Wills, Trusts & Estates

Wills, Trusts & Estates

Wills, Trusts & Estates

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

exemption. As of 2018, the federal estate tax exemption was $11,180,000. For a<br />

married couple, the combined exemption is $22,360,000.<br />

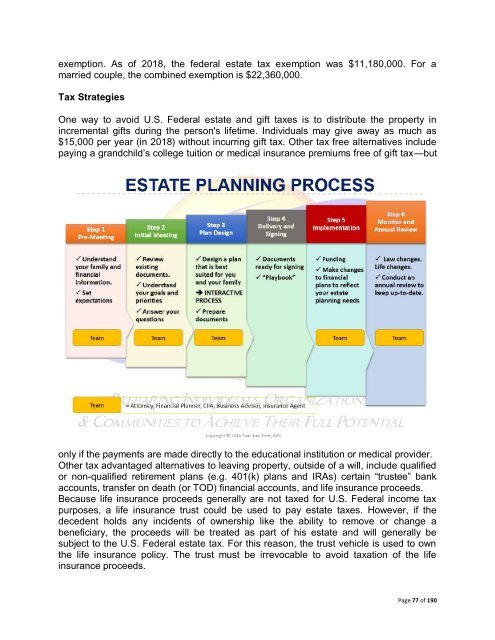

Tax Strategies<br />

One way to avoid U.S. Federal estate and gift taxes is to distribute the property in<br />

incremental gifts during the person's lifetime. Individuals may give away as much as<br />

$15,000 per year (in 2018) without incurring gift tax. Other tax free alternatives include<br />

paying a grandchild’s college tuition or medical insurance premiums free of gift tax—but<br />

only if the payments are made directly to the educational institution or medical provider.<br />

Other tax advantaged alternatives to leaving property, outside of a will, include qualified<br />

or non-qualified retirement plans (e.g. 401(k) plans and IRAs) certain “trustee” bank<br />

accounts, transfer on death (or TOD) financial accounts, and life insurance proceeds.<br />

Because life insurance proceeds generally are not taxed for U.S. Federal income tax<br />

purposes, a life insurance trust could be used to pay estate taxes. However, if the<br />

decedent holds any incidents of ownership like the ability to remove or change a<br />

beneficiary, the proceeds will be treated as part of his estate and will generally be<br />

subject to the U.S. Federal estate tax. For this reason, the trust vehicle is used to own<br />

the life insurance policy. The trust must be irrevocable to avoid taxation of the life<br />

insurance proceeds.<br />

Page 77 of 190