THE BEHAVIORAL ECONOMICS GUIDE 2016

BEGuide2016

BEGuide2016

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

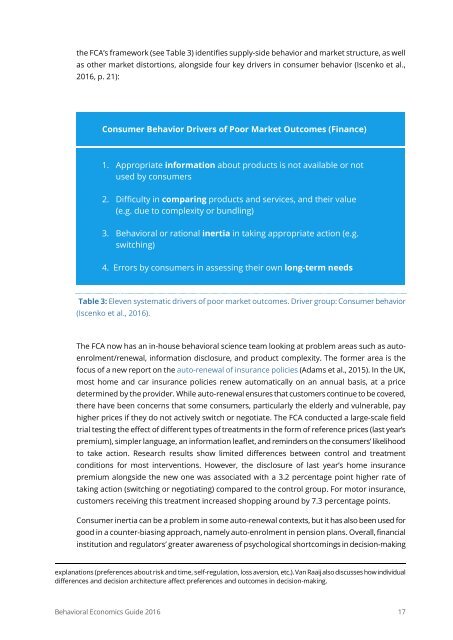

the FCA’s framework (see Table 3) identifies supply-side behavior and market structure, as well<br />

as other market distortions, alongside four key drivers in consumer behavior (Iscenko et al.,<br />

<strong>2016</strong>, p. 21):<br />

Consumer Behavior Drivers of Poor Market Outcomes (Finance)<br />

1. Appropriate information about products is not available or not<br />

used by consumers<br />

2. Difficulty in comparing products and services, and their value<br />

(e.g. due to complexity or bundling)<br />

3. Behavioral or rational inertia in taking appropriate action (e.g.<br />

switching)<br />

4. Errors by consumers in assessing their own long-term needs<br />

Table 3: Eleven systematic drivers of poor market outcomes. Driver group: Consumer behavior<br />

(Iscenko et al., <strong>2016</strong>).<br />

The FCA now has an in-house behavioral science team looking at problem areas such as autoenrolment/renewal,<br />

information disclosure, and product complexity. The former area is the<br />

focus of a new report on the auto-renewal of insurance policies (Adams et al., 2015). In the UK,<br />

most home and car insurance policies renew automatically on an annual basis, at a price<br />

determined by the provider. While auto-renewal ensures that customers continue to be covered,<br />

there have been concerns that some consumers, particularly the elderly and vulnerable, pay<br />

higher prices if they do not actively switch or negotiate. The FCA conducted a large-scale field<br />

trial testing the effect of different types of treatments in the form of reference prices (last year’s<br />

premium), simpler language, an information leaflet, and reminders on the consumers’ likelihood<br />

to take action. Research results show limited differences between control and treatment<br />

conditions for most interventions. However, the disclosure of last year’s home insurance<br />

premium alongside the new one was associated with a 3.2 percentage point higher rate of<br />

taking action (switching or negotiating) compared to the control group. For motor insurance,<br />

customers receiving this treatment increased shopping around by 7.3 percentage points.<br />

Consumer inertia can be a problem in some auto-renewal contexts, but it has also been used for<br />

good in a counter-biasing approach, namely auto-enrolment in pension plans. Overall, financial<br />

institution and regulators’ greater awareness of psychological shortcomings in decision-making<br />

explanations (preferences about risk and time, self-regulation, loss aversion, etc.). Van Raaij also discusses how individual<br />

differences and decision architecture affect preferences and outcomes in decision-making.<br />

Behavioral Economics Guide <strong>2016</strong> 17