Q4 2018 New Markets Investor

The magazine targets an audience of corporate and private investors, but its lucid voice makes it intelligible and essential reading for anybody who wants to understand investment strategies and markets in the 21st century.

The magazine targets an audience of corporate and private investors, but its lucid voice makes it intelligible and essential reading for anybody who wants to understand investment strategies and markets in the 21st century.

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Q3 2016<br />

‘The combination of cheap<br />

money and private IPOs has not<br />

only changed the way start-ups are<br />

being funded, but also insulating<br />

investors from reality.<br />

vulnerable to becoming mere features that other, larger<br />

platforms could easily incorporate into their offering.<br />

“This group of ‘Icarus’-class start-ups fly very close<br />

to the burning sun: simultaneously attracting platform<br />

company valuations while shouldering the huge<br />

business risk of becoming low-value add-on features<br />

during the next few years”, he said.<br />

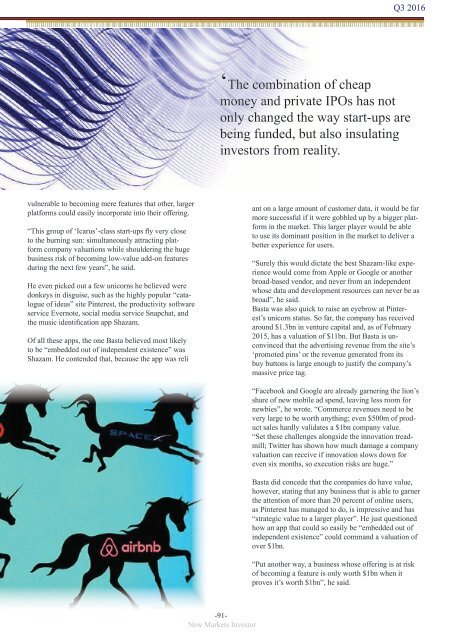

He even picked out a few unicorns he believed were<br />

donkeys in disguise, such as the highly popular “catalogue<br />

of ideas” site Pinterest, the productivity software<br />

service Evernote, social media service Snapchat, and<br />

the music identification app Shazam.<br />

Of all these apps, the one Basta believed most likely<br />

to be “embedded out of independent existence” was<br />

Shazam. He contended that, because the app was reli<br />

ant on a large amount of customer data, it would be far<br />

more successful if it were gobbled up by a bigger platform<br />

in the market. This larger player would be able<br />

to use its dominant position in the market to deliver a<br />

better experience for users.<br />

“Surely this would dictate the best Shazam-like experience<br />

would come from Apple or Google or another<br />

broad-based vendor, and never from an independent<br />

whose data and development resources can never be as<br />

broad”, he said.<br />

Basta was also quick to raise an eyebrow at Pinterest’s<br />

unicorn status. So far, the company has received<br />

around $1.3bn in venture capital and, as of February<br />

2015, has a valuation of $11bn. But Basta is unconvinced<br />

that the advertising revenue from the site’s<br />

‘promoted pins’ or the revenue generated from its<br />

buy buttons is large enough to justify the company’s<br />

massive price tag.<br />

“Facebook and Google are already garnering the lion’s<br />

share of new mobile ad spend, leaving less room for<br />

newbies”, he wrote. “Commerce revenues need to be<br />

very large to be worth anything; even $500m of product<br />

sales hardly validates a $1bn company value.<br />

“Set these challenges alongside the innovation treadmill;<br />

Twitter has shown how much damage a company<br />

valuation can receive if innovation slows down for<br />

even six months, so execution risks are huge.”<br />

Basta did concede that the companies do have value,<br />

however, stating that any business that is able to garner<br />

the attention of more than 20 percent of online users,<br />

as Pinterest has managed to do, is impressive and has<br />

“strategic value to a larger player”. He just questioned<br />

how an app that could so easily be “embedded out of<br />

independent existence” could command a valuation of<br />

over $1bn.<br />

“Put another way, a business whose offering is at risk<br />

of becoming a feature is only worth $1bn when it<br />

proves it’s worth $1bn”, he said.<br />

-91-<br />

<strong>New</strong> <strong>Markets</strong> <strong>Investor</strong>