Activity Report 2015

Activity Report 2015 - Federal Audit Oversight Authority FAOA

Activity Report 2015 - Federal Audit Oversight Authority FAOA

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Financial Audit | FAOA <strong>2015</strong><br />

17<br />

If the entity has an internal audit function<br />

the auditor makes inquiries of<br />

appropriate internal audit staff and<br />

assesses the nature of internal audit’s<br />

responsibilities, how it fits into the<br />

entity’s organisational structure and<br />

its activities with respect to financial<br />

reporting (ISA 240.19, 315.6 letter a<br />

and 23). The auditor then has the following<br />

choices:<br />

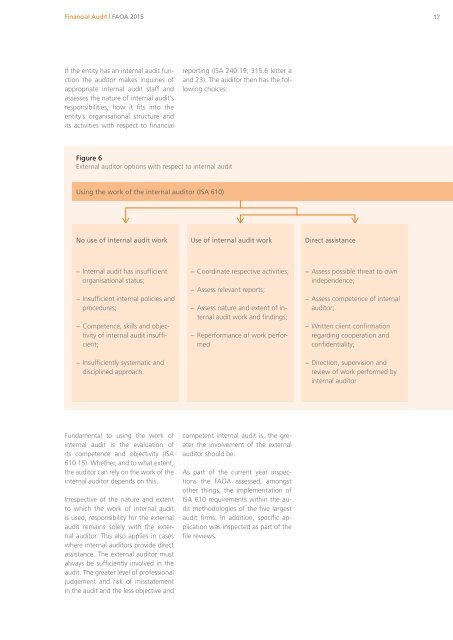

Figure 6<br />

External auditor options with respect to internal audit<br />

Using the work of the internal auditor (ISA 610)<br />

No use of internal audit work<br />

Use of internal audit work<br />

Direct assistance<br />

− Internal audit has insufficient<br />

organisational status;<br />

− Insufficient internal policies and<br />

procedures;<br />

− Competence, skills and objectivity<br />

of internal audit insufficient;<br />

− Insufficiently systematic and<br />

disciplined approach.<br />

− Coordinate respective activities;<br />

− Assess relevant reports;<br />

− Assess nature and extent of internal<br />

audit work and findings;<br />

− Reperformance of work performed<br />

− Assess possible threat to own<br />

independence;<br />

− Assess competence of internal<br />

auditor;<br />

− Written client confirmation<br />

regarding cooperation and<br />

confidentiality;<br />

− Direction, supervision and<br />

review of work performed by<br />

internal auditor<br />

Fundamental to using the work of<br />

internal audit is the evaluation of<br />

its competence and objectivity (ISA<br />

610.15). Whether, and to what extent,<br />

the auditor can rely on the work of the<br />

internal auditor depends on this.<br />

Irrespective of the nature and extent<br />

to which the work of internal audit<br />

is used, responsibility for the external<br />

audit remains solely with the external<br />

auditor. This also applies in cases<br />

where internal auditors provide direct<br />

assistance. The external auditor must<br />

always be sufficiently involved in the<br />

audit. The greater level of professional<br />

judgement and risk of misstatement<br />

in the audit and the less objective and<br />

competent internal audit is, the greater<br />

the involvement of the external<br />

auditor should be.<br />

As part of the current year inspections<br />

the FAOA assessed, amongst<br />

other things, the implementation of<br />

ISA 610 requirements within the audit<br />

methodologies of the five largest<br />

audit firms. In addition, specific application<br />

was inspected as part of the<br />

file reviews.