The Future Of Airline Distribution - IATA

The Future Of Airline Distribution - IATA

The Future Of Airline Distribution - IATA

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>The</strong> <strong>Future</strong> of <strong>Airline</strong> <strong>Distribution</strong> - A Look Ahead To 2017<br />

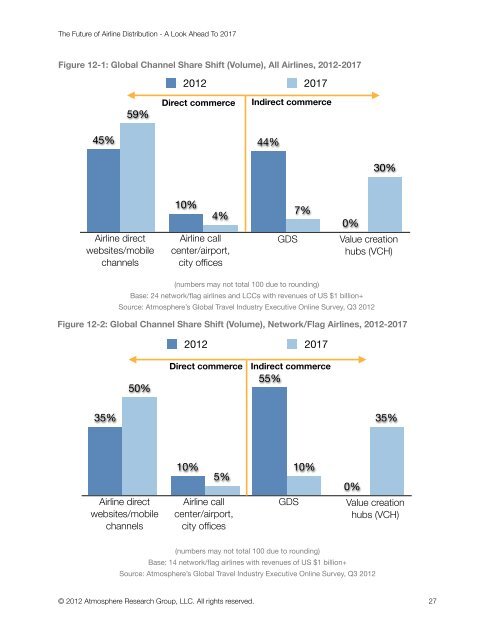

Figure 12-1: Global Channel Share Shift (Volume), All <strong>Airline</strong>s, 2012-2017<br />

45%<br />

59%<br />

<strong>Airline</strong> direct<br />

websites/mobile<br />

channels<br />

2012 2017<br />

10%<br />

4%<br />

<strong>Airline</strong> call<br />

center/airport,<br />

city offices<br />

44%<br />

30%<br />

© 2012 Atmosphere Research Group, LLC. All rights reserved. 27<br />

7%<br />

(numbers may not total 100 due to rounding)<br />

0%<br />

GDS Value creation<br />

hubs (VCH)<br />

Base: 24 network/flag airlines and LCCs with revenues of US $1 billion+<br />

Source: Atmosphere’s Global Travel Industry Executive Online Survey, Q3 2012<br />

Figure 12-2: Global Channel Share Shift (Volume), Network/Flag <strong>Airline</strong>s, 2012-2017<br />

35%<br />

50%<br />

<strong>Airline</strong> direct<br />

websites/mobile<br />

channels<br />

Direct commerce Indirect commerce<br />

2012 2017<br />

Direct commerce<br />

10%<br />

5%<br />

<strong>Airline</strong> call<br />

center/airport,<br />

city offices<br />

Indirect commerce<br />

55%<br />

10%<br />

(numbers may not total 100 due to rounding)<br />

0%<br />

35%<br />

GDS Value creation<br />

hubs (VCH)<br />

Base: 14 network/flag airlines with revenues of US $1 billion+<br />

Source: Atmosphere’s Global Travel Industry Executive Online Survey, Q3 2012