BBA Group Annual Report 2004 - BBA Aviation

BBA Group Annual Report 2004 - BBA Aviation

BBA Group Annual Report 2004 - BBA Aviation

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

24 <strong>BBA</strong> GROUP FINANCIAL<br />

ANNUAL REPORT<br />

<strong>2004</strong> REVIEW<br />

This process was completed in December <strong>2004</strong> and the results<br />

and accompanying notes are shown in the table below.<br />

The areas affected are broadly those described in last<br />

year’s <strong>Annual</strong> <strong>Report</strong> but the following points should be noted:<br />

Financial Assets & Liabilities: Due to the continuing debate<br />

around the final contents of IAS 39 and its acceptance by the<br />

EU, it is not mandatory for the <strong>Group</strong> to include all financial<br />

assets & liabilities on its transition Balance Sheet but<br />

instead to do so at 1 January 2005. It is the <strong>Group</strong>’s intention<br />

to achieve hedge accounting for those transactions which<br />

are entered into for that purpose. To this end, the necessary<br />

documentation of all hedges has been put in place as at<br />

31 December <strong>2004</strong>.<br />

The 2005 Income Statement could be impacted by<br />

potential ineffectiveness of hedges, particularly cash flow<br />

hedges that are entered into based on forecast data. These<br />

forecasts will be reviewed regularly and the effect is not<br />

expected to be material to the <strong>Group</strong>’s earnings.<br />

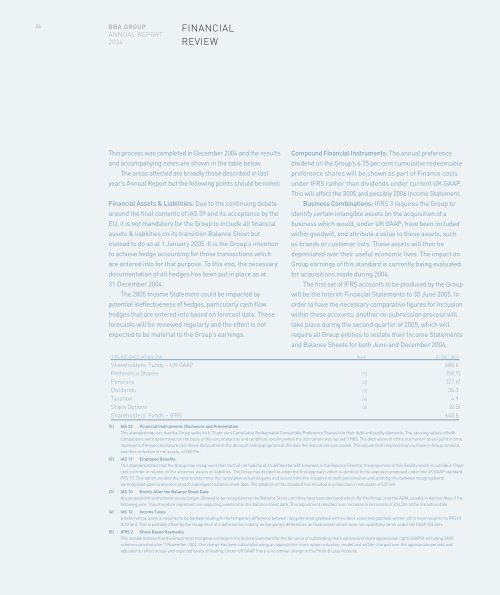

IFRS RECONCILIATION (£M)<br />

Compound Financial Instruments: The annual preference<br />

dividend on the <strong>Group</strong>’s 6.75 per cent cumulative redeemable<br />

preference shares will be shown as part of Finance costs<br />

under IFRS rather than dividends under current UK GAAP.<br />

This will affect the 2005 and possibly 2006 Income Statement.<br />

Business Combinations: IFRS 3 requires the <strong>Group</strong> to<br />

identify certain intangible assets on the acquisition of a<br />

business which would, under UK GAAP, have been included<br />

within goodwill, and attribute a value to these assets, such<br />

as brands or customer lists. These assets will then be<br />

depreciated over their useful economic lives. The impact on<br />

<strong>Group</strong> earnings of this standard is currently being evaluated<br />

for acquisitions made during <strong>2004</strong>.<br />

The first set of IFRS accounts to be produced by the <strong>Group</strong><br />

will be the Interim Financial Statements to 30 June 2005. In<br />

order to have the necessary comparative figures for inclusion<br />

within these accounts, another re-submission process will<br />

take place during the second quarter of 2005, which will<br />

require all <strong>Group</strong> entities to restate their Income Statements<br />

and Balance Sheets for both June and December <strong>2004</strong>.<br />

Note 31 DEC 2003<br />

Shareholders’ Funds – UK GAAP 680.6<br />

Preference Shares (1) (50.9)<br />

Pensions (2) (27.6)<br />

Dividends (3) 34.3<br />

Taxation (4) 4.9<br />

Share Options (5) (0.5)<br />

Shareholders’ Funds – IFRS 640.8<br />

(1) IAS 32 Financial Instruments: Disclosure and Presentation<br />

This standard requires that the <strong>Group</strong> splits its 6.75 per cent Cumulative Redeemable Convertible Preference Shares into their debt and equity elements. The carrying values of both<br />

components were determined on the basis of the circumstances and conditions existing when the instrument was issued (1988). The debt element of the instrument at any point in time<br />

represents the expected future cash flows discounted at the discount rate appropriate at the date the instrument was issued. This adjustment resulted in an increase in <strong>Group</strong> net debt,<br />

and thus reduction in net assets, of £50.9m.<br />

(2) IAS 19 Employee Benefits<br />

This standard states that the <strong>Group</strong> may recognise either the full net liability of its defined benefit schemes in the Balance Sheet or the proportion of this liability which is outside a 10 per<br />

cent corridor in relation to the schemes’ assets or liabilities. The <strong>Group</strong> has decided to adopt the first approach which is identical to the approach proposed under the UK GAAP standard<br />

FRS 17. This option avoided the need to determine the cumulative actuarial gains and losses from the inception of each pension plan and splitting this between recognised and<br />

unrecognised gains and losses at each subsequent balance sheet date. The adoption of this standard has resulted in a reduction in net assets of £27.6m.<br />

(3) IAS 10 Events After the Balance Sheet Date<br />

Any proposed final dividends are no longer allowed to be recognised on the Balance Sheet until they have been declared which, for the <strong>Group</strong>, is at the AGM, usually in April or May of the<br />

following year. They therefore represent non-adjusting events after the balance sheet date. This adjustment resulted in an increase in net assets of £34.3m at the transition date.<br />

(4) IAS 12 Income Taxes<br />

A deferred tax asset is required to be booked relating to the temporary difference between tax generated goodwill with no book value and goodwill written off to reserves prior to FRS10<br />

(£10.5m). This is partially offset by the recognition of a deferred tax liability on temporary differences on fixed assets which were non qualifying items under UK GAAP £(5.6)m.<br />

(5) IFRS 2 Share Based Payments<br />

This standard states that the <strong>Group</strong> must recognise a charge in the Income Statement for the fair value of outstanding share options and share appreciation rights (SARS), including SAYE<br />

schemes granted after 7 November 2002. The charge has been calculated using an appropriate share option valuation model and will be charged over the appropriate periods and<br />

adjusted to reflect actual and expected levels of vesting. Under UK GAAP there is no similar charge in the Profit & Loss Account.