6In the longer run<strong>Angola</strong>’s known oil and gas reserves are relativelymodest, being far smaller than those of Nigeria orSaudi Arabia. Its oil output is projected to peak in2010. Between 2015 and 2018, <strong>Angola</strong>’s petrodollarbasednational budget could flip from surplus to deficitif no alternative sources of state revenue are found.The hydrocarbon sector currently absorbs aroundthree-quarters of all investment but generates only afraction of one percent of all new employment. Bycontrast, the agricultural sector absorbs less than onepercent of recorded new investment 18 but couldgenerate massive new employment.Should <strong>Angola</strong> persist in its current pattern of elitecentredconsumption and hydrocarbon-centredproduction, it will probably face a serious downturn byaround 2020. 19 The revenue shock triggered in 2008by falling oil and diamond prices (accompanied in alllikelihood by accelerated capital flight) provides aforetaste of what may lie ahead. The next decade couldsee an abrupt end to rising expectations among urbanstrata who aspire to stable middle class lifestyles. Thecurrent development model is thus a ticking politicaltime bomb. The coming decade will reveal whether thatbomb will be defused or not.Other extractive industries andlandDiamonds have linked <strong>Angola</strong> to world systems sincethe early 1900s, but with impacts rather different fromthose of the oil sector. Many diamond-digging firms areactive, most employing private or irregular armedforces. In principle a state monopoly managed underformal sector rules, alluvial diamond mining alsoinvolves informal trade and labour circuits. As of2000, an estimated 300 to 350 thousand artisanal18 BPI 2007, Estudos Económicos e Financeiros – <strong>Angola</strong>,Departamento de Estudos Económicos e Financeiros, Outubro, Lisboa:BPI19 Mitchell, J. and P. Stevens 2008, Ending Dependence. HardChoices for Oil-Exporting States, London: Chatham House (the RoyalInstitute of International Affairs)diamond miners or garimpeiros were thought to beactive; <strong>yet</strong> even after a brutal government-ledcampaign to suppress them, there were in 2007 at leastas many if not more garimpeiros. 20All these elements pose political and fiscal challengesboth to central authority and to internationalmonitoring. Diamond-trafficking paid Unita’s billsduring its last nine years of war. In 1994, an abortivepeace settlement allocated control over five diamondareas to Unita; in 2002 this elite bargain was renewed,this time with success. Separatist movements in themain diamond zones of Lunda North and Lunda Southhave emerged, but have been held in check throughagreements among political and military elites abouteach one’s shares of diamond revenues. Transparencyhas been even weaker than in the hydrocarbon sector,although UN and civil society pressures have broughtformal diamond trading circuits under a permanentpublic spotlight. These get attention because theyinvolve major international players, such as the DeBeers monopoly.Other extractive industries such as iron ore, granite andmarble are far less lucrative, but control over them islikewise subject to limited access in the service ofinternationalised elite bargains. The same logic holdsfor access to land. Upward pressures on global foodprices strengthen incentives for foreign corporationssuch as Lonhro to acquire land suitable for farming orranching, either for direct use or for speculation.Chinese investors are also among those showing activeinterest in <strong>Angola</strong>n farmlands. A land law enacted in2004 protects small farmers only marginally, 21 insteadfavouring corporate interests. Such trends castshadows on the prospects for decent rural livelihoodsand an equitable distribution of income and wealth; onthe contrary, they set the scene for further socioeconomicpolarisation and conflict.20 PAC 2007, Diamond Industry Annual Review for <strong>Angola</strong> 2007,Ottawa: Partnership Africa-Canada21 Discussed in ‘A Questão da Terra em <strong>Angola</strong>. Ontem e Hoje’ F.Pacheco (coord.), Caderno de Estudos Sociais No. 1, 2005, Luanda:Centro de Estudos Sociais e Desenvolvimento; and ARD, Inc. 2007,Strengthening Land Tenure and Property Rights in <strong>Angola</strong>. Land Lawand Policy: Overview of Legal Framework, Washington DC/BurlingtonVT: USAID/ARDWorking Paper 81

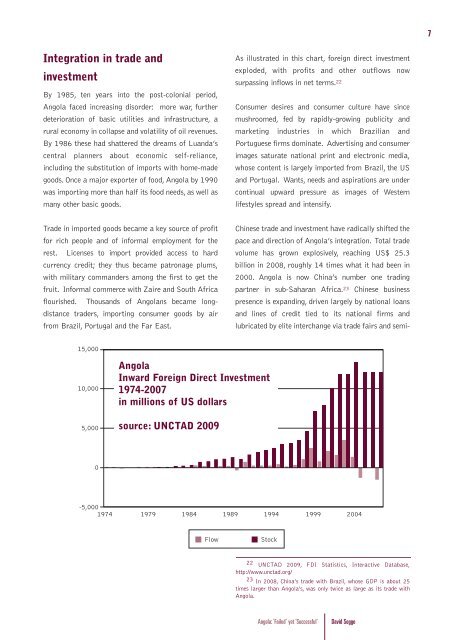

7Integration in trade andinvestmentBy 1985, ten years into the post-colonial period,<strong>Angola</strong> faced increasing disorder: more war, furtherdeterioration of basic utilities and infrastructure, arural economy in collapse and volatility of oil revenues.By 1986 these had shattered the dreams of Luanda’scentral planners about economic self-reliance,including the substitution of imports with home-madegoods. Once a major exporter of food, <strong>Angola</strong> by 1990was importing more than half its food needs, as well asmany other basic goods.As illustrated in this chart, foreign direct investmentexploded, with profits and other outflows nowsurpassing inflows in net terms. 22Consumer desires and consumer culture have sincemushroomed, fed by rapidly-growing publicity andmarketing industries in which Brazilian andPortuguese firms dominate. Advertising and consumerimages saturate national print and electronic media,whose content is largely imported from Brazil, the USand Portugal. Wants, needs and aspirations are undercontinual upward pressure as images of Westernlifestyles spread and intensify.Trade in imported goods became a key source of profitfor rich people and of informal employment for therest. Licenses to import provided access to hardcurrency credit; they thus became patronage plums,with military commanders among the first to get thefruit. Informal commerce with Zaire and South Africaflourished. Thousands of <strong>Angola</strong>ns became longdistancetraders, importing consumer goods by airfrom Brazil, Portugal and the Far East.Chinese trade and investment have radically shifted thepace and direction of <strong>Angola</strong>’s integration. Total tradevolume has grown explosively, reaching US$ 25.3billion in 2008, roughly 14 times what it had been in2000. <strong>Angola</strong> is now China’s number one tradingpartner in sub-Saharan Africa. 23 Chinese businesspresence is expanding, driven largely by national loansand lines of credit tied to its national firms andlubricated by elite interchange via trade fairs and semi-15,00010,000<strong>Angola</strong>Inward Foreign Direct Investment1974-2007in millions of US dollars5,000source: UNCTAD 20090-5,00019741979 1984 1989 1994 1999 2004FlowStock22 UNCTAD 2009, FDI Statistics, Interactive Database,http://www.unctad.org/23 In 2008, China’s trade with Brazil, whose GDP is about 25times larger than <strong>Angola</strong>’s, was only twice as large as its trade with<strong>Angola</strong>.<strong>Angola</strong>: ‘Failed’ <strong>yet</strong> ‘Successful’David Sogge