Lighting Strategy - Philips

Lighting Strategy - Philips

Lighting Strategy - Philips

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

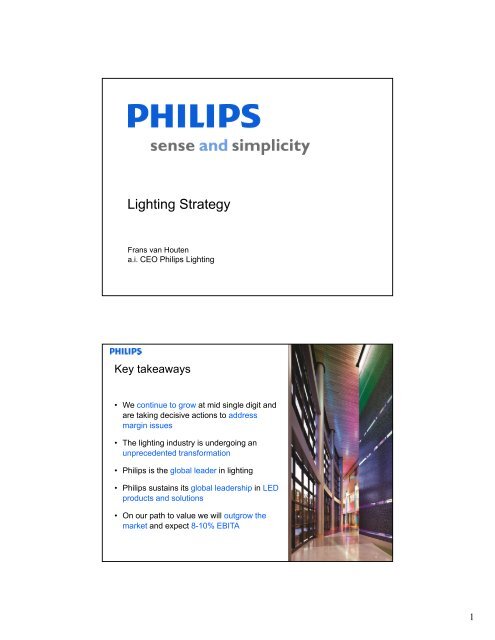

<strong>Lighting</strong> <strong>Strategy</strong><br />

Frans van Houten<br />

a.i. CEO <strong>Philips</strong> <strong>Lighting</strong><br />

Key takeaways<br />

• We continue to grow at mid single digit and<br />

are taking decisive actions to address<br />

margin issues<br />

• The lighting industry is undergoing an<br />

unprecedented transformation<br />

• <strong>Philips</strong> is the global leader in lighting<br />

• <strong>Philips</strong> sustains its global leadership in LED<br />

products and solutions<br />

• On our path to value we will outgrow the<br />

market and expect 8-10% EBITA<br />

2<br />

3<br />

24<br />

1

Key takeaways<br />

• We continue to grow at mid single digit and<br />

are taking decisive actions to address<br />

margin issues<br />

• The lighting industry is undergoing an<br />

unprecedented transformation<br />

• <strong>Philips</strong> is the global leader in lighting<br />

• <strong>Philips</strong> sustains its global leadership in LED<br />

products and solutions<br />

• On our path to value we will outgrow the<br />

market and expect 8-10% EBITA<br />

We have undertaken actions to address issues with<br />

our performance<br />

Results impacted by<br />

• Slower market growth<br />

• Operational issues in Consumer Luminaires and Brazil<br />

• Lower sales in Lumileds driven by Display business<br />

• Margin pressure driven by higher material prices and unfavorable mix<br />

• Investments for growth, in R&D and go-to-market<br />

Decisive actions…<br />

• Increase prices<br />

• Improve mix<br />

• Reduce costs<br />

• Fix operational issues<br />

…while maintaining investments<br />

25<br />

26<br />

2

Key takeaways<br />

• We continue to grow at mid single digit and<br />

are taking decisive actions to address<br />

margin issues<br />

• The lighting industry is undergoing an<br />

unprecedented transformation<br />

• <strong>Philips</strong> is the global leader in lighting<br />

• <strong>Philips</strong> sustains its global leadership in LED<br />

products and solutions<br />

• On our path to value we will outgrow the<br />

market and expect 8-10% EBITA<br />

The lighting industry is transforming and offers<br />

significant growth opportunities<br />

Global General Illumination 1 market forecasted to<br />

grow to around EUR 80 Bln by 2015…<br />

EUR billion<br />

75 - 80<br />

2011<br />

Conventional lighting<br />

LED lighting<br />

CAGR of<br />

5 – 7%<br />

1 Excluding Automotive <strong>Lighting</strong> and LED components market<br />

Source: <strong>Philips</strong> <strong>Lighting</strong> global market study 2010, updated for 2011<br />

2015<br />

…driven by LED, legislation and increasing light<br />

points in growth geographies<br />

• <strong>Lighting</strong> market will grow faster than GDP,<br />

driven by:<br />

– LED: LED penetration forecasted to<br />

grow to ~45% by 2015<br />

– Energy efficiency: Many governments<br />

are phasing out inefficient lighting<br />

technologies<br />

– Growth in light points: Increased<br />

electrification leading to strong growth in<br />

light points in growth geographies<br />

• Conventional lighting continues to be a large<br />

part of the market<br />

27<br />

28<br />

3

<strong>Lighting</strong> industry value is gradually migrating from<br />

light sources to applications and solutions<br />

Strong growth forecasted in the applications 1<br />

market…<br />

2011<br />

CAGR<br />

7-8%<br />

2013<br />

2015<br />

1 Includes Luminaires and <strong>Lighting</strong> controls, but excludes home controls market<br />

2 Digital <strong>Lighting</strong> includes LED lighting and <strong>Lighting</strong> controls<br />

Source: <strong>Philips</strong> <strong>Lighting</strong> global market study 2010, updated for 2011<br />

…driven by transition to LED and increasing<br />

demand for integrated solutions<br />

• Currently, applications constitute ~70% of<br />

the global lighting market<br />

• Penetration of LED based lighting fixtures is<br />

forecasted to be over 50% by 2015<br />

• Penetration of LEDs in road lighting in China<br />

increased from 30% in<br />

2010<br />

• Digital lighting 2 driving the penetration of<br />

intelligent solutions (e.g. telemonitoring,<br />

daylight harvesting etc.)<br />

<strong>Philips</strong> has a unique position in a changing lighting<br />

competitive landscape<br />

Digital <strong>Lighting</strong> value chain The changing industry landscape<br />

LED<br />

components<br />

Electronics<br />

/ LED chip<br />

players<br />

Modules/<br />

bulbs<br />

LED bulbs /<br />

modules<br />

players<br />

Luminaires<br />

LED<br />

luminaires<br />

players<br />

Controls/<br />

solutions<br />

<strong>Lighting</strong>/<br />

building<br />

controls<br />

players<br />

• Traditional value chain had:<br />

– 3 to 4 global and few local lamps<br />

players<br />

– 6 to 8 regional and thousands of local<br />

luminaires players<br />

• Lower barriers to entry in LEDs will initially<br />

mean more players across the value chain –<br />

not all positioned to win<br />

• Building systems and lighting controls players<br />

collaborating on turnkey projects for energy<br />

savings<br />

• <strong>Philips</strong> has an unique advantage, leveraging<br />

strong position across the value chain<br />

29<br />

30<br />

4

Key takeaways<br />

• We continue to grow at mid single digit and<br />

are taking decisive actions to address<br />

margin issues<br />

• The lighting industry is undergoing an<br />

unprecedented transformation<br />

• <strong>Philips</strong> is the global leader in lighting<br />

• <strong>Philips</strong> sustains its global leadership in LED<br />

products and solutions<br />

• On our path to value we will outgrow the<br />

market and expect 8-10% EBITA<br />

<strong>Philips</strong> is the global leader in lighting with a strong<br />

portfolio…<br />

We are the largest lighting company… …with a strong and balanced portfolio<br />

Indexed sales of <strong>Philips</strong> lighting and<br />

top 5 competitors 1<br />

<strong>Philips</strong> 424<br />

Competitor 1 261<br />

Competitor 2 100<br />

Competitor 3 66<br />

Competitor 4 63<br />

Competitor 5 48<br />

2<br />

General <strong>Lighting</strong> Others<br />

1 Sales for competitors based on the latest fiscal year information<br />

2 Includes backlighting, display / flash, projector lighting and other<br />

non-general illumination categories<br />

6%<br />

11%<br />

Total sales<br />

EUR 7.6 Bln<br />

28%<br />

8%<br />

Lamps<br />

Packaged LEDs<br />

Professional Luminaires<br />

and Controls<br />

Last 12 months<br />

June ‘11<br />

6%<br />

41%<br />

Consumer Luminaires<br />

Drivers and modules<br />

Automotive<br />

31<br />

32<br />

5

…with strong coverage across geographies…<br />

We have global coverage… …with strong presence in growth geographies<br />

29%<br />

EMEA<br />

North America<br />

Total sales<br />

EUR 7.6 Bln<br />

5%<br />

Last 12 months<br />

June ‘11<br />

27%<br />

…and segments<br />

39%<br />

Asia Pacific<br />

Latin America<br />

<strong>Philips</strong> <strong>Lighting</strong><br />

Customer Segments 1<br />

61%<br />

Total sales<br />

EUR 7.6 Bln<br />

Last 12 months<br />

June ‘11<br />

Growth Geographies<br />

Mature geographies<br />

Homes Offices Outdoor Industry Retail Hospitality Entertainment Healthcare Automotive<br />

23%<br />

1 Indicative split<br />

17% 15% 10% 15% 5% 3% 4% 8%<br />

More than 75% of our revenue is from<br />

professional customer segments<br />

39%<br />

33<br />

34<br />

6

We are the leading global lighting brand with high<br />

customer loyalty<br />

Strong brand preference vs. competition… …helping us to maintain market leadership<br />

<strong>Philips</strong> <strong>Lighting</strong> brand equity index 1 , 2010<br />

<strong>Philips</strong> <strong>Lighting</strong><br />

Competitor 1<br />

Average<br />

Competitor 2<br />

Competitor 3<br />

1 <strong>Philips</strong> brand equity study 2010<br />

2 Customer panels and Industry associations<br />

3 General Illumination only<br />

85<br />

84<br />

100<br />

100<br />

131<br />

Lamps<br />

Consumer<br />

Luminaires<br />

Professional<br />

Luminaires<br />

Systems &<br />

Controls<br />

Automotive<br />

Packaged<br />

LEDs3 Overall<br />

<strong>Lighting</strong><br />

YoY change in market share 2 , 1H 2011<br />

Europe<br />

North<br />

America<br />

Latin<br />

America<br />

Asia/<br />

Pacific<br />

Share gain Neutral Share loss<br />

And we are the leading LED lighting company<br />

Strong positions in LED lighting Robust growth across our LED portfolio<br />

• LED licensing program with over 140<br />

licensees is clear testimony of our LED<br />

innovation leadership<br />

• One of the leading lighting packaged LEDs<br />

players worldwide<br />

• LED lamps market share exceeds our share<br />

in conventional lamps<br />

• Largest LED luminaires company<br />

Last 12 months sales, EUR million<br />

466<br />

Q2 ’09<br />

CAGR<br />

+52%<br />

797<br />

Q2 ’10<br />

1,081<br />

Q2 ’11<br />

Total<br />

35<br />

36<br />

7

Key takeaways<br />

• We continue to grow at mid single digit and<br />

are taking decisive actions to address<br />

margin issues<br />

• The lighting industry is undergoing an<br />

unprecedented transformation<br />

• <strong>Philips</strong> is the global leader in lighting<br />

• <strong>Philips</strong> sustains its global leadership in LED<br />

products and solutions<br />

• On our path to value we will outgrow the<br />

market and expect 8-10% EBITA<br />

We have a strategy to maintain leadership in<br />

conventional lighting and win in LEDs / applications<br />

Global General Illumination 1 market<br />

EUR billion<br />

90–100<br />

1<br />

2011 2015<br />

2020<br />

LED luminaires and controls<br />

Conventional luminaires<br />

1 Excluding Automotive <strong>Lighting</strong> and LED components market<br />

Source: <strong>Philips</strong> <strong>Lighting</strong> global market study 2010, updated for 2011<br />

2<br />

3<br />

LED lamps and modules<br />

Conventional lamps and drivers<br />

1<br />

Win “golden tail” in conventional<br />

lamp and drivers.<br />

Create flexibility to anticipate slower<br />

or faster phase out<br />

2<br />

Leverage growth opportunity in LED<br />

lamps and modules<br />

3<br />

Invest in LED luminaires and<br />

controls to secure future leadership<br />

37<br />

38<br />

8

Sustaining our leadership position in LED lighting<br />

and solutions…<br />

Building blocks Our strategy<br />

Sustaining<br />

value creation<br />

in Lamps<br />

Driving value<br />

creation in<br />

applications<br />

and solutions<br />

Winning in<br />

mature and<br />

growth<br />

geographies<br />

• Capitalize on portfolio, distribution and brand in conventional<br />

to sustain leadership in LED<br />

• Extract maximum value from conventional lamps while<br />

effectively managing our industrial footprint<br />

• Capitalize on portfolio, distribution and brand in conventional<br />

to sustain leadership in LED<br />

• Leverage controls portfolio to develop integrated, segment<br />

specific lighting solutions<br />

• Customer engagement through key account management for<br />

end-users, specifiers and OEM customers<br />

• Drive leadership in growth geographies through penetration<br />

into tier 3 /4 cities<br />

..whilst building on necessary strengths for<br />

sustainable value creation<br />

Strengths<br />

<strong>Philips</strong> brand<br />

Cost-efficiency and<br />

responsiveness<br />

Go-to-market<br />

strength<br />

Global footprint<br />

1 Consumer brand equity study 2010<br />

Innovation leader<br />

• World’s 42nd most valuable brand in 2010 compared to 65th in 2004<br />

• Consistently among top-ranked players, top 10% in India, China and Brazil,<br />

top 20% globally in the Corporate brand equity index1 • Integrated value chain and end-to-end processes for fastest time-to-market<br />

• Low-cost and highly efficient manufacturing and supply base<br />

• Strong Key Account Management and specifier relations<br />

• Strong coverage in 4 metropolitan cities and 32 main cities in China<br />

• Over 1 million selling points through wholesale in India<br />

• Leader in LED lighting innovation (e.g. L-prize), with an established<br />

technology roadmap, ahead of competition<br />

• Leading IP position acknowledged across the industry<br />

• Serving customers in over 180 countries<br />

• Growth geographies contributing around 40% of our total revenue<br />

• Global presence driving scale<br />

39<br />

40<br />

9

Initiatives under Accelerate! are creating a<br />

platform for profitable growth<br />

Accelerate! for <strong>Lighting</strong><br />

Customer<br />

centricity<br />

End-to-end<br />

excellence<br />

Operating<br />

model /<br />

Cost reduction<br />

Growth and<br />

performance<br />

culture<br />

Resource to Win<br />

• We strengthen and empower market teams to drive entrepreneurship and local<br />

relevance so that customers can be served better<br />

• End-to-end process optimization to improve time-to-market and supply chain<br />

performance<br />

• Simplify <strong>Lighting</strong> organization to drive speed and accountability<br />

• Overhead cost reduction yielding significant cost savings (~EUR 200M)<br />

• Accelerated footprint rationalization<br />

• Drive accountability and entrepreneurship<br />

• Improved performance management at business-market combination level<br />

• Granular plans with step-up in investments for growth in R&D (LED, solutions and<br />

controls) and go-to-market (key account management, solution selling)<br />

• IP creation and leverage<br />

Initiatives under Accelerate! are creating a<br />

platform for profitable growth<br />

Accelerate! for <strong>Lighting</strong><br />

Customer<br />

centricity<br />

End-to-end<br />

excellence<br />

Operating<br />

model /<br />

Cost reduction<br />

Growth and<br />

performance<br />

culture<br />

• We strengthen and empower market teams to drive entrepreneurship and local<br />

relevance so that customers can be served better<br />

• End-to-end process optimization to improve time-to-market and supply chain<br />

performance<br />

• Simplify <strong>Lighting</strong> organization to drive speed and accountability<br />

• Overhead cost reduction yielding significant cost savings (~EUR 200M)<br />

• Accelerated footprint rationalization<br />

• Drive accountability and entrepreneurship<br />

• Improved performance management at business-market combination level<br />

Resource to Win • Granular plans with step-up in investments for growth in R&D (LED, solutions and<br />

controls) and go-to-market (key account management, solution selling)<br />

• IP creation and leverage<br />

41<br />

42<br />

10

We invest to drive performance across the value<br />

chain, leveraging our vertical model in LED…<br />

Investments<br />

Vertical Model<br />

benefits<br />

Product /<br />

Technology<br />

Operations<br />

Go-to-<br />

Market<br />

Packaged LED Bulbs / modules Luminaires / Controls / Solutions<br />

• Performance/cost<br />

leadership in LED for<br />

illumination<br />

• Capacity/scale<br />

• Operational excellence<br />

• Portfolio expansion<br />

• Performance/cost leadership<br />

• Standardization<br />

• Low cost operations<br />

• Reduced time-to-market<br />

• LEDification of luminaires portfolio<br />

• Strengthen portfolio in controls<br />

• <strong>Lighting</strong> system development<br />

• Low cost operations<br />

• Reduced time-to-market<br />

• Increase distribution reach • Customer/ specifier relations • Customer/ specifier relations<br />

• Solution selling<br />

• Expand reach in growth<br />

geographies<br />

Drive scale in packaged LEDs through <strong>Philips</strong>’ LED growth<br />

Fast product development through common platforms and end-to-end value chain coordination<br />

Best performance and lowest cost at system level<br />

Secure LED supply at lowest cost<br />

..focusing our R&D on key growth areas and growth<br />

geographies<br />

Focusing our R&D investments on key growth<br />

areas…<br />

Conventional<br />

1<br />

Digital<br />

R&D investment by technology type<br />

2008<br />

2010<br />

1 Includes investments in LEDs and Controls<br />

2011<br />

2015<br />

100%<br />

…and increasing our R&D footprint in growth<br />

geographies<br />

EMEA<br />

NA<br />

APR<br />

2008<br />

R&D FTE distribution by region<br />

2010<br />

2011<br />

2015<br />

100%<br />

43<br />

44<br />

11

Key takeaways<br />

• We continue to grow at mid single digit and<br />

are taking decisive actions to address<br />

margin issues<br />

• The lighting industry is undergoing an<br />

unprecedented transformation<br />

• <strong>Philips</strong> is the global leader in lighting<br />

• <strong>Philips</strong> sustains its global leadership in LED<br />

products and solutions<br />

• On our path to value we will outgrow the<br />

market and expect 8-10% EBITA<br />

Improve <strong>Lighting</strong> performance to achieve mid term<br />

target of 8-10% EBITA by 2013<br />

15<br />

10<br />

Comp.<br />

Sales<br />

Growth (%)<br />

5<br />

0-<br />

4<br />

<strong>Philips</strong> <strong>Lighting</strong> Mid-Term Performance box<br />

Performance<br />

Box 2013<br />

8 10 12<br />

EBITA %<br />

Mid-Term financial objectives (2013)<br />

Sales growth CAGR 1 6 – 8%<br />

<strong>Lighting</strong> reported 2 EBITA 8 – 10%<br />

1 Assuming market growth of 5 -7%<br />

2 Including restructuring and acquisition related charges<br />

45<br />

46<br />

12

Key takeaways<br />

• We continue to grow at mid single digit and<br />

are taking decisive actions to address<br />

margin issues<br />

• The lighting industry is undergoing an<br />

unprecedented transformation<br />

• <strong>Philips</strong> is the global leader in lighting<br />

• <strong>Philips</strong> sustains its global leadership in LED<br />

products and solutions<br />

• On our path to value we will outgrow the<br />

market and expect 8-10% EBITA<br />

47<br />

13