Chapter 5: Matrix Approaches to Simple Linear Regression

Chapter 5: Matrix Approaches to Simple Linear Regression

Chapter 5: Matrix Approaches to Simple Linear Regression

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

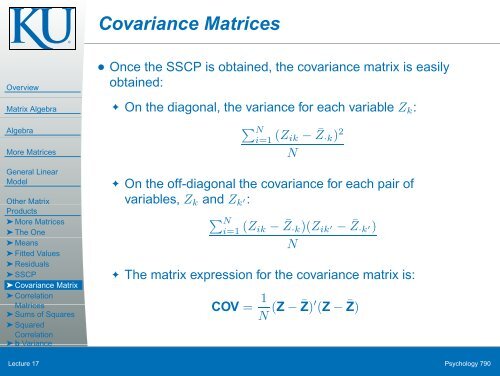

Covariance MatricesOverview<strong>Matrix</strong> AlgebraAlgebraMore MatricesGeneral <strong>Linear</strong>ModelOther <strong>Matrix</strong>Products➤ More Matrices➤ The One➤ Means➤ Fitted Values➤ Residuals➤ SSCP➤ Covariance <strong>Matrix</strong>➤ CorrelationMatrices➤ Sums of Squares➤ SquaredCorrelation➤ b Variance● Once the SSCP is obtained, the covariance matrix is easilyobtained:✦ On the diagonal, the variance for each variable Z k :∑ Ni=1 (Z ik − ¯Z·k ) 2✦ On the off-diagonal the covariance for each pair ofvariables, Z k and Z k ′:∑ Ni=1 (Z ik − ¯Z·k )(Z ik′ − ¯Z·k ′)✦ The matrix expression for the covariance matrix is:NNCOV = 1 N (Z − ¯Z) ′ (Z − ¯Z)Wrapping Lecture 17 UpPsychology 790