09042018 - AS APC'S NEC MEETS TODAY: Oyegun, Tinubu's ‘soldiers’ head for showdown

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

32 — Vanguard, MONDAY, APRIL 9, 2018<br />

(08052201997)<br />

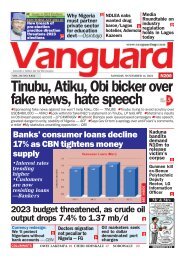

MPC and the blind leading the blind<br />

THE Central Bank’s<br />

Monetary Policy<br />

Committee, decided on<br />

Wednesday, April 4, 2018, to<br />

retain its Monetary Policy Rate<br />

(MPR) at 14 per cent, while<br />

mandatory Cash Reserve Ratio<br />

<strong>for</strong> banks, would remain at 22.5<br />

per cent. Disturbingly, however,<br />

there is no real hope that, such<br />

rates which have subsisted <strong>for</strong><br />

almost three years and inflicted<br />

so much social agony will now<br />

redeem the economy!<br />

Clearly, the prevailing 14 per<br />

cent inflation rate will make Naira<br />

income earners poorer this year,<br />

while, industries will struggle to<br />

survive, if they pay well over 20<br />

per cent to borrow. Similarly,<br />

government will be compelled to<br />

pay over 14 per cent to ironically<br />

borrow to service its risk free<br />

sovereign debts!<br />

The above title was first<br />

published on October 5, 2015,<br />

when MPR was 13 per cent, CRR<br />

25 per cent while inflation<br />

trended at 15.5 per cent; a<br />

summary of that article follows<br />

hereafter. Please read on.<br />

“The Monetary Policy<br />

Committee is the 'Think Tank' <strong>for</strong><br />

best practice strategies that<br />

should drive Nigeria's economic<br />

growth and prosperity. Thus, if<br />

the MPC's recommendations<br />

were appropriate, inclusive<br />

economic growth would evolve;<br />

conversely if MPC's diagnosis<br />

and prescriptions are wrong, then<br />

our current stunted growth<br />

experience, must inevitably be<br />

the product of Policies mid-wived<br />

by the MPC.<br />

Nonetheless, while the<br />

complimentary role of fiscal policy<br />

in a nation's economic growth is<br />

undeniable, best practice money<br />

supply management, can<br />

however redeem a grotesque<br />

fiscal plan; conversely, an<br />

"excellently structured" budget<br />

will grossly diminish in value if<br />

extant monetary strategies<br />

sustain rising inflation with,<br />

increasingly high cost of funds<br />

and an unstable Naira exchange<br />

rate determined by fiat!<br />

Consequently, a nation with a<br />

benevolent spread of latent<br />

wealth, with diverse agricultural<br />

and mineral resources, will<br />

remain poor if there is brazen<br />

indiscipline in managing its<br />

money supply; <strong>for</strong> example, if the<br />

authorities recklessly and<br />

liberally, continuously print or<br />

create money (values), inflation<br />

would hit the roof, and all income<br />

earners, will ultimately become<br />

traumatized and pauperized as<br />

the Naira’s purchasing power<br />

becomes steadily whittled down.<br />

Furthermore, subsisting high cost<br />

of loanable funds will also make<br />

sustainable real investments a<br />

challenge, and ultimately<br />

deepen our already suffocated job<br />

market to precipitate a wave of<br />

social insecurity! Consequently,<br />

the MPC’s role in promoting best<br />

practice management of money<br />

supply, is recognised to be<br />

pivotal <strong>for</strong> achieving enhanced<br />

social and economic welfare <strong>for</strong><br />

our people.<br />

Regrettably, however, <strong>for</strong> over<br />

two decades, the best ef<strong>for</strong>ts of<br />

MPC/CBN 'collaboration' have<br />

failed to successfully manage<br />

money supply and keep<br />

inflation, below best practice level<br />

of 2% to stabilize the value of all<br />

incomes; furthermore, subsisting<br />

monetary policy directions have<br />

also failed to bring down cost of<br />

borrowing, to supportive levels<br />

below 10%. It is clearly unrealistic<br />

and foolhardy to expect credible<br />

economic growth or indeed<br />

successful diversification, when<br />

cost of funds approaches 30% <strong>for</strong><br />

real sector domestic investors.<br />

Regrettably, however, it is<br />

inexplicable that despite<br />

Nigeria’s heavy unemployment<br />

burden, our MPC 'Think Tank'<br />

has, consistently endorsed<br />

inappropriately higher doubledigit<br />

Monetary Policy Rates,<br />

which in turn, compel banks to<br />

lend to customers, including the<br />

productive sector at clearly<br />

oppressive rates, well above 20%.<br />

Incidentally, when the MPC<br />

concluded its 103rd bimonthly<br />

meeting last week (21/9/2015), it<br />

retained its existing, anti-growth,<br />

13% benchmark <strong>for</strong> CBN<br />

advances to banks, while it<br />

slashed the cash ratio, which<br />

commercial banks must retain as<br />

The Monetary<br />

Policy Committee is<br />

the 'Think Tank' <strong>for</strong><br />

best practice<br />

strategies that<br />

should drive<br />

Nigeria's economic<br />

growth and<br />

prosperity<br />

reserves, from 31% to 25%. The<br />

overt interpretation of such<br />

monetary indices, is simply, that<br />

CBN appears impervious to the<br />

crying needs of the real sector <strong>for</strong><br />

access to cheaper funds;<br />

furthermore, the adoption of a<br />

cash reserve ratio which is as<br />

high as 25%, also suggest that<br />

the CBN clearly considers the<br />

prevailing level of money supply<br />

worrisome<br />

and<br />

counterproductive to price<br />

stability; consequently the apex<br />

bank’s intention is clearly to<br />

reduce both consumer spending<br />

and the capacity of banks to<br />

extend credit to their customers,<br />

despite the downside, that the<br />

high monetary policy<br />

benchmarks adopted <strong>for</strong> this<br />

purpose, would restrain<br />

investment and industrial<br />

capacity utilisation and<br />

significantly impede job creation<br />

in the economy.<br />

Thus, <strong>for</strong> these reasons, the<br />

MPC's regime of inflation and<br />

interest rates have historically<br />

been clearly out of tune <strong>for</strong> an<br />

economy with very low<br />

consumer demand, a shrinking<br />

industrial base, and an<br />

irrepressible and socially<br />

poisonous rate of<br />

unemployment.<br />

“The MPC's tight money policy<br />

is clearly traceable to the fear that<br />

a lower cash reserve<br />

requirement <strong>for</strong> banks will<br />

expand the economy’s already,<br />

dis-com<strong>for</strong>tingly bloated money<br />

supply to facilitate increased<br />

consumer spending, which could<br />

trigger inflation well beyond 10%<br />

to threaten price stability and the<br />

purchasing power of all Naira<br />

incomes”.<br />

“Instructively, the recent<br />

en<strong>for</strong>cement of the Treasury<br />

Single Account, reportedly, led<br />

to a 10% reduction in the size of<br />

perceived surplus Naira supply<br />

in the system. Regrettably, this<br />

reduction appears to be clearly<br />

insufficient to tame the Naira<br />

liquidity surplus which drives<br />

oppressive inflation rates, and<br />

instigate higher cost of borrowing<br />

with collateral threats to job<br />

creation, social prosperity and<br />

national security.”<br />

“The persistence of incurable<br />

systemic, surplus money supply,<br />

is clearly demonstrated by CBN's<br />

notice of the 4th September, 2015,<br />

that it removes some of the<br />

perceived excess money in the<br />

system to restrain inflation by<br />

borrowing over N800bn from the<br />

money market between<br />

September and December this<br />

year (2015). Incidentally, the<br />

banking subsector, primarily, will<br />

earn between 12-15% interest on<br />

these loans which CBN will,<br />

inexplicably, keep sterile or idle<br />

in order to reduce the inflationary<br />

pressures propelled by the threat<br />

of unbridled systemic money<br />

supply, chasing relatively few<br />

goods and services.”<br />

“Alarmingly, the CBN now<br />

makes annual interest payments<br />

of over N500bn to warehouse<br />

such ‘burdensome’ surplus cash<br />

it borrows and simply keeps idle<br />

in CBN vaults and records, while<br />

the real sector inexplicably suffers<br />

severe funding deprivations<br />

which invariably engender<br />

contraction in production and job<br />

opportunities. In this event, any<br />

sectoral cash intervention funds<br />

provided to stimulate economic<br />

activity and job creation, will<br />

inadvertently, ironically, further<br />

expand the subsisting bloated<br />

cash surplus in the system; so<br />

that, ultimately the additional<br />

liquidity injected will still be,<br />

indiscriminately subsequently<br />

mopped up also, once again, by<br />

CBN despite the attendant high<br />

interest rates that are clearly<br />

discordant with rates payable on<br />

sovereign risk free loans,<br />

particularly by a country with<br />

robust resource endowments<br />

such as Nigeria.”<br />

Worse still, it has been<br />

suggested that the latest<br />

reduction of cash reserve ratio<br />

from 31% to 25% would<br />

supplement/compound liquidity<br />

by over N300bn; invariably,<br />

reduction in CRR will<br />

inadvertently also increase the<br />

CBN’s portfolio <strong>for</strong> idle debts<br />

which nonetheless, tragically<br />

attract industrially<br />

counterproductive interest rates.<br />

Incredibly, inspite of these policy<br />

contradictions, a gullible media<br />

and a trusting but misguided<br />

public still believe that the MPC/<br />

CBN will lead our nation to<br />

Eldorado.”<br />

SAVE THE NAIRA, SAVE<br />

NIGERIANS<br />

FINANCIAL VANGUARD<br />

cess and are now telling the<br />

banks to adopt it. But it does not<br />

remove, by law the relationship,<br />

from the money moving<br />

perspective, it is still the banks. I<br />

don’t see it changing. I hear people<br />

talk about cryptocurrency, it<br />

will not play a significant part in<br />

the world <strong>for</strong> their local transactions.<br />

No government in the world<br />

will give up its ability to generate<br />

or create its own currency with<br />

third parties it does not know. So<br />

we will have cryptocurrency <strong>for</strong><br />

selected use the same way even<br />

today I can buy dollars when I<br />

want to send somebody to buy<br />

something <strong>for</strong> me in America. But<br />

<strong>for</strong> my day to day, it is Naira. The<br />

only way you have local cryptocurrency<br />

is if the central<br />

bank issues it itself. But not that<br />

anyone of those out there will<br />

come in.<br />

So will the banks be threatened<br />

by the Fintechs? Yes. I think<br />

there is even other business that<br />

is easier <strong>for</strong> the Fintechs to get<br />

involved in. Insurance, anything<br />

that requires a lot of technical<br />

use is actually easier.<br />

Even in some aspects of health,<br />

but the money bit of the business<br />

is banks, which is why<br />

they are focusing on banks. It<br />

is a collaboration that will happen.<br />

It is not one taking over<br />

from the other. The trend <strong>for</strong> e-<br />

payment transactions last year<br />

was that, yes there was still<br />

growth but the rate of growth<br />

slowed. What happened last<br />

year that slowed down the<br />

growth rate of e-payment transactions?<br />

Why the slow pace of<br />

growth?<br />

We also noticed slow pace of<br />

growth in BVN enrolment.<br />

Why is this so?<br />

Starting with transactions, if<br />

you look in absolute terms, the<br />

growth in 2017 was more than<br />

the growth in 2016. But the base<br />

had increased. So if you look<br />

in absolute terms there were a<br />

lot more transactions. It is because<br />

the base has been increasing<br />

over time so that is why<br />

we are seeing a slowdown in<br />

the build up. But there is a<br />

lot more transactions in 2017<br />

than in 2016. We think that will<br />

happen <strong>for</strong> a while. But are we<br />

going to back to such massive<br />

growth? Now that goes back to<br />

your question on the BVN; Almost<br />

all bank customers now<br />

have BVN. The number of account<br />

continues to grow but the<br />

numbers of individuals that<br />

have account are not going as<br />

fast.<br />

So unless we bring more people<br />

in you will find you and I will<br />

be doing more transaction but at<br />

some point, all my payments are<br />

electronic. So there is no more<br />

growth in electronic transactions.<br />

So now I am still doing some<br />

cash, but more and more we we<br />

ECONOMY<br />

No government will submit its currency to cryptocurrencies - Shonubi, NIBSS CEO<br />

Continued from page 30<br />

are doing cards, we are doing<br />

transfers. Soon those of us that<br />

have bank accounts will only be<br />

doing electronic payments. So,<br />

what next?<br />

Those who are outside the<br />

banking space will continue to<br />

do business even though with<br />

cash. So the focus has to do with,<br />

how do we increase the 33 million<br />

to 40-50 million? How do we<br />

bring people in, into the banking<br />

space and then we will begin<br />

to see the growth again pick<br />

up significantly and that is one<br />

of the aims this year from the<br />

CBN to the banking industry to<br />

focus on financial inclusion and<br />

getting more customers into the<br />

banking system.