Income Tax Fundamentals 2012, 30th ed. - CengageBrain

Income Tax Fundamentals 2012, 30th ed. - CengageBrain

Income Tax Fundamentals 2012, 30th ed. - CengageBrain

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Licens<strong>ed</strong> to:<br />

c Nruboc/Dreamstime.com<br />

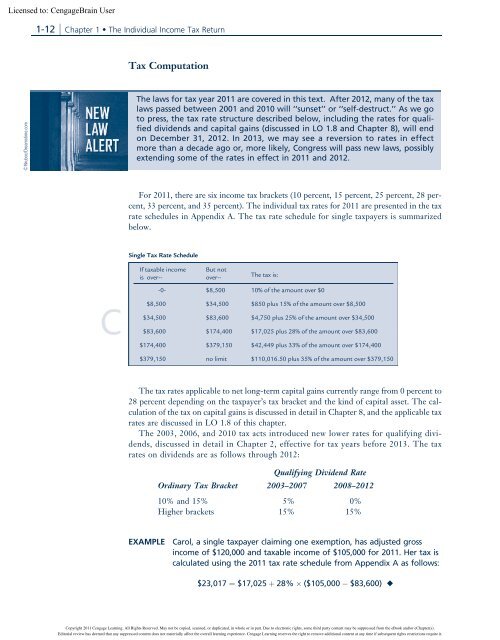

1-12 Chapter 1 The Individual <strong>Income</strong> <strong>Tax</strong> Return<br />

<strong>Tax</strong> Computation<br />

The laws for tax year 2011 are cover<strong>ed</strong> in this text. After <strong>2012</strong>, many of the tax<br />

laws pass<strong>ed</strong> between 2001 and 2010 will ‘‘sunset’’ or ‘‘self-destruct.’’ As we go<br />

to press, the tax rate structure describ<strong>ed</strong> below, including the rates for qualifi<strong>ed</strong><br />

dividends and capital gains (discuss<strong>ed</strong> in LO 1.8 and Chapter 8), will end<br />

on December 31, <strong>2012</strong>. In 2013, we may see a reversion to rates in effect<br />

more than a decade ago or, more likely, Congress will pass new laws, possibly<br />

extending some of the rates in effect in 2011 and <strong>2012</strong>.<br />

For 2011, there are six income tax brackets (10 percent, 15 percent, 25 percent, 28 percent,<br />

33 percent, and 35 percent). The individual tax rates for 2011 are present<strong>ed</strong> in the tax<br />

rate sch<strong>ed</strong>ules in Appendix A. The tax rate sch<strong>ed</strong>ule for single taxpayers is summariz<strong>ed</strong><br />

below.<br />

Single <strong>Tax</strong> Rate Sch<strong>ed</strong>ule<br />

If taxable income<br />

is over--<br />

But not<br />

over--<br />

The tax is:<br />

-0- $8,500 10% of the amount over $0<br />

$8,500 $34,500 $850 plus 15% of the amount over $8,500<br />

$34,500 $83,600 $4,750 plus 25% of the amount over $34,500<br />

$83,600 $174,400 $17,025 plus 28% of the amount over $83,600<br />

$174,400 $379,150 $42,449 plus 33% of the amount over $174,400<br />

$379,150 no limit $110,016.50 plus 35% of the amount over $379,150<br />

The tax rates applicable to net long-term capital gains currently range from 0 percent to<br />

28 percent depending on the taxpayer’s tax bracket and the kind of capital asset. The calculation<br />

of the tax on capital gains is discuss<strong>ed</strong> in detail in Chapter 8, and the applicable tax<br />

rates are discuss<strong>ed</strong> in LO 1.8 of this chapter.<br />

The 2003, 2006, and 2010 tax acts introduc<strong>ed</strong> new lower rates for qualifying dividends,<br />

discuss<strong>ed</strong> in detail in Chapter 2, effective for tax years before 2013. The tax<br />

rates on dividends are as follows through <strong>2012</strong>:<br />

Qualifying Dividend Rate<br />

Ordinary <strong>Tax</strong> Bracket 2003–2007 2008–<strong>2012</strong><br />

10% and 15% 5% 0%<br />

Higher brackets 15% 15%<br />

EXAMPLE Carol, a single taxpayer claiming one exemption, has adjust<strong>ed</strong> gross<br />

income of $120,000 and taxable income of $105,000 for 2011. Her tax is<br />

calculat<strong>ed</strong> using the 2011 tax rate sch<strong>ed</strong>ule from Appendix A as follows:<br />

$23,017 ¼ $17,025 þ 28% ($105,000 $83,600) ◆<br />

Copyright 2011 Cengage Learning. All Rights Reserv<strong>ed</strong>. May not be copi<strong>ed</strong>, scann<strong>ed</strong>, or duplicat<strong>ed</strong>, in whole or in part. Due to electronic rights, some third party content may be suppress<strong>ed</strong> from the eBook and/or eChapter(s).<br />

Editorial review has deem<strong>ed</strong> that any suppress<strong>ed</strong> content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it.