note de conjoncture mars 2000 - Epsilon - Insee

note de conjoncture mars 2000 - Epsilon - Insee

note de conjoncture mars 2000 - Epsilon - Insee

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

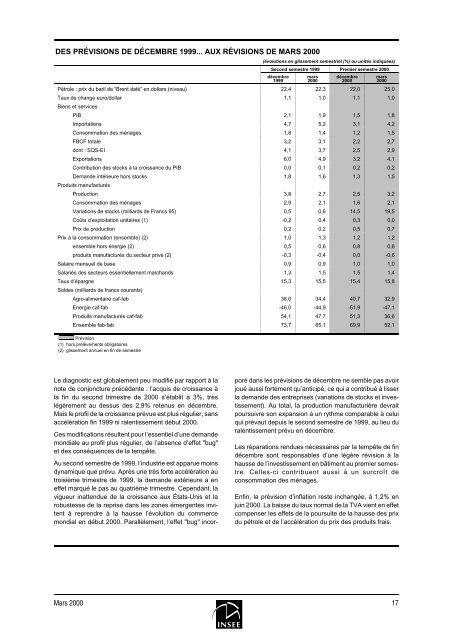

DES PRÉVISIONS DE DÉCEMBRE 1999... AUX RÉVISIONS DE MARS <strong>2000</strong>(évolutions en glissement semestriel (%) ou unités indiquées)Second semestre 1999 Premier semestre <strong>2000</strong>décembre1999<strong>mars</strong><strong>2000</strong>décembre<strong>2000</strong>Pétrole : prix du baril <strong>de</strong> “Brent daté” en dollars (niveau) 22,4 22,3 22,0 25,0Taux <strong>de</strong> change euro/dollar 1,1 1,0 1,1 1,0Biens et servicesPIB 2,1 1,9 1,5 1,8Importations 4,7 5,2 3,1 4,2Consommation <strong>de</strong>s ménages 1,8 1,4 1,2 1,5FBCF totale 3,2 3,1 2,2 2,7dont : SQS-EI 4,1 3,7 2,5 2,9Exportations 6,0 4,9 3,2 4,1Contribution <strong>de</strong>s stocks à la croissance du PIB 0,0 0,1 0,2 0,2Deman<strong>de</strong> intérieure hors stocks 1,8 1,6 1,3 1,5Produits manufacturésProduction 3,8 2,7 2,5 3,2Consommation <strong>de</strong>s ménages 2,9 2,1 1,6 2,1Variations <strong>de</strong> stocks (milliards <strong>de</strong> Francs 95) 0,5 0,6 14,5 19,5Coûts d’exploitation unitaires (1) -0,2 0,4 0,3 0,0Prix <strong>de</strong> production 0,2 0,2 0,5 0,7Prix à la consommation (ensemble) (2) 1,0 1,3 1,2 1,2ensemble hors énergie (2) 0,5 0,6 0,8 0,6produits manufacturés du secteur privé (2) -0,3 -0,4 0,0 -0,6Salaire mensuel <strong>de</strong> base 0,9 0,9 1,0 1,0Salariés <strong>de</strong>s secteurs essentiellement marchands 1,3 1,5 1,5 1,4Taux d’épargne 15,3 15,5 15,4 15,8Sol<strong>de</strong>s (milliards <strong>de</strong> francs courants)Agro-alimentaire caf-fab 38,0 34,4 40,7 32,9Energie caf-fab -46,0 -44,9 -51,9 -47,1Produits manufacturés caf-fab 54,1 47,7 51,3 36,6Ensemble fab-fab 73,7 65,1 69,9 52,1Prévision(1) hors prélèvements obligatoires(2) glissement annuel en fin <strong>de</strong> semestre<strong>mars</strong><strong>2000</strong>Le diagnostic est globalement peu modifié par rapport à la<strong>note</strong> <strong>de</strong> <strong>conjoncture</strong> précé<strong>de</strong>nte : l’acquis <strong>de</strong> croissance àla fin du second trimestre <strong>de</strong> <strong>2000</strong> s’établit à 3%, trèslégèrement au <strong>de</strong>ssus <strong>de</strong>s 2,9% retenus en décembre.Mais le profil <strong>de</strong> la croissance prévue est plus régulier, sansaccélèration fin 1999 ni ralentissement début <strong>2000</strong>.Ces modifications résultent pour l’essentiel d’une <strong>de</strong>man<strong>de</strong>mondiale au profil plus régulier, <strong>de</strong> l’absence d’effet "bug"et <strong>de</strong>s conséquences <strong>de</strong> la tempête.Au second semestre <strong>de</strong> 1999, l’industrie est apparue moinsdynamique que prévu. Après une très forte accélération autroisième trimestre <strong>de</strong> 1999, la <strong>de</strong>man<strong>de</strong> extérieure a eneffet marqué le pas au quatrième trimestre. Cependant, lavigueur inattendue <strong>de</strong> la croissance aux États-Unis et larobustesse <strong>de</strong> la reprise dans les zones émergentes invitentà reprendre à la hausse l’évolution du commercemondial en début <strong>2000</strong>. Parallèlement, l’effet "bug" incorporédans les prévisions <strong>de</strong> décembre ne semble pas avoirjoué aussi fortement qu’anticipé, ce qui a contribué à lisserla <strong>de</strong>man<strong>de</strong> <strong>de</strong>s entreprises (variations <strong>de</strong> stocks et investissement).Au total, la production manufacturière <strong>de</strong>vraitpoursuivre son expansion à un rythme comparable à celuiqui prévaut <strong>de</strong>puis le second semestre <strong>de</strong> 1999, au lieu duralentissement prévu en décembre.Les réparations rendues nécessaires par la tempête <strong>de</strong> findécembre sont responsables d’une légère révision à lahausse <strong>de</strong> l’investissement en bâtiment au premier semestre.Celles-ci contribuent aussi à un surcroît <strong>de</strong>consommation <strong>de</strong>s ménages.Enfin, la prévision d’inflation reste inchangée, à 1,2% enjuin <strong>2000</strong>. La baisse du taux normal <strong>de</strong> la TVA vient en effetcompenser les effets <strong>de</strong> la poursuite <strong>de</strong> la hausse <strong>de</strong>s prixdu pétrole et <strong>de</strong> l’accélération du prix <strong>de</strong>s produits frais.Mars <strong>2000</strong> 17