Chapter 5: Matrix Approaches to Simple Linear Regression

Chapter 5: Matrix Approaches to Simple Linear Regression

Chapter 5: Matrix Approaches to Simple Linear Regression

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

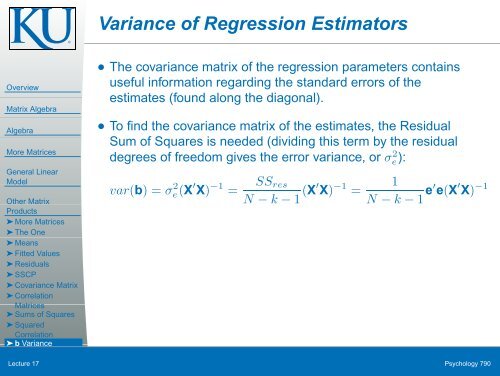

Variance of <strong>Regression</strong> Estima<strong>to</strong>rsOverview<strong>Matrix</strong> AlgebraAlgebraMore MatricesGeneral <strong>Linear</strong>ModelOther <strong>Matrix</strong>Products➤ More Matrices➤ The One➤ Means➤ Fitted Values➤ Residuals➤ SSCP➤ Covariance <strong>Matrix</strong>➤ CorrelationMatrices➤ Sums of Squares➤ SquaredCorrelation➤ b Variance● The covariance matrix of the regression parameters containsuseful information regarding the standard errors of theestimates (found along the diagonal).● To find the covariance matrix of the estimates, the ResidualSum of Squares is needed (dividing this term by the residualdegrees of freedom gives the error variance, or σ 2 e):var(b) = σ 2 e(X ′ X) −1 =SS resN − k − 1 (X′ X) −1 =1N − k − 1 e′ e(X ′ X) −1Wrapping Lecture 17 UpPsychology 790