44Notes to the Financial <strong>Statement</strong>sP Accounting Reserves and Long Term LiabilityAccounting ReservesFixed AssetRestatementAccount£’000CapitalFinancingAccount£’000Long TermLiabilityTotalGovernmentGrantDeferredAccount£’000 £’000Balance as at 01.04.<strong>2006</strong> (1,405,491) (75,280) (60,089) (1,540,860)Minimum Revenue Provision Adjustment 0 (12,129) 0 (12,129)Transfers during year 0 (43,820) 43,820 0Revaluation <strong>of</strong> Fixed Assets (23,853) 0 0 (23,853)Financing <strong>of</strong> Fixed Assets 0 (12,831) (76,190) (89,021)Depreciation 0 96,846 0 96,846RCCO 0 (15,965) 0 (15,965)Capital expenditure adjustment 11,954 309 0 12,263Cost <strong>of</strong> assets disposed 36,593 0 0 36,593Balance as at 31.03.20<strong>07</strong> (1,380,797) (62,870) (92,459) (1,536,126)Accounting ReservesFixed Asset Restatement AccountThe Fixed Asset Restatement Account is debited orcredited with the deficits or surpluses that arise onthe revaluation <strong>of</strong> fixed assets as well as being writtendown by the net book value <strong>of</strong> assets when they aredisposed <strong>of</strong>. The account cannot be used to supportspending.Capital Financing AccountThe Capital Finance Account contains the amount<strong>of</strong> capital expenditure that has been financedfrom revenue and capital receipts excluding sumsreceived in respect <strong>of</strong> loans negotiated to financecapital investment. The account also contains thedifference between the minimum revenue provisionand depreciation. Additionally, it handles the release<strong>of</strong> government grants from the Government GrantsDeferred Account as funds are applied for financingpurposes. The account cannot be used to supportspending.Balance as at 1 Aprilpercentage change over previous yearLong Term LiabilityGovernment Grant Deferred AccountGovernment grants are received and applied to financecapital expenditure on fixed assets. Such grants areusually non-specific to particular capital schemes andcannot be written <strong>of</strong>f through the Asset ManagementRevenue Account to match depreciation. Instead,they are written <strong>of</strong>f to the Capital Financing Accountin the year <strong>of</strong> application. Where grants are specificthe grant is released to the Capital Financing Accountas the book value <strong>of</strong> purchased fixed assets isdepleted.SORP <strong>2006</strong> requires the Government Grant DeferredAccount to be shown as a Long Term Liability.Q Police Officer Pension ReservePolice Officer Pension Reserve<strong>2006</strong>-<strong>07</strong>£’00014,743,98717.98%2005-06£’00012,496,48833.28%2004-05£’0009,375,9736.37%2003-04£’0008,814,650Actuarial gainpercentage change over previous year(1,095,714)(177.59)%1,412,100(43)%2,461,50218588.80%13,171Revenue Reserve movementpercentage change over previous year926,12710.86%835,39926.77%659,01320.22%548,152Balance as at 31 Marchpercentage change over previous year14,574,400(1.15)%14,743,98717.99%12,496,48833.28%9,375,973

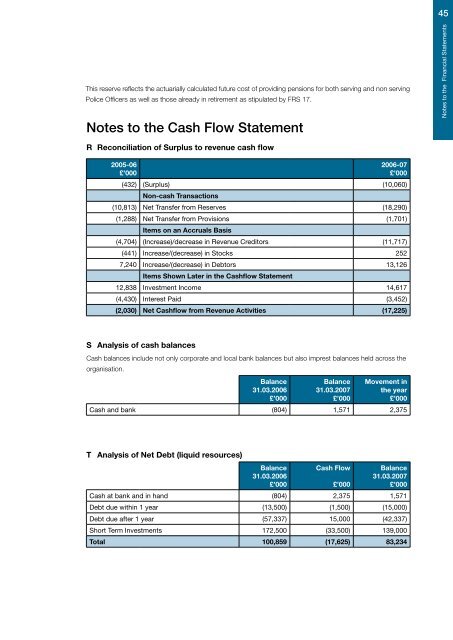

45This reserve reflects the actuarially calculated future cost <strong>of</strong> providing pensions for both serving and non servingPolice Officers as well as those already in retirement as stipulated by FRS 17.Notes to the Cash Flow <strong>Statement</strong>Notes to the Financial <strong>Statement</strong>sR Reconciliation <strong>of</strong> Surplus to revenue cash flow2005-06£’000<strong>2006</strong>-<strong>07</strong>£’000(432) (Surplus) (10,060)Non-cash Transactions(10,813) Net Transfer from Reserves (18,290)(1,288) Net Transfer from Provisions (1,701)Items on an Accruals Basis(4,704) (Increase)/decrease in Revenue Creditors (11,717)(441) Increase/(decrease) in Stocks 2527,240 Increase/(decrease) in Debtors 13,126Items Shown Later in the Cashflow <strong>Statement</strong>12,838 Investment Income 14,617(4,430) Interest Paid (3,452)(2,030) Net Cashflow from Revenue Activities (17,225)S Analysis <strong>of</strong> cash balancesCash balances include not only corporate and local bank balances but also imprest balances held across theorganisation.Balance31.03.<strong>2006</strong>£’000Balance31.03.20<strong>07</strong>£’000Movement inthe year£’000Cash and bank (804) 1,571 2,375T Analysis <strong>of</strong> Net Debt (liquid resources)Balance31.03.<strong>2006</strong>£’000Cash Flow£’000Balance31.03.20<strong>07</strong>£’000Cash at bank and in hand (804) 2,375 1,571Debt due within 1 year (13,500) (1,500) (15,000)Debt due after 1 year (57,337) 15,000 (42,337)Short Term Investments 172,500 (33,500) 139,000Total 100,859 (17,625) 83,234

![Appendix 1 [PDF]](https://img.yumpu.com/51078997/1/184x260/appendix-1-pdf.jpg?quality=85)

![Transcript of this meeting [PDF]](https://img.yumpu.com/50087310/1/184x260/transcript-of-this-meeting-pdf.jpg?quality=85)

![Street drinking in Hounslow [PDF]](https://img.yumpu.com/49411456/1/184x260/street-drinking-in-hounslow-pdf.jpg?quality=85)