Identifying Speculative Bubbles with an Infinite Hidden Markov Model

Identifying Speculative Bubbles with an Infinite Hidden Markov Model

Identifying Speculative Bubbles with an Infinite Hidden Markov Model

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

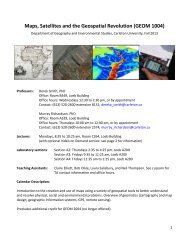

0 20 40 60 80 100(a) The non-bubble scenariotime0 20 40 60 80 100(b) The periodically collapsing explosivebehavior of Ev<strong>an</strong>s (1991)time0 20 40 60 80 100time0 20 40 60 80 100time(c) The locally explosive behavior of PWY(d) The hybrid bubble behaviorFigure 1: Illustration of different data generating processes of bubblesincorporates linear dynamic (Figure 1a), existing nonlinear dynamics (Figure 1a-1b), <strong>an</strong>d somemuch richer dynamic <strong>with</strong> multiple <strong>an</strong>d heterogeneous bubbles (Figure 1d). 4The second contribution is that we propose <strong>an</strong> easy <strong>an</strong>d coherent dating algorithm for bubblesby estimating the iHMM in the Bayesi<strong>an</strong> framework. One of the prevailing approachesfor date stamping bubbles 5 is the <strong>Markov</strong>-switching Augmented Dickey-Fuller (MSADF) testproposed by Hall et al. (1999, HPS hereafter). The MSADF test requires to assume or testfor state dimension before estimating the model. However, to the best of our knowledge, theperform<strong>an</strong>ce of testing procedures for the state dimension of a <strong>Markov</strong>-switching model which4 Phillips et al. (2011a) argues that multiples bubbles is a inherent feature of a long-sp<strong>an</strong> economic or fin<strong>an</strong>cialprice series.5 Another prevailing approach is the sup type unit root test of Phillips et al. (2011b) <strong>an</strong>d Phillips et al.(2011a).3