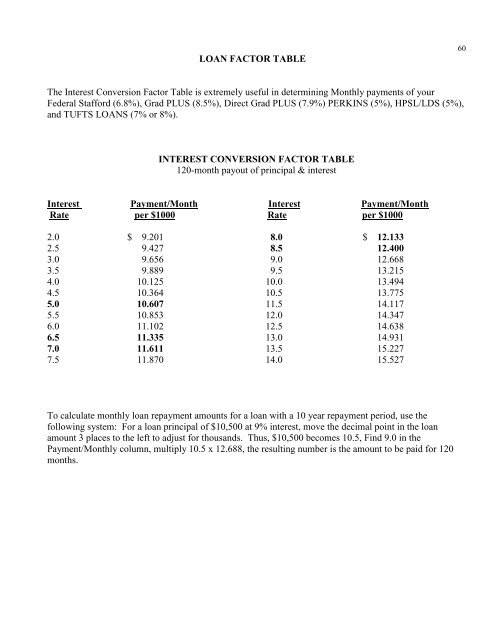

LOAN FACTOR TABLE60The Interest Conversion Factor Table is extremely useful in determining Monthly payments <strong>of</strong> yourFederal Stafford (6.8%), Grad PLUS (8.5%), Direct Grad PLUS (7.9%) PERKINS (5%), HPSL/LDS (5%),and TUFTS LOANS (7% or 8%).INTEREST CONVERSION FACTOR TABLE120-month payout <strong>of</strong> principal & interestInterest Payment/Month Interest Payment/MonthRate per $1000 Rate per $10002.0 $ 9.201 8.0 $ 12.1332.5 9.427 8.5 12.4003.0 9.656 9.0 12.6683.5 9.889 9.5 13.2154.0 10.125 10.0 13.4944.5 10.364 10.5 13.7755.0 10.607 11.5 14.1175.5 10.853 12.0 14.3476.0 11.102 12.5 14.6386.5 11.335 13.0 14.9317.0 11.611 13.5 15.2277.5 11.870 14.0 15.527To calculate monthly <strong>loan</strong> <strong>repayment</strong> amounts for a <strong>loan</strong> with a 10 year <strong>repayment</strong> period, use thefollowing system: For a <strong>loan</strong> principal <strong>of</strong> $10,500 at 9% interest, move the decimal point in the <strong>loan</strong>amount 3 places to the left to adjust for thousands. Thus, $10,500 becomes 10.5, Find 9.0 in thePayment/Monthly column, multiply 10.5 x 12.688, the resulting number is the amount to be paid for 120months.

ACCRUED INTEREST TABLE61The purpose <strong>of</strong> this chart is to help you estimate the amount <strong>of</strong> interest that would accrue on your <strong>loan</strong>every month so that you can estimate how much would be added to your <strong>loan</strong>’s principal if you and yourlender agree to capitalize interest.ApproximateMonthly Accrued InterestIf Interest Rate Is:Principal 6.0% 7.0% 8.0% 9.0% 10.0% 11.0%$ 500 $2.50 $2.92 $3.33 $3.75 $4.17 $4.581,000 5.00 5.83 6.67 7.50 8.33 9.171,500 7.50 8.75 10.00 11.25 12.50 13.752,000 10.00 11.67 13.33 15.00 16.67 18.332,500 12.50 14.58 16.67 18.75 20.83 22.923,000 15.00 17.50 20.00 22.50 25.00 27.503,500 17.50 20.42 23.33 26.25 29.17 32.084,000 20.00 23.33 26.67 30.00 33.33 36.674,500 22.50 26.25 30.00 33.75 37.50 41.255,000 25.00 29.17 33.33 37.50 41.67 45.835,500 27.50 32.08 36.67 41.25 45.83 50.426,000 30.00 35.00 40.00 45.00 50.00 55.006,500 32.50 37.92 43.33 48.75 54.17 59.587,000 35.00 40.83 46.67 52.50 58.33 64.177,500 37.50 43.75 50.00 56.25 62.50 68.75The advantage <strong>of</strong> capitalizing interest is that you would not be required to make interest payments duringany in-school, grace or deferment period. The disadvantage would be that you would pay more in interestcharges over the life <strong>of</strong> your <strong>loan</strong> because your interest charges will be added to your principal balance.Your monthly <strong>repayment</strong> amount will be higher if you choose to capitalize.For example, if you owe $500 in principal at an interest rate <strong>of</strong> 6.0 percent, then approximately $2.50 ininterest would accrue on your <strong>loan</strong> every month. If you and your lender agree to capitalization on aquarterly basis (every three months), approximately $7.50 would be added to your $500 principal balance.As a result, at the end <strong>of</strong> one quarter you would owe, and interest would accrue on, $507.50 in principal.Or, if you owe $4,000 in principal at an interest rate <strong>of</strong> 11.0 percent, then approximately $36.37 in interestwould accrue on your <strong>loan</strong> every month. If you and your lender had agreed to capitalize interest on aquarterly basis (every three months), approximately $110.01 would be added to your $4000 principalbalance. As a result, at the end <strong>of</strong> one quarter, you would owe, and interest would accrue on $4,110.01 inprincipal.Contact your lender if you have questions or need more information.