- Page 2:

This page intentionally left blank

- Page 6:

This page intentionally left blank

- Page 10:

EDITOR Lacey Vitetta PROJECT EDITOR

- Page 14:

vi BRIEF CONTENTS PART III PARTIAL

- Page 18:

viii PREFACE TO 2 ND EDITION—A RE

- Page 22:

x PREFACE TO 2 ND EDITION—A READE

- Page 26:

This page intentionally left blank

- Page 30:

This page intentionally left blank

- Page 34:

This page intentionally left blank

- Page 38:

xviii CONTENTS CHAPTER 3 VC RETURNS

- Page 42:

xx CONTENTS Reference 177 Exercises

- Page 46:

xxii CONTENTS Summary 288 Key Terms

- Page 50:

xxiv CONTENTS 23.3 Sequential Games

- Page 54:

This page intentionally left blank

- Page 58:

4 CHAPTER 1 THE VC INDUSTRY EXHIBIT

- Page 62:

6 CHAPTER 1 THE VC INDUSTRY capital

- Page 66:

8 CHAPTER 1 THE VC INDUSTRY Because

- Page 70:

10 CHAPTER 1 THE VC INDUSTRY a succ

- Page 74:

12 CHAPTER 1 THE VC INDUSTRY EXHIBI

- Page 78:

14 CHAPTER 1 THE VC INDUSTRY compan

- Page 82:

16 CHAPTER 1 THE VC INDUSTRY The ma

- Page 86:

18 CHAPTER 1 THE VC INDUSTRY EXHIBI

- Page 90:

20 CHAPTER 1 THE VC INDUSTRY rapid

- Page 94:

22 CHAPTER 2 VC PLAYERS focusing on

- Page 98:

24 CHAPTER 2 VC PLAYERS EXHIBIT 2-2

- Page 102:

26 CHAPTER 2 VC PLAYERS just a few

- Page 106:

28 CHAPTER 2 VC PLAYERS EXHIBIT 2-4

- Page 110:

30 CHAPTER 2 VC PLAYERS true that d

- Page 114:

32 CHAPTER 2 VC PLAYERS methods, we

- Page 118:

34 CHAPTER 2 VC PLAYERS EXAMPLE 2.2

- Page 122:

36 CHAPTER 2 VC PLAYERS As an illus

- Page 126:

38 CHAPTER 2 VC PLAYERS EXHIBIT 2-5

- Page 130:

40 CHAPTER 2 VC PLAYERS restriction

- Page 134:

42 CHAPTER 2 VC PLAYERS GPs are com

- Page 138:

44 CHAPTER 2 VC PLAYERS Distributio

- Page 142:

CHAPTER3 VC RETURNS VCS SPEND their

- Page 146:

48 CHAPTER 3 VC RETURNS EXHIBIT 3-2

- Page 150:

50 CHAPTER 3 VC RETURNS unfolded in

- Page 154:

52 CHAPTER 3 VC RETURNS CA clients

- Page 158:

54 CHAPTER 3 VC RETURNS and the ann

- Page 162:

56 CHAPTER 3 VC RETURNS EXHIBIT 3-5

- Page 166:

58 CHAPTER 3 VC RETURNS Gross value

- Page 170:

60 CHAPTER 3 VC RETURNS EXHIBIT 3-7

- Page 174:

62 CHAPTER 3 VC RETURNS EXHIBIT 3-8

- Page 178:

64 CHAPTER 3 VC RETURNS EXHIBIT 3-9

- Page 182:

66 CHAPTER 4 THE COST OF CAPITAL FO

- Page 186:

68 CHAPTER 4 THE COST OF CAPITAL FO

- Page 190:

70 CHAPTER 4 THE COST OF CAPITAL FO

- Page 194:

72 CHAPTER 4 THE COST OF CAPITAL FO

- Page 198:

74 CHAPTER 4 THE COST OF CAPITAL FO

- Page 202:

76 CHAPTER 4 THE COST OF CAPITAL FO

- Page 206:

78 CHAPTER 4 THE COST OF CAPITAL FO

- Page 210:

80 CHAPTER 4 THE COST OF CAPITAL FO

- Page 214:

82 CHAPTER 4 THE COST OF CAPITAL FO

- Page 218:

84 CHAPTER 5 THE BEST VCs First, we

- Page 222:

86 CHAPTER 5 THE BEST VCs reason to

- Page 226:

88 CHAPTER 5 THE BEST VCs EXHIBIT 5

- Page 230:

90 CHAPTER 5 THE BEST VCs multiple

- Page 234:

92 CHAPTER 5 THE BEST VCs time with

- Page 238:

94 CHAPTER 5 THE BEST VCs among the

- Page 242:

96 CHAPTER 5 THE BEST VCs and other

- Page 246:

98 CHAPTER 5 THE BEST VCs SUMMARY A

- Page 250:

100 CHAPTER 6 VC AROUND THE WORLD E

- Page 254:

102 CHAPTER 6 VC AROUND THE WORLD c

- Page 258:

104 CHAPTER 6 VC AROUND THE WORLD p

- Page 262:

106 CHAPTER 6 VC AROUND THE WORLD T

- Page 266:

108 CHAPTER 6 VC AROUND THE WORLD c

- Page 270:

110 CHAPTER 6 VC AROUND THE WORLD E

- Page 274:

112 CHAPTER 6 VC AROUND THE WORLD 6

- Page 278:

114 CHAPTER 6 VC AROUND THE WORLD P

- Page 282:

116 CHAPTER 6 VC AROUND THE WORLD s

- Page 286:

118 CHAPTER 6 VC AROUND THE WORLD 6

- Page 290:

120 CHAPTER 6 VC AROUND THE WORLD B

- Page 294: This page intentionally left blank

- Page 298: 124 CHAPTER 7 THE ANALYSIS OF VC IN

- Page 302: 126 CHAPTER 7 THE ANALYSIS OF VC IN

- Page 306: 128 CHAPTER 7 THE ANALYSIS OF VC IN

- Page 310: 130 CHAPTER 7 THE ANALYSIS OF VC IN

- Page 314: 132 CHAPTER 7 THE ANALYSIS OF VC IN

- Page 318: 134 CHAPTER 7 THE ANALYSIS OF VC IN

- Page 322: 136 CHAPTER 7 THE ANALYSIS OF VC IN

- Page 326: 138 CHAPTER 7 THE ANALYSIS OF VC IN

- Page 330: 140 CHAPTER 7 THE ANALYSIS OF VC IN

- Page 334: 142 CHAPTER 7 THE ANALYSIS OF VC IN

- Page 338: 144 CHAPTER 7 THE ANALYSIS OF VC IN

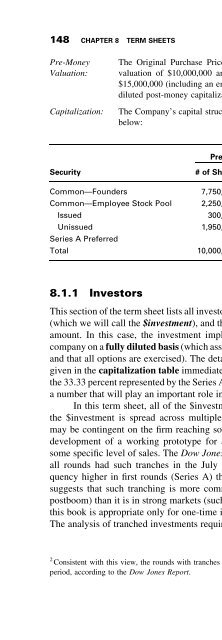

- Page 342: CHAPTER8 TERM SHEETS IN THIS CHAPTE

- Page 348: The real-options analysis of Chapte

- Page 352: 8.2 THE CHARTER The Charter, also k

- Page 356: 8.2.1 Dividends In public companies

- Page 360: A Preferred shall be redeemable fro

- Page 364: Non-Competition and Non-Solicitatio

- Page 368: quarterly, or monthly increments, u

- Page 372: 8.4.2 Founders’ Stock The buyback

- Page 376: CHAPTER9 PREFERRED STOCK IN THE UNI

- Page 380: EXHIBIT 9-2 EXIT DIAGRAM FOR CP CP

- Page 384: Structures IV and V have mandatory

- Page 388: EXHIBIT 9-5 EXIT DIAGRAM FOR RP + C

- Page 392: EXHIBIT 9-9 EXIT DIAGRAM FOR THE SE

- Page 396:

EXHIBIT 9-12 EXIT PROCEEDS UNDER AL

- Page 400:

9.2 ANTIDILUTION PROVISIONS 175 Pro

- Page 404:

KEY TERMS Conversion condition, Con

- Page 408:

about the reduction to the proposed

- Page 412:

10.1 THE VC METHOD: INTRODUCTION 18

- Page 416:

for all first-round investments was

- Page 420:

our estimate of the exit valuation.

- Page 424:

Conceptually, it is straightforward

- Page 428:

EXHIBIT 10-2 VC METHOD SPREADSHEET

- Page 432:

Step 4: For this example, we assume

- Page 436:

EXERCISES 193 (a) Suppose that each

- Page 440:

CHAPTER11 DCF ANALYSIS OF GROWTH CO

- Page 444:

figure out how long rapid growth wi

- Page 448:

To do this, we abstract from the ac

- Page 452:

the acquisition of assets from othe

- Page 456:

EXHIBIT 11-5 NI AND CF CALCULATIONS

- Page 460:

GV 5 ð1 2 g=RÞ E=ðr 2 gÞ: ð11:

- Page 464:

matching the firm’s revenue growt

- Page 468:

EXHIBIT 11-8 REALITY-CHECK DCF MODE

- Page 472:

EXHIBIT 11-9 REALITY-CHECK DCF FOR

- Page 476:

Earnings 5 Net Income Net investmen

- Page 480:

12.1 INTRODUCTION TO COMPARABLES AN

- Page 484:

(not bondholders), the P/E numerato

- Page 488:

12.2 CHOOSING COMPARABLE COMPANIES

- Page 492:

have about $50M in revenue, 150 emp

- Page 496:

EXHIBIT 12-5 VALUATION MULTIPLES 12

- Page 500:

12.3 USING COMPARABLE COMPANIES TO

- Page 504:

KEY TERMS Comparables analysis 5 mu

- Page 508:

PARTIII PARTIAL VALUATION 229

- Page 512:

CHAPTER13 OPTION PRICING PART III P

- Page 516:

13.1 EUROPEAN OPTIONS 233 Exhibit 1

- Page 520:

EXHIBIT 13-3 BOND VALUES ON GOOD DA

- Page 524:

13.2 PRICING OPTIONS USING A REPLIC

- Page 528:

The Black-Scholes formula may look

- Page 532:

is zero. An unbiased approximation

- Page 536:

same Black-Scholes formula to price

- Page 540:

Problem What is the value of the RE

- Page 544:

Problem What is the exit equation c

- Page 548:

investments. Although the assumptio

- Page 552:

EXHIBIT 13-13 SURVIVAL PLOT FOR RE

- Page 556:

In Section 14.3, we show how to ext

- Page 560:

EXHIBIT 14-1 EXIT DIAGRAM FOR THE S

- Page 564:

14.3 EXCESS LIQUIDATION PREFERENCES

- Page 568:

Reality Check: The preceding analys

- Page 572:

EXHIBIT 14-6 SENSITIVITY ANALYSIS F

- Page 576:

14.6 CP WITH EXCESS LIQUIDATION PRE

- Page 580:

EXAMPLE 14.6 Suppose EBV is conside

- Page 584:

EXHIBIT 14-11 EXIT DIAGRAM FOR SERI

- Page 588:

EXHIBIT 14-13 EXIT DIAGRAM FOR SERI

- Page 592:

14.3 Suppose EBV is considering a $

- Page 596:

Problems (a) What is the LP valuati

- Page 600:

A comparison of Equations (15.5) an

- Page 604:

15.2 A CONVERSION SHORTCUT 15.2 A C

- Page 608:

Next, we estimate partial valuation

- Page 612:

EXHIBIT 15-5 EXIT DIAGRAM FOR SERIE

- Page 616:

15.4 DIVIDENDS IN LATER ROUNDS 283

- Page 620:

Series A RVPSðTÞ 5 ð1 1 0:12TAÞ

- Page 624:

Series C conversion condition : 1=3

- Page 628:

valuations considered in Exhibit 15

- Page 632:

for a finite threshold. To solve fo

- Page 636:

proceeds. At W 5 90, this share wou

- Page 640:

The (voluntary) conversion conditio

- Page 644:

(d) Plot the LP valuation for both

- Page 648:

EXHIBIT 16-7 LP VALUATION AND COST

- Page 652:

Series D cap point 5 WDðcapÞ 5 $1

- Page 656:

We can read this diagram as Partial

- Page 660:

CHAPTER17 IMPLIED VALUATION IN CHAP

- Page 664:

EXHIBIT 17-1 VALUE DIVISION AFTER S

- Page 668:

(c) The GP valuation is GP valuatio

- Page 672:

EXHIBIT 17-5 VALUE DIVISION AFTER S

- Page 676:

EXHIBIT 17-6 EXIT DIAGRAM FOR SERIE

- Page 680:

the value of the RP component, and

- Page 684:

We can read this diagram as The LP

- Page 688:

EXERCISES EXERCISES 319 17.1 True,

- Page 692:

proceeds to be given to management.

- Page 696:

We can read this diagram as Partial

- Page 700:

EXHIBIT 18-4 EXIT DIAGRAM FOR MANAG

- Page 704:

(b) To compute the breakeven valuat

- Page 708:

EXHIBIT 18-8 EXIT DIAGRAM FOR THE S

- Page 712:

So far, these are exactly the same

- Page 716:

EXHIBIT 18-10 EXIT DIAGRAM FOR THE

- Page 720:

EXERCISES 335 18.2 We use the same

- Page 724:

PARTIV THE FINANCE OF INNOVATION 33

- Page 728:

CHAPTER19 R&D FINANCE RESEARCH AND

- Page 732:

EXHIBIT 19-2 R&D SHARE OF GDP, MOST

- Page 736:

EXHIBIT 19-4 R&D EXPENDITURE BY SOU

- Page 740:

more than $5B in R&D are “transpo

- Page 744:

the FDA relies heavily on advisory

- Page 748:

EXHIBIT 19-8 FUEL CELL PROJECT Proj

- Page 752:

EXHIBIT 19-9 R&D EXPENDITURE AND CO

- Page 756:

19.3 HOW IS R&D FINANCED? 353 far a

- Page 760:

Exhibits 19-7 and 19-8, summarize t

- Page 764:

CHAPTER20 MONTE CARLO SIMULATION IN

- Page 768:

analyst generates random numbers an

- Page 772:

EXHIBIT 20-3 EVENT TREE WITH THREE

- Page 776:

point x, which can be written as th

- Page 780:

anch represents the maximum of the

- Page 784:

is 5 E 2 $1B f(E). Then, the expect

- Page 788:

EXHIBIT 20-12 LOG-NORMAL PDF 0.5 0.

- Page 792:

EXHIBIT 20-15 MONTE CARLO SIMULATIO

- Page 796:

20.3 SIMULATION WITH MULTIPLE SOURC

- Page 800:

375 EXHIBIT 20-19 DCF MODEL FOR NEW

- Page 804:

of development. (Note that this pro

- Page 808:

21.1 DECISION TREES When a decision

- Page 812:

compute the expected value at Node

- Page 816:

EXAMPLE 21.1 (Fuelco) Fuelco is con

- Page 820:

EXHIBIT 21-5 FUELCO’S DECISION TR

- Page 824:

Denoting shares of the binary optio

- Page 828:

EXHIBIT 21-7 FUELCO’S DECISION TR

- Page 832:

EXHIBIT 21-8 FUELCO’S DECISION TR

- Page 836:

where V(β) is given by Equation (2

- Page 840:

21.5 DRUGCO, REVISITED In this sect

- Page 844:

397 EXHIBIT 21-12 DCF MODEL FOR NEW

- Page 848:

(a) Draw the decision tree for Semi

- Page 852:

EXHIBIT 22-1 CALL OPTION IN A DECIS

- Page 856:

subperiod, we allow only two possib

- Page 860:

22.1 THE BLACK-SCHOLES EQUATION, RE

- Page 864:

EXHIBIT 22-5 JOE’S PROBLEM, BASE

- Page 868:

22.2 MULTIPLE STRIKE PRICES AND EAR

- Page 872:

EXHIBIT 22-9 EXCERPTS FROM TREES FO

- Page 876:

In Exhibit 22-11, we show the optio

- Page 880:

value. Thus, if Fuelco delays the p

- Page 884:

EXHIBIT 22-14 EXCERPTS FROM TREES F

- Page 888:

CHAPTER23 GAME THEORY R&D DECISIONS

- Page 892:

EXHIBIT 23-2 PRISONER’S DILEMMA,

- Page 896:

As in the prisoner’s dilemma game

- Page 900:

EXAMPLE 23.2 Drugco and Pharmco pro

- Page 904:

EXHIBIT 23-8 ODDS-AND-EVENS GAME, N

- Page 908:

Problems (a) Draw the extensive for

- Page 912:

Thus far in the book, we have perfo

- Page 916:

EXHIBIT 23-12 STANDARDS GAME, NORMA

- Page 920:

EXHIBIT 23-14 ENTRY GAME, NORMAL FO

- Page 924:

EXHIBIT 23-16 ENTRY GAME, WITH COMM

- Page 928:

competitor can just come along and

- Page 932:

EXHIBIT 23-19 PROJECT C, STEP 2, WE

- Page 936:

ugly head: both Fuelco and Cellco w

- Page 940:

CHAPTER24 R&D VALUATION IN THIS CHA

- Page 944:

EXHIBIT 24-1 SCHEMATIC FOR THE FULL

- Page 948:

449 EXHIBIT 24-4 DCF MODEL, DEAL 1

- Page 952:

EXHIBIT 24-5 BIGCO NPV AS OF PHASE

- Page 956:

24.1 DRUG DEVELOPMENT 453 (c) To ev

- Page 960:

EXHIBIT 24-9 DRUGCO ZERO-PROFIT CUR

- Page 964:

Problems (a) Draw the decision tree

- Page 968:

EXHIBIT 24-12 FUELCO’S DECISION T

- Page 972:

EXHIBIT 24-14 FUELCO’S DECISION T

- Page 976:

EXHIBIT 24-17 NODE 12, EXPANDED 12

- Page 980:

can reap great rewards, it is dange

- Page 984:

TERM SHEET FOR SERIES A PREFERRED S

- Page 988:

APPENDIX A SAMPLE TERM SHEET 469 Li

- Page 992:

APPENDIX A SAMPLE TERM SHEET 471 of

- Page 996:

APPENDIX A SAMPLE TERM SHEET 473 su

- Page 1000:

[regarding technology ownership, co

- Page 1004:

Lock-up: Investors shall agree in c

- Page 1008:

Non-Competition and Non-Solicitatio

- Page 1012:

holding greater than [1]% of Compan

- Page 1016:

Company breaches this no-shop oblig

- Page 1020:

in Chapters 13. We describe below h

- Page 1024:

APPENDIXC GUIDE TO CRYSTAL BALL s C

- Page 1028:

EXHIBIT C-2 SPREADSHEET SETUP FOR C

- Page 1032:

APPENDIX C GUIDE TO CRYSTAL BALL EX

- Page 1036:

EXHIBIT C-6 RUN PREFERENCES WINDOW

- Page 1040:

EXHIBIT C-8 SPREADSHEET SETUP FOR C

- Page 1044:

APPENDIX C GUIDE TO CRYSTAL BALL EX

- Page 1048:

APPENDIX C GUIDE TO CRYSTAL BALL EX

- Page 1052:

501 EXHIBIT C-13 SPREADSHEET SETUP

- Page 1056:

EXHIBIT C-14 STATISTICAL OUTCOME FO

- Page 1060:

“exercises” are given without s

- Page 1064:

507 EXHIBIT C-19 SPREADSHEET SETUP

- Page 1068:

APPENDIX C GUIDE TO CRYSTAL BALL s

- Page 1072:

REFERENCES 511 EXHIBIT C-24 OUTCOME

- Page 1076:

GLOSSARY 513 Adjusted conversion pr

- Page 1080:

GLOSSARY 515 then general partners

- Page 1084:

GLOSSARY 517 Discount rate: The rat

- Page 1088:

GLOSSARY 519 Expiration diagram: On

- Page 1092:

GLOSSARY 521 Hedge funds: Hedge fun

- Page 1096:

GLOSSARY 523 exclusive (only the li

- Page 1100:

GLOSSARY 525 Mixed-strategy NE: A N

- Page 1104:

GLOSSARY 527 Periodic return: The r

- Page 1108:

GLOSSARY 529 Rapid-growth period: I

- Page 1112:

GLOSSARY 531 Rule 144A: A Securitie

- Page 1116:

GLOSSARY 533 Tagalong: (5 Take-me-a

- Page 1120:

INDEX Abnormal returns, 68, 512 neg

- Page 1124:

EV/Revenue, 216 Price/Book, 217 Pri

- Page 1128:

Exercise price, 518 Exit diagram, 1

- Page 1132:

Implied valuation, 305 319, 521. Se

- Page 1136:

LP cost, 186 LP valuation, 186 Moni

- Page 1140:

Private Equity Performance Monitor,

- Page 1144:

Series C investment, 278 282 exit d

- Page 1148:

spreadsheet, 189 standard VC method