumulated amortization <strong>of</strong> mining properties1626 Deferred exploration and development charges1627 Accumulated amortization <strong>of</strong> deferred explorationand development charges1628 Quarries1629 Accumulated amortization <strong>of</strong> quarries1630 Gravel pits1631 Accumulated amortization <strong>of</strong> gravel pits1632 Timber limits1633 Accumulated amortization <strong>of</strong> timber limits1680 Buildings1681 Accumulated amortization <strong>of</strong> buildings1682 Manufacturing and processing plant1683 Accumulated amortization <strong>of</strong> manufacturing andprocessing plant1684 Buildings under construction1740 Machinery, equipment, furniture, and fixtures1741 Accumulated amortization <strong>of</strong> machinery,equipment, furniture, and fixtures1742 Mo<strong>to</strong>r vehicles1743 Accumulated amortization <strong>of</strong> mo<strong>to</strong>r vehicles1744 Tools and dies1745 Accumulated amortization <strong>of</strong> <strong>to</strong>ols and dies1746 Construction and excavating equipment1747 Accumulated amortization <strong>of</strong> construction andexcavating equipment1748 Forestry and logging equipment1749 Accumulated amortization <strong>of</strong> forestry and loggingequipment1750 Fishing gear and netssonar equipment1751 Accumulated amortization <strong>of</strong> fishing gear and nets1752 Mining equipment1753 Accumulated amortization <strong>of</strong> mining equipment1754 Oil and gas systemspipelines and distribution systems1755 Accumulated amortization <strong>of</strong> oil and gas systems1756 Production equipment for resource industries1757 Accumulated amortization <strong>of</strong> productionequipment for resource industries1758 Production equipment for o<strong>the</strong>r than resourceindustries1759 Accumulated amortization <strong>of</strong> productionequipment for o<strong>the</strong>r than resource industries1760 Exploration equipment1761 Accumulated amortization <strong>of</strong> explorationequipment1762 Shipping equipment1763 Accumulated amortization <strong>of</strong> shipping equipment1764 Ships and boats1765 Accumulated amortization <strong>of</strong> ships and boats1766 Aircraft1767 Accumulated amortization <strong>of</strong> aircraft1768 Signs1769 Accumulated amortization <strong>of</strong> signs1770 Small <strong>to</strong>ols1771 Accumulated amortization <strong>of</strong> small <strong>to</strong>ols1772 Radio and communication equipment1773 Accumulated amortization <strong>of</strong> radio andcommunication equipmentwww.cra.gc.ca 13

2220 Due from joint venture(s)/partnership(s)long-term amounts due from jointventure(s)/partnership(s), or syndicate(s), such asadvances, loans, or notesItems 2240 <strong>to</strong> 2250 – Related parties can refer <strong>to</strong> affiliate,associated, and subsidiary corporations.NoteLong-term investment in a parent company should bereported in <strong>the</strong> appropriate item in this block. However,item 2182 – Due from corporate shareholders, should beused for long-term amounts due from a parent company.2240 Due from/investment in related parties2241 Due from/investment in Canadian related parties2242 Shares in Canadian related corporations2243 Loans/advances <strong>to</strong> Canadian related corporations2244 Investment in Canadian related corporations atcost2245 Investment in Canadian related corporations atequity2246 Due from/investment in foreign related parties2247 Shares in foreign related corporations2248 Loans/advances <strong>to</strong> foreign related corporations2249 Investment in foreign related corporations at cost2250 Investment in foreign related corporations atequity2280 Investment in co-tenancyinvestment in co-ownerships2300 Long term investments2301 Foreign shares2302 O<strong>the</strong>r types <strong>of</strong> foreign investmentsforeign investments in joint ventures, partnerships,bonds, and debentures2303 Canadian shares2304 Government <strong>of</strong> Canada debtgovernment <strong>of</strong> Canada long-term bonds and debentures2305 Canadian, provincial, and municipal governmentdebt2306 Canadian corporate bonds and debentureslong-term bond coupons and bond deposits2307 Debt securities2308 Equity securities2309 Securities purchased under resale agreements2310 Central credit union shares2311 O<strong>the</strong>r Canadian long-term investments2360 Long-term loansadvances and notes shown long-term2361 Mortgages2362 Personal and credit card loans2363 Business and government loans2364 Line <strong>of</strong> credit2420 O<strong>the</strong>r long-term assetsinvestment tax credits, s<strong>to</strong>ck exchange seats, andutilities deposits2421 Future (deferred) income taxesincome taxes applicable <strong>to</strong> future years, and reserve forincome taxes, shown long term2422 Deferred pension charges2423 Deferred unrealized exchange losses2424 O<strong>the</strong>r deferred items/chargesdebt discount and expense, deferred development costs,deferred finance charges, deferred organization expense,lease inducements, tenant inducements, and cost onincomplete contracts2425 Accumulated amortization <strong>of</strong> deferred charges2426 Reserve fund2427 Cash surrender value <strong>of</strong> life insurance2589 Total long-term assets2590 Assets held in trusttrust fund, trust assets, or funds held in escrowcorporations such as collection agencies, funeral homes,insurance agencies, real estate agencies, travel agencies,and travel wholesalers would use this item – an amountreported in this item should have a balancing amountreported in Item 3470 – Amounts held in trust, in <strong>the</strong>liabilities section2599 Total assetsthis item represents <strong>the</strong> <strong>to</strong>tal <strong>of</strong> all current, capital,long-term assets, and assets held in trust and must bereported (see “Validity check items” on page 5)LiabilitiesCurrent liabilities2600 Bank overdraftbank indebtedness2620 Amounts payable and accrued liabilitiesaccrued liabilities, agreements payable, claims payable,rent payable, and utilities payable2621 Trade payables2622 Trade payables <strong>to</strong> related parties2623 Holdbacks payable2624 Wages payable2625 Management fees payable2626 Bonuses payable2627 Employee deductions payablepayroll deductions for employee benefits such asEmployment Insurance, Canada Pension Plan, QuebecParental Insurance Plan, group insurance, and pensionplans2628 Withholding taxes payable2629 Interest payableaccrued interest payable2630 Amounts payable <strong>to</strong> members <strong>of</strong> NPOsfor corporations that are non-pr<strong>of</strong>it organizations <strong>to</strong>report amounts payable <strong>to</strong> members2680 Taxes payablecapital taxes, foreign taxes, GST/HST, current incometaxes, logging taxes, sales taxes, and tax credits payable2700 Short term debtcorporate loans, demand loans, loans from foreignbanks, and notes payable shown short term2701 Loans from Canadian banks2702 Liability for securities sold short2703 Liability for securities sold under repurchaseagreementswww.cra.gc.ca 15

2704 Gold and silver certificates2705 Cheques and o<strong>the</strong>r items in transit2706 Lien notes2707 Credit card loans2770 Deferred incomedeferred capital or book gain, unearned income,unearned interest, unearned service charges, andunrealized foreign exchange gain shown currentItems 2780 <strong>to</strong> 2783 – current amounts due <strong>to</strong>shareholder(s)/direc<strong>to</strong>r(s), such as advances, loans, or notes2780 Due <strong>to</strong> shareholder(s)/direc<strong>to</strong>r(s)2781 Due <strong>to</strong> individual shareholder(s)2782 Due <strong>to</strong> corporate shareholder(s)due <strong>to</strong> parent company2783 Due <strong>to</strong> direc<strong>to</strong>r(s)2840 Due <strong>to</strong> joint venture(s)/partnership(s)current amounts due <strong>to</strong> joint venture(s)/partnership(s),and syndicate(s) such as advances, loans, or notesItems 2860 <strong>to</strong> 2863 – Related parties can refer <strong>to</strong> affiliate,associated, and subsidiary corporations.2860 Due <strong>to</strong> related parties2861 Demand notes due <strong>to</strong> related parties2862 Interest payable <strong>to</strong> related parties2863 Advances due <strong>to</strong> related parties2920 Current portion <strong>of</strong> long-term liability2940 Bankers’ acceptancesfor financial institutions – any amount reported in thisitem should be equal <strong>to</strong> <strong>the</strong> amount reported in Assets asItem 1460 – Cus<strong>to</strong>mers’ liability under acceptances2960 O<strong>the</strong>r current liabilitiesprogress payments shown current2961 Deposits receivedbids, contract deposits, rental deposits, tenders, andsecurity deposits2962 Dividends payable2963 Future (deferred) income taxesincome taxes applicable <strong>to</strong> future years and reserve forincome taxes shown current2964 Reserves for guarantees, warranties, or indemnities2965 <strong>General</strong> provisions/reservescontingent liabilities, provision for losses on loans, andpension reserves shown current2966 Crew shares3139 Total current liabilitiesLong-term liabilities3140 Long-term debt3141 Mortgages3142 Farm credit corporation loan3143 Chartered bank loan3144 Credit Union/Caisse Populaire loan3145 Provincial or terri<strong>to</strong>rial government loan3146 Supply company loan3147 Private loan3148 Central, league, and federation loans3149 Line <strong>of</strong> credit3150 Liability for securities sold short3151 Liability for securities sold under repurchaseagreements3152 Lien notes3200 Deposit liabilities <strong>of</strong> financial institutionsapplies <strong>to</strong> financial institutions and represents depositsmade by cus<strong>to</strong>mers3210 Bonds and debentures3220 Deferred incomedeferred capital or book gain, unearned income,unearned interest, unearned service charges, andunrealized foreign exchange gain shown long term3240 Future (deferred) income taxesincome taxes applicable <strong>to</strong> future years and reserve forincome taxes shown long termItems 3260 <strong>to</strong> 3263 – long-term amounts due <strong>to</strong>shareholder(s)/direc<strong>to</strong>r(s), such as advances, loans, or notes3260 Due <strong>to</strong> shareholder(s)/direc<strong>to</strong>r(s)3261 Due <strong>to</strong> individual shareholder(s)3262 Due <strong>to</strong> corporate shareholder(s)due <strong>to</strong> parent company3263 Due <strong>to</strong> direc<strong>to</strong>r(s)3270 Due <strong>to</strong> membersadvances, loans, or notes from members <strong>of</strong> co-operativesor credit unions3280 Due <strong>to</strong> joint venture(s)/partnership(s)long-term amounts due <strong>to</strong> jointventure(s)/partnership(s), and syndicate(s) such asadvances, loans, or notesItems 3300 <strong>to</strong> 3302 – Related parties can refer <strong>to</strong> affiliate,associated, and subsidiary corporations.3300 Due <strong>to</strong> related parties3301 Amounts owing <strong>to</strong> related Canadian parties3302 Amounts owing <strong>to</strong> related foreign parties3320 O<strong>the</strong>r long-term liabilitiesminority shareholder interest and o<strong>the</strong>r deferred creditsshown long term3321 Long-term obligations/commitments/capitalleases3322 Reserves for guarantees, warranties, or indemnities3323 Provision for site res<strong>to</strong>rationdismantlement and abandonment costs, future removal,and site res<strong>to</strong>ration costs3324 Contributions <strong>to</strong> qualifying environmental trustenvironmental trust, mine reclamation, and reclamation<strong>of</strong> waste disposal sites3325 <strong>General</strong> provisions/reservescontingent liabilities, provision for losses on loans, andpension reserves shown long term3326 Preference shares restatedapplies <strong>to</strong> preferred shares that have been restated as aliability and reported as a long-term liability16www.cra.gc.ca

3327 Member allocationsallocation <strong>to</strong> members <strong>of</strong> credit unions and co-operatives3328 Deferred revenue from incomplete contractsintended for contrac<strong>to</strong>rs using <strong>the</strong> completion method <strong>of</strong>reporting revenue <strong>to</strong> report deferred revenue fromincomplete contracts3450 Total long-term liabilities3460 Subordinated debt3470 Amounts held in trusttrust fund, trust liabilities, or funds held in escrow,corporations such as collection agencies, funeral homes,insurance agencies, real estate agencies, travel agencies,and travel wholesalers would use this item – an amountreported in this item should have a balancing amountreported in Item 2590 – Assets held in trust, in <strong>the</strong>assets section3499 Total liabilitiesthis item represents <strong>the</strong> <strong>to</strong>tal <strong>of</strong> all current andlong-term liabilities and must be reported (see “Validitycheck items” on page 5)Shareholder equity3500 Common shares3520 Preferred shares3540 Contributed and o<strong>the</strong>r surplus3541 Contributed surpluscapital donations, capital grants, and paid-in surplus3542 Appraisal surplusexcess <strong>of</strong> appraisal value over cost, revaluation account,and revaluation surplus3543 <strong>General</strong> reservegeneral reserves, inven<strong>to</strong>ry reserves, mortgage reserves,and security reserves3570 Head <strong>of</strong>fice accounthome <strong>of</strong>fice account and head <strong>of</strong>fice investment3600 Retained earnings/deficit3620 Total shareholder equitythis item represents <strong>the</strong> sum <strong>of</strong> all shareholder equityamounts and must be reported (see “Validity checkitems” on page 5)3640 Total liabilities and shareholder equityRetained Earnings <strong>Information</strong>Retained earnings/deficit3660 Retained earnings/deficit – start3680 Net income/lossany amount reported in this item should be equal <strong>to</strong> <strong>the</strong>amount reported at Item 9999 – Net income/loss aftertaxes and extraordinary items3720 Prior period adjustments3740 O<strong>the</strong>r items affecting retained earningsdividends credited <strong>to</strong> investment account –if you choose <strong>to</strong> report dividends received in retainedearnings ra<strong>the</strong>r than on <strong>the</strong> income statement add <strong>the</strong>dividend back on Schedule 1 – Net income (loss) forincome tax purposes3741 Share redemptions3742 Special reserves3743 Currency adjustments3744 Unusual revenue items3745 Interfund transferintended for corporations that are non-pr<strong>of</strong>i<strong>to</strong>rganizations <strong>to</strong> report fund amounts transferred<strong>to</strong>/from retained earning from/<strong>to</strong> <strong>the</strong> income statement3849 Retained earnings/deficit – endthis item represents <strong>the</strong> sum <strong>of</strong> all retained earningsamounts and must be reported if you are reportingretained earnings (see “Validity check items” on page 5)– an amount reported in this item should be <strong>the</strong> sameamount reported in Item 3600 – Retainedearnings/deficit, in <strong>the</strong> shareholder equity sectionIncome Statement <strong>Information</strong>0001 Operating namecomplete this section if <strong>the</strong> operating name is differentfrom <strong>the</strong> corporation name (e.g., 111111 Ontario Ltd.,operating as Maggie’s Muffins)0002 Description <strong>of</strong> <strong>the</strong> operationcomplete <strong>the</strong> description <strong>of</strong> <strong>the</strong> operation when reportingmore than one income statement, and <strong>the</strong> activity isdifferent from <strong>the</strong> major business activity – refer <strong>to</strong>Appendix B <strong>of</strong> this guide for more information onreporting multiple lines <strong>of</strong> business0003 Sequence Numberfor more than one income statement, use sequencenumbers for each statement – number 01 for <strong>the</strong> incomestatement relating <strong>to</strong> <strong>the</strong> main activity withsupplementary income statements numberedconsecutively from 02Revenue8000 Trade sales <strong>of</strong> goods and servicesthis item is for corporations who are not involved in <strong>the</strong>resource industry (Items 8040 <strong>to</strong> 8053) or <strong>the</strong> fishingindustry (Items 8160 <strong>to</strong> 8166), but whose main source<strong>of</strong> income is <strong>the</strong> sale <strong>of</strong> a product or service – amounts inmay be reported net <strong>of</strong> discounts allowed on sales, salesrebates, volume discounts, returns, and allowances8020 Sales <strong>of</strong> goods and services <strong>to</strong> related partiessee explanation for item 8000 above8030 Interdivisional sales3700 Dividends declaredliquidating dividends, premium paid on redemption <strong>of</strong>shares, and s<strong>to</strong>ck dividends declared on shares3701 Cash dividends3702 Patronage dividendswww.cra.gc.ca 17

8040 Sales from resource properties8041 Petroleum and natural gas sales8042 Petroleum and natural gas sales <strong>to</strong> related parties8043 Gas marketing8044 Processing revenue8045 Pipeline revenue8046 Seismic sales8047 Mining revenue8048 Coal revenue8049 Oil sands revenue8050 Royalty income8051 Oil and gas partnership/joint venture income/loss8052 Mining partnership/joint venture income/loss8053 O<strong>the</strong>r production revenuewell operating fees and sulphur revenue8089 Total sales <strong>of</strong> goods and services8090 Investment revenue8091 Interest from foreign sourcesmay be reported as gross <strong>of</strong> withholding taxes –withholding taxes would <strong>the</strong>n be reported inItem 9283 – Withholding taxes8092 Interest from Canadian bonds and debentures8093 Interest from Canadian mortgage loans8094 Interest from o<strong>the</strong>r Canadian sourcesfinance income, guaranteed investment certificatesinterest, interest on overpaid taxes, and loan interest8095 Dividend income8096 Dividends from Canadian sources8097 Dividends from foreign sourcesmay be reported gross <strong>of</strong> withholding taxes –withholding taxes would <strong>the</strong>n be reported inItem 9283 – Withholding taxes8100 Interest income (financial institutions)8101 Loan interest8102 Securities interest8103 Deposits with banks interest8120 Commission revenuecommissions earned on <strong>the</strong> sale <strong>of</strong> products or servicesby businesses such as advertising agencies, brokers,insurance agents, lottery ticket sales, salesrepresentatives, or travel agenciessome corporations may present sales and cost <strong>of</strong> sales on<strong>the</strong>ir income statement, with commission earned being<strong>the</strong> net amount – report only <strong>the</strong> commission on <strong>the</strong>GIFIExampleLottery ticket sales $40,000Cost <strong>of</strong> lottery tickets $25,000Commission $15,000This would be reported as:Item 8120 – Commission revenue 150008140 Rental revenuerevenue from <strong>the</strong> renting <strong>of</strong> boats, hotel or motel rooms,machinery or equipment, and s<strong>to</strong>rage lockers8141 Real estate rental revenueamounts received as income from renting or leasing <strong>of</strong>apartments, commercial buildings, land, <strong>of</strong>fice space,residential housing, and shopping centresmay also use <strong>to</strong> report income from investments inco-tenancies and co-ownerships8142 Film rental revenue8150 Vehicle leasinglong-term vehicle leasing and short term vehicle leasing8160 Fishing revenue8161 Fish products8162 O<strong>the</strong>r marine productsamounts received from <strong>the</strong> sale <strong>of</strong> flippers, herring roe,herring scales, Irish moss, kelp, seal meat, and seaweed8163 Fishing grants, credits, and rebates8164 Fishing subsidies8165 Compensation for loss <strong>of</strong> fishing income orpropertyamounts received from The Atlantic GroundfishStrategy (TAGS) or insurance proceeds8166 Sharesman incomeItems 8210 <strong>to</strong> 8212 – realized gains/losses on disposal <strong>of</strong>assets – These items represent <strong>the</strong> net amount <strong>of</strong> proceeds overnet book value on <strong>the</strong> disposal or sale <strong>of</strong> an asset.NoteLosses on disposal/sale <strong>of</strong> assets shown as an expenseshould be reported in <strong>the</strong>se items as a negative.8210 Realized gains/losses on disposal <strong>of</strong> assetsgain/loss or pr<strong>of</strong>it/loss on disposal/sale <strong>of</strong> capital assets8211 Realized gains/losses on sale <strong>of</strong> investmentspr<strong>of</strong>it/loss on disposal <strong>of</strong> investments or marketablesecurities8212 Realized gains/losses on sale <strong>of</strong> resourceproperties8220 NPO amounts received8221 Membership fees8222 Assessments8223 Gifts8224 Gross sales and revenues from organizationalactivitiesItems 8230 <strong>to</strong> 8250 – o<strong>the</strong>r revenue – This block <strong>of</strong> items is forsecondary sources <strong>of</strong> income. Although <strong>the</strong>re are items in thisblock that are <strong>of</strong>ten main sources <strong>of</strong> income, Item 8000 – Tradesales <strong>of</strong> goods and services, should still be used <strong>to</strong> report <strong>the</strong> mainincome.compensation could also be reported in this item (forexample, compensation for collecting sales tax)8121 Commission income on real estate transactions18www.cra.gc.ca

ExampleA corporation, whose main source <strong>of</strong> revenue is consultingfees, would choose Item 8000 – Trade sales <strong>of</strong> goods andservices, <strong>to</strong> report this income.However, if <strong>the</strong> corporation’s main source <strong>of</strong> income isfrom architectural design, but <strong>the</strong>re is secondary incomefrom consulting, <strong>the</strong> architectural income would bereported in Item 8000 and <strong>the</strong> consulting income inItem 8241 – Consulting fees.8230 O<strong>the</strong>r revenuegains on settlement <strong>of</strong> a debt and miscellaneous revenue8231 Foreign exchange gains/lossesamortization <strong>of</strong> deferred exchange gains and losses andrealized gains and losses on foreign currency8232 Income/loss <strong>of</strong> subsidiaries/affiliatesfor corporations that report investment in subsidiarycorporations on <strong>the</strong> equity basis8233 Income/loss <strong>of</strong> o<strong>the</strong>r divisions8234 Income/loss <strong>of</strong> joint venturesfor corporations that report investments in jointventures on <strong>the</strong> equity basis8235 Income/loss <strong>of</strong> partnershipsfor corporations that report investments in partnershipson <strong>the</strong> equity basisNoteA loss on foreign exchange, subsidiaries/affiliates, o<strong>the</strong>rdivisions, joint ventures or partnerships shown as anexpense should be reported in <strong>the</strong> appropriate item(Items 8231 <strong>to</strong> 8235) as a negative.8236 Realization <strong>of</strong> deferred revenuesrealization <strong>of</strong> interest income, realization <strong>of</strong> instalmentpayments, and realization <strong>of</strong> service charges8237 Royalty income o<strong>the</strong>r than resourceroyalty income or royalty fees from computer programs,copyrights, motion pictures, or patents8238 Alberta royalty tax credits8239 Management and administration fees8240 Telecommunications revenue8241 Consulting fees8242 Subsidies and grantsgovernment assistance and subvention payments (fornon-fishing corporations), federal, provincial, terri<strong>to</strong>rial,or municipal grants received by corporations that arenon-pr<strong>of</strong>it organizations8243 Sale <strong>of</strong> by-productssecondary income earned by a garage selling discardedoil or tires <strong>to</strong> be used for o<strong>the</strong>r than <strong>the</strong> intended use, ora restaurant selling discarded food as pig feed8244 Deposit services8245 Credit services8246 Card services8247 Patronage dividends8248 Insurance recoverieslife insurance proceeds on <strong>the</strong> death <strong>of</strong> insuredexecutives8249 Expense recoveries8250 Bad debt recoveries8299 Total revenuerepresents <strong>the</strong> sum <strong>of</strong> all revenue amounts and must bereported if <strong>the</strong>re is no farming revenue (see “Validitycheck items” on page 5)Cost <strong>of</strong> sales8300 Opening inven<strong>to</strong>ry8301 Opening inven<strong>to</strong>ry – finished goods8302 Opening inven<strong>to</strong>ry – raw materials8303 Opening inven<strong>to</strong>ry – goods in processopening inven<strong>to</strong>ry – work in progress8320 Purchases/cost <strong>of</strong> materialscost <strong>of</strong> merchandise sold, fuel and purchased power,manufacturing supplies used, materials, andmerchandise purchasedmay be reported net <strong>of</strong> discounts earned on purchases8340 Direct wagescommissions, labour, production wages, and supervisionwhen shown in cost <strong>of</strong> sales8350 Benefits on direct wages8360 Trades and sub-contractscontract labour, cus<strong>to</strong>m work, sub-contract labour, andoutside labour8370 Production costs o<strong>the</strong>r than resource8400 Resource production costsgas processing, oil and gas operating expenses, oil andgas production, milling, smelting, and refining8401 Pipeline operations8402 Drilling8403 Site res<strong>to</strong>ration costsfuture removal costs8404 Gross overriding royalty8405 Freehold royalties8406 O<strong>the</strong>r producing properties rentalfreehold lease rentals and freehold delay rentals8407 Prospect/geologicaldigital processing, geochemical work, geophysical work,gravity meters, magnetic playbacks, seismographs,staking, and velocity surveys8408 Well operating, fuel and equipment8409 Well abandonment and dry holes8410 O<strong>the</strong>r lease rentals8411 Exploration expensesaerial surveys8412 Development expensesstripping costs8435 Crown charges8436 Crown royalties8437 Crown lease rentals8438 Freehold mineral tax8439 Mining taxes8440 Oil sand leases8441 Saskatchewan resource surcharge8450 O<strong>the</strong>r direct costs8451 Equipment hire and operationwww.cra.gc.ca 19

8452 Log yardbarker, bucking, clipper, log sorting, and sawing8453 Forestry costscutting, firefighting supplies, scaling, and silviculture8454 Logging road costsroad clearing, ploughing, and grating8455 Stumpage costs8456 Royalty costsroyalties paid <strong>to</strong> holders <strong>of</strong> copyrights, movies, patents,performing rights, and trademarks, found in cost <strong>of</strong>sales8457 Freight in and dutycus<strong>to</strong>ms and excise duty8458 Inven<strong>to</strong>ry write downrevaluation <strong>of</strong> inven<strong>to</strong>ry and inven<strong>to</strong>ry adjustments8459 Direct cost amortization <strong>of</strong> tangible assetsamortization <strong>of</strong> leasehold improvements and amountsreferred <strong>to</strong> as depreciation shown in cost <strong>of</strong> sales8460 Direct cost amortization <strong>of</strong> natural resource assetsamounts referred <strong>to</strong> as depletion shown in cost <strong>of</strong> sales8461 Overhead expenses allocated <strong>to</strong> cost <strong>of</strong> salesamounts reported under cost <strong>of</strong> sales that are normallyconsidered operating expenses8500 Closing inven<strong>to</strong>ry8501 Closing inven<strong>to</strong>ry – finished goods8502 Closing inven<strong>to</strong>ry – raw materials8503 Closing inven<strong>to</strong>ry – goods in processclosing inven<strong>to</strong>ry – work in progress8518 Cost <strong>of</strong> salesrepresents <strong>the</strong> sum <strong>of</strong> all cost <strong>of</strong> sales amounts8519 Gross pr<strong>of</strong>it/lossrepresents <strong>the</strong> net amount <strong>of</strong> Item 8089 – Total sales <strong>of</strong>goods and services, less Item 8518 – Cost <strong>of</strong> sales – mayalso be referred <strong>to</strong> as gross marginOperating expenses8520 Advertising and promotion8521 Advertisingcatalogues, media expenses, and publications8522 Donationscharitable donations, donations <strong>to</strong> <strong>the</strong> crown, andpolitical donations8523 Meals and entertainmenttickets (<strong>the</strong>atre, concert, athletic event, etc.)8524 Promotionbooths, demonstrations/presentations, displays,prospectus, samples, and seminars (given)8570 Amortization <strong>of</strong> intangible assetsamortization <strong>of</strong> intangible assets such as deferredcharges, goodwill (prior <strong>to</strong> 2002), patents, franchises,copyrights, trademarks, organization costs, and researchand development costs8571 Goodwill impairment lossapplies <strong>to</strong> 2002 and subsequent tax years8590 Bad debt expenseallowance for bad debts, allowance/provision fordoubtful accounts, bad debt, bad debt written-<strong>of</strong>f,provision for bad debts, and reserve for bad debt8610 Loan lossesfor loans, mortgages, and o<strong>the</strong>r loan-type amountswritten <strong>of</strong>f8611 Provision for loan lossesprovision/allowance for loan, mortgage, or credit losses8620 Employee benefitsassociation dues, clothing allowance, lodging, payrolldeductions/levies/taxes, and room and board8621 Group insurance benefitsmedical, dental, and life insurance plans8622 Employer’s portion <strong>of</strong> employee benefitsCanada Pension Plan, company pension plan,Employment Insurance, Quebec Parental InsurancePlan, and Workers’ Compensation8623 Contributions <strong>to</strong> deferred income planscontributions <strong>to</strong> a registered pension plan, deferredpr<strong>of</strong>it sharing plan, employee pr<strong>of</strong>it sharing plan, andregistered supplementary unemployment benefit plan8650 Amortization <strong>of</strong> natural resource assetsamounts referred <strong>to</strong> as depletion8670 Amortization <strong>of</strong> tangible assetsamortization <strong>of</strong> leasehold improvements and amountsreferred <strong>to</strong> as depreciation8690 Insurancebonding, fire insurance, liability insurance, premiumexpenses, property insurance, and vehicle insurance8691 Life insurance on executivesinsurance policies where <strong>the</strong> beneficiary is <strong>the</strong>corporation ra<strong>the</strong>r than <strong>the</strong> estate <strong>of</strong> <strong>the</strong> executive8710 Interest and bank chargesfinance charges, bank charges, and interest payments oncapital leases8711 Interest on short-term debt8712 Interest on bonds and debenturesamortization <strong>of</strong> bond discounts8713 Interest on mortgagesamortization <strong>of</strong> mortgage discount or expense8714 Interest on long-term debt8715 Bank charges8716 Credit card chargesinterest on credit cards8717 Collection and credit costs8740 Interest paid (financial institutions)8741 Interest paid on deposits8742 Interest paid on bonds and debentures8760 Business taxes, licences, and membershipsbeverage licences, business charges, mo<strong>to</strong>r vehiclelicences and/or registration permits, and trade licences8761 Membershipsdues and subscriptions8762 Business taxesbusiness tax, provincial capital tax (excludingNova Scotia and <strong>New</strong> Brunswick taxes on largecorporations), bridge <strong>to</strong>lls, gross receipt tax, health andeducation tax, hospital tax, permits, road <strong>to</strong>lls, and taxeson leases8763 Franchise fees8764 Government fees20www.cra.gc.ca

8780 <strong>New</strong> Brunswick tax on large corporations8790 Nova Scotia tax on large corporations8810 Office expenses8811 Office stationery and supplies8812 Office utilitiesutility expenses related <strong>to</strong> an <strong>of</strong>fice such as electricity,gas, heating, hydro, and telephone8813 Data processingword processing8860 Pr<strong>of</strong>essional feesengineering fees, pr<strong>of</strong>essional services, and surveyor fees8861 Legal feeslawyer and notary fees8862 Accounting feesbookkeeping8863 Consulting fees8864 Architect feesarchitectural design and illustration fees and landscapearchitect fees8865 Appraisal feesreal estate and jewellery appraisal, and financialvaluation services8866 Labora<strong>to</strong>ry fees8867 Medical fees8868 Veterinary feesbreeding fees8869 Brokerage fees8870 Transfer feesland and property transfer fees8871 Management and administration fees8872 Refining and assay8873 Registrar and transfer agent fees8874 Restructuring costsreorganization costs8875 Security commission fees8876 Training expenseanimal training, management training, and staffdevelopment8877 Studio and recording8910 Rentalrental expenses for arena, boat/vessel/ship, coal andlumberyards, railway sidings, safety deposit box/vaults,and parking charges8911 Real estate rentalapartment, building, land, and <strong>of</strong>fice rentals8912 Occupancy costs8913 Condominium fees8914 Equipment rentalrental expenses for computer equipment, film, <strong>of</strong>ficemachines, and road and construction equipment8915 Mo<strong>to</strong>r vehicle rentals8916 Moorage (boat)dock and wharf space8917 S<strong>to</strong>ragerental expense for garages and warehouses8918 Quota rentalforestry and logging quota rental expenses8960 Repairs and maintenanceaircraft repairs and maintenance8961 Repairs and maintenance – buildingspremises upkeep8962 Repairs and maintenance – vehicles8963 Repairs and maintenance – boats8964 Repairs and maintenance – machinery andequipmentgas and power line repairs and maintenance9010 O<strong>the</strong>r repairs and maintenancejani<strong>to</strong>rial services, landscaping, and yard maintenance9011 Machine shop expense9012 Road costssnow removal costs9013 Securityalarm system and surveillance equipment repairs andmaintenance9014 Garbage removal9060 Salaries and wagesamounts not found in cost <strong>of</strong> sales such asadministrative salaries, casual labour, cost <strong>of</strong> livingallowance, down time, fees <strong>to</strong> employees, minimumwage levies, payroll remuneration, severance pay,supervision, and vacation pay9061 Commissions9062 Crew share9063 Bonusesincentive compensation9064 Direc<strong>to</strong>rs fees9065 Management salaries<strong>of</strong>ficers’ salaries9066 Employee salaries<strong>of</strong>fice salaries9110 Sub-contractscontract labour, contract work, cus<strong>to</strong>m work, and hiredlabour9130 Suppliesmedical supplies, veterinary drugs and supplies,wrapping and packing supplies9131 Small <strong>to</strong>ols9132 Shop expense9133 Uniforms9134 Laundrydry-cleaning9135 Food and catering9136 Fishing gear9137 Nets and traps9138 Salt, bait, and ice9139 Camp supplies9150 Computer-related expenses9151 Upgradeupdates <strong>to</strong> computer s<strong>of</strong>tware9152 Internet9180 Property taxesmunicipal and realty taxes9200 Travel expensesairfare, hotel rooms, travel allowance, travel, andaccommodationswww.cra.gc.ca 21

9711 Feed, supplements, straw, and beddingpurchased dairy rations and forage9712 Lives<strong>to</strong>ck purchases9713 Veterinary fees, medicine, and breeding feesartificial insemination, disease testing, embryotransplants, neutering, semen, spaying, and studservice9714 Minerals and salts9760 Machinery expenses9761 Machinery insurance9762 Machinery licences9763 Machinery repairs9764 Machinery fuellubricants9765 Machinery lease9790 <strong>General</strong> farm expensesmilk testing, negative farm support payments, andsilage preservation9791 Amortization <strong>of</strong> tangible assetsamortization <strong>of</strong> leasehold improvements and amountsreferred <strong>to</strong> as depreciation9792 Advertising, marketing costs, and promotion9793 Bad debtallowance for bad debts, allowance/provision fordoubtful accounts, bad debt, bad debt written-<strong>of</strong>f,provision for bad debts, and reserve for bad debt9794 Benefits related <strong>to</strong> employee salariescontributions <strong>to</strong> deferred income plans(DPSP/EPSP/RPP), employer’s portion <strong>of</strong> employeebenefits (CPP/EI/QPIP/WCB), group insurance benefits(dental/life/medical plans), payroll deductions, andlodging/room and board9795 Building repairs and maintenance9796 Clearing, levelling, and draining landexpenses from building a road, digging/drilling a waterwell, installing land drainage, ploughing land, andbringing public utilities <strong>to</strong> <strong>the</strong> farm9797 Crop insurance, Revenue Protection Program, andstabilization premiums9798 Cus<strong>to</strong>m or contract workegg cleaning/grading/sorting/spraying, cheese aging,and contract harvesting/combining/crop dusting9799 Electricity9800 Fence repairs and maintenance9801 Freight and truckingdelivery and distribution costs and shipping9802 Heating fuel and curing fuelcoal, oil, natural gas, and fuel for curing <strong>to</strong>bacco/cropdrying/greenhouses9803 Insurance program overpayment recapture9804 O<strong>the</strong>r insurance premiumsfarm insurance, private crop insurance, lives<strong>to</strong>ckinsurance, and business interruption insurancepremiums9805 Interest and bank chargesfinance charges, interest on a farm loan, interest onlong-term debt, and interest on a mortgage9806 Marketing board fees9807 Memberships/subscription feesassociation fees9808 Office expensesfarm-related <strong>of</strong>fice expenses such as accounting/receiptbooks, invoices, and stationery9809 Pr<strong>of</strong>essional feesamounts reported as farm-related expenses such asaccounting/bookkeeping fees, data processing costs, andlegal fees9810 Property taxesland, municipal, and realty taxes9811 Rent – land and buildings9812 Rent – machinery9813 O<strong>the</strong>r rental expenses9814 Salaries and wages9815 Salaries and wages o<strong>the</strong>r than spouse ordependantssalaries for farmhand and self9816 Salaries and wages paid <strong>to</strong> dependants9817 Selling costs9818 Supplies9819 Mo<strong>to</strong>r vehicle expensesau<strong>to</strong>mobile expenses, gas, mo<strong>to</strong>r vehicle fuel, propane,tires, vehicle repairs and maintenance, and vehiclewashing9820 Small <strong>to</strong>ols9821 Soil testing9822 S<strong>to</strong>rage/drying9823 Licences/permits9824 Telephone9825 Quota rental (<strong>to</strong>bacco, dairy)9826 Gravel9827 Purchases <strong>of</strong> commodities resold9828 Salaries and wages paid <strong>to</strong> spouse9829 Mo<strong>to</strong>r vehicle interest and leasing costs9830 Prepared feed9831 Cus<strong>to</strong>m feed9832 Amortization <strong>of</strong> intangible assets9833 Amortization <strong>of</strong> milk quota9834 Travel expenses9835 Capital/business taxes9836 Commissions and levies9850 Non-farming expensesif you are not using items 8300 <strong>to</strong> 9368, use this item <strong>to</strong>report any non-farming expenses <strong>of</strong> a farmingcorporation9870 Net inven<strong>to</strong>ry adjustmentmay be used <strong>to</strong> report <strong>the</strong> farm’s opening inven<strong>to</strong>ry lessclosing inven<strong>to</strong>ryNoteIf <strong>the</strong> closing inven<strong>to</strong>ry is greater than <strong>the</strong> openinginven<strong>to</strong>ry, this item should be reported as a negative.9898 Total farm expensesrepresents <strong>the</strong> sum <strong>of</strong> all farm expense amountsincluding any amount in item 9850 and must bereported if <strong>the</strong>re are no amounts in any <strong>of</strong> items 8300 <strong>to</strong>9368 (see “Validity check items” on page 5)24www.cra.gc.ca

ExampleMultiple lines <strong>of</strong> business – Part 1Main Income StatementRevenueSales 1,500,000O<strong>the</strong>r revenue 1,500Foreign exchange 4,200Investment 5,630Buy it Here (net) 152,850Rent-a-Thing (net) 311,6301,975,810Cost <strong>of</strong> sales 725,0001,250,810ExpensesAdvertising 2,000CPP 7,100Depreciation 128,000Insurance 30,000Interest on mortgages 140,900Bank charges 12,700Capital taxes 6,600Office 5,800Legal fees 5,900Consulting 4,100Management fees 2,600Parking 230Repairs and maintenance 44,000Jani<strong>to</strong>rial services 3,000Salaries and wages 282,000Supplies 14,500Property taxes 42,000Telephone 4,500Utilities 54,000Au<strong>to</strong>mobile expenses 11,700Miscellaneous expenses 30,100831,730Supplementary statement – Buy It HereRevenueSales 275,000Cost <strong>of</strong> sales 95,500Gross pr<strong>of</strong>it 179,500Operating expensesAdvertising 750Medical plan 400CPP 1,200Repairs and maintenance 300Salaries and wages 21,000Supplies 1,800Utilities 1,20026,650Net income 152,850Supplementary Statement – Rent-a-ThingRevenueEquipment rental 350,000ExpensesMedical plan 570CPP 1,500Repairs and maintenance 800Salaries and wages 30,000Supplies 5,50038,370Net income 311,630Net income before taxes 419,080Unrealized gain (loss) 51,930Income taxes 9,000Net income after taxes 462,010www.cra.gc.ca 27

Part 21001 Operating Name: Manufacture-it-now0002 Description <strong>of</strong> <strong>the</strong> operation: manufacturing0003 Sequence number: 01RevenueAmount8000 Trade sales <strong>of</strong> goods and services 15000008230 O<strong>the</strong>r revenue 15008231 Foreign exchange gains/losses 42008090 Investment revenue 56308299 Total revenue 15113308518 Cost <strong>of</strong> sales 7250008519* Gross pr<strong>of</strong>it/loss 775000Operating expenses8521 Advertising 20008622 Employer’s portion <strong>of</strong> employee benefits 71008670 Amortization <strong>of</strong> tangible assets 1280008690 Insurance 300008713 Interest on mortgages 1409008715 Bank charges 127008762 Business taxes 66008810 Office expenses 58008861 Legal fees 59008863 Consulting fees 41008871 Management and administration fees 26008910 Rental 2308960 Repairs and maintenance 440009010 O<strong>the</strong>r repairs and maintenance 30009060 Salaries and wages 2820009130 Supplies 145009180 Property taxes 420009225 Telephone and telecommunications 45009220 Utilities 540009281 Vehicle expenses 117009270 O<strong>the</strong>r expenses 301009367 Total operating expenses 8317309368** Total expenses 15567309369*** Net non-farming income (45400)9970 Net income/loss before taxes andextraordinary items (45400)* 8519 = 8000 – 8518** 9368 = 8518 + 9367*** 9369 = 8299 – 93680001 Operating Name: Buy-it-here0002 Description <strong>of</strong> <strong>the</strong> operation: retail0003 Sequence number: 02Revenue Amount8000 Trade sales <strong>of</strong> goods and services 2750008299 Total revenue 2750008518 Cost <strong>of</strong> sales 955008519* Gross pr<strong>of</strong>it/loss 179500Operating expenses8521 Advertising 7508621 Group insurance benefits 4008622 Employer’s portion <strong>of</strong> employee benefits 12008960 Repairs and maintenance 3009060 Salaries and wages 210009130 Supplies 18009220 Utilities 12009367 Total operating expenses 266509368** Total expenses 1221509369*** Net non-farming income 1528509970 Net income/loss before taxes andextraordinary items 152850* 8519 = 8000 – 8518** 9368 = 8518 + 9367*** 9369 = 8299 – 93680001 Operating Name: Rent-a-thing0002 Description <strong>of</strong> <strong>the</strong> operation: equipment rental0003 Sequence number: 03RevenueAmount8140 Rental revenue 3500008299 Total revenue 350000Operating expenses8621 Group insurance benefits 5708622 Employer’s portion <strong>of</strong> employee benefits 15008960 Repairs and maintenance 8009060 Salaries and wages 300009130 Supplies 55009367 Total operating expenses 383709368 Total expenses 383709369* Net non-farming income 3116309970 Net income/loss before taxes andextraordinary items 311630* 9369 = 8299 – 9368Summary StatementRevenue Amount9970 Net income/loss before taxes and419080extraordinary items – all operations9980 Unrealized gains/losses 519309990 Current income taxes 90009999* Net income/loss after taxes andextraordinary items 462010* 9999 = 9970 + 9980 – 999028www.cra.gc.ca

Appendix C – Non-Pr<strong>of</strong>it OrganizationsThis Appendix is intended <strong>to</strong> help corporations that are non-pr<strong>of</strong>it organizations (NPOs) <strong>to</strong> use <strong>the</strong> GIFI <strong>to</strong> report <strong>the</strong>irfinancial statement information.Table A shows some NPO terminology and <strong>the</strong> equivalent GIFI terminology. Table B provides specific NPO terms and <strong>the</strong>suggested equivalent GIFI item.Table ANPO terminologyMembers’ equityOwners’ equityFund balancesNet assetsReservesBalance at end <strong>of</strong> year – <strong>General</strong> SurplusOperating fund<strong>General</strong> fundStatement <strong>of</strong> revenue and expendituresStatement <strong>of</strong> income and surplusStatement <strong>of</strong> receipts and disbursementsStatement <strong>of</strong> operationsExcess <strong>of</strong> revenues over expenses(expenses over revenues)Equivalent GIFI terminologyShareholder equityRetained earningsIncome statementNet non-farming incomeTable BNPO termEquivalent GIFI itemAssets and liabilitiesCash 1001 CashAmounts receivable from o<strong>the</strong>r than members 1060 Accounts receivableAmounts receivable from members 1073 Amounts receivable from members <strong>of</strong> NPOsInven<strong>to</strong>ry 1120 Inven<strong>to</strong>riesShort-term investments 1180 Short-term investmentsPrepaid expenses 1484 Prepaid expensesFixed assets 2008 Total tangible capital assetsLong-term investments 2300 Long-term investmentsTotal assets 2599 Total assetsAmounts owing <strong>to</strong> o<strong>the</strong>r than members 2620 Amounts payable and accrued liabilitiesAmounts owing <strong>to</strong> members 2630 Amounts payable <strong>to</strong> members <strong>of</strong> NPOsTotal liabilities 3499 Total liabilitiesAmounts receivedInterest received 8090 Investment revenueDividends received 8095 Dividend incomeRentals received 8140 Rental revenueProceeds <strong>of</strong> disposition <strong>of</strong> capital property 8210 Realized gains/losses on disposal <strong>of</strong> assetsMembership dues or fees 8221 Membership feesAssessments received 8222 AssessmentsGifts 8223 GiftsGross sales and revenues from organizational activities 8224 Gross sales and revenues from organizational activitiesRoyalties received 8237 Royalty income o<strong>the</strong>r than resourceFederal, provincial, or municipal grants received 8242 Subsidies and grantsTotal receipts 8299 Total revenueTransfer(s) <strong>to</strong>/from fund(s)Shown in retained earnings 3745 Interfund transferShown on income statement 9286 Interfund transferwww.cra.gc.ca 29