Relaunch Investment Suitability

Relaunch Investment Suitability

Relaunch Investment Suitability

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

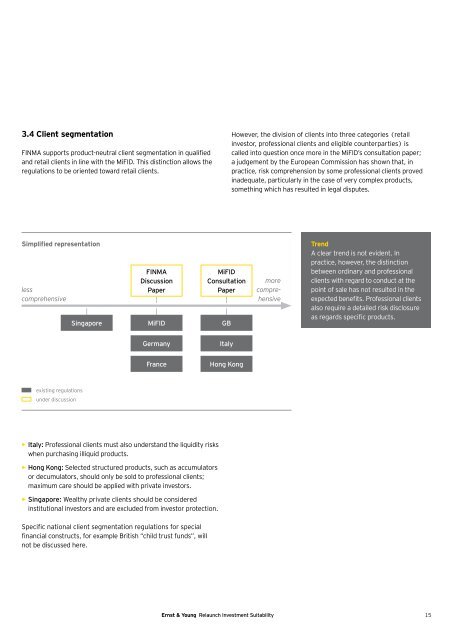

3.4 Client segmentation<br />

FINMA supports product-neutral client segmentation in qualified<br />

and retail clients in line with the MiFID. This distinction allows the<br />

regulations to be oriented toward retail clients.<br />

Simplified representation<br />

less<br />

comprehensive<br />

existing regulations<br />

under discussion<br />

FINMA<br />

Discussion<br />

Paper<br />

Singapore MiFID<br />

Germany<br />

France<br />

• Italy: Professional clients must also understand the liquidity risks<br />

when purchasing illiquid products.<br />

• Hong Kong: Selected structured products, such as accumulators<br />

or decumulators, should only be sold to professional clients;<br />

maximum care should be applied with private investors.<br />

• Singapore: Wealthy private clients should be considered<br />

institutional investors and are excluded from investor protection.<br />

Specific national client segmentation regulations for special<br />

financial constructs, for example British “child trust funds”, will<br />

not be discussed here.<br />

MiFID<br />

Consultation<br />

Paper<br />

GB<br />

Italy<br />

Hong Kong<br />

more<br />

compre-<br />

hensive<br />

Ernst & Young <strong>Relaunch</strong> <strong>Investment</strong> <strong>Suitability</strong><br />

However, the division of clients into three categories (retail<br />

investor, professional clients and eligible counterparties) is<br />

called into question once more in the MiFID’s consultation paper;<br />

a judgement by the European Commission has shown that, in<br />

practice, risk comprehension by some professional clients proved<br />

inadequate, particularly in the case of very complex products,<br />

something which has resulted in legal disputes.<br />

Trend<br />

A clear trend is not evident. In<br />

practice, however, the distinction<br />

between ordinary and professional<br />

clients with regard to conduct at the<br />

point of sale has not resulted in the<br />

expected benefits. Professional clients<br />

also require a detailed risk disclosure<br />

as regards specific products.<br />

15