Forecasting the Bankruptcy Risk on the Example of Romanian ...

Forecasting the Bankruptcy Risk on the Example of Romanian ...

Forecasting the Bankruptcy Risk on the Example of Romanian ...

- No tags were found...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

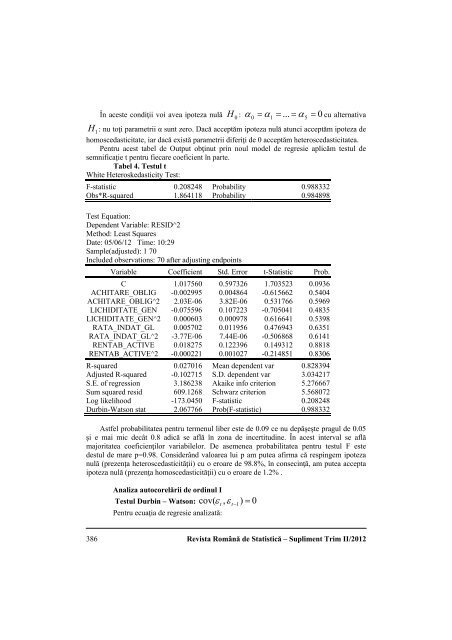

În aceste c<strong>on</strong>diţii voi avea ipoteza nulă 0H : 0 1 ... 5 0cu alternativaH1 : nu toţi parametrii α sunt zero. Dacă acceptăm ipoteza nulă atunci acceptăm ipoteza dehomoscedasticitate, iar dacă există parametrii diferiţi de 0 acceptăm heteroscedasticitatea.Pentru acest tabel de Output obţinut prin noul model de regresie aplicăm testul desemnificaţie t pentru fiecare coeficient în parte.Tabel 4. Testul tWhite Heteroskedasticity Test:F-statistic 0.208248 Probability 0.988332Obs*R-squared 1.864118 Probability 0.984898Test Equati<strong>on</strong>:Dependent Variable: RESID^2Method: Least SquaresDate: 05/06/12 Time: 10:29Sample(adjusted): 1 70Included observati<strong>on</strong>s: 70 after adjusting endpointsVariable Coefficient Std. Error t-Statistic Prob.C 1.017560 0.597326 1.703523 0.0936ACHITARE_OBLIG -0.002995 0.004864 -0.615662 0.5404ACHITARE_OBLIG^2 2.03E-06 3.82E-06 0.531766 0.5969LICHIDITATE_GEN -0.075596 0.107223 -0.705041 0.4835LICHIDITATE_GEN^2 0.000603 0.000978 0.616641 0.5398RATA_INDAT_GL 0.005702 0.011956 0.476943 0.6351RATA_INDAT_GL^2 -3.77E-06 7.44E-06 -0.506868 0.6141RENTAB_ACTIVE 0.018275 0.122396 0.149312 0.8818RENTAB_ACTIVE^2 -0.000221 0.001027 -0.214851 0.8306R-squared 0.027016 Mean dependent var 0.828394Adjusted R-squared -0.102715 S.D. dependent var 3.034217S.E. <strong>of</strong> regressi<strong>on</strong> 3.186238 Akaike info criteri<strong>on</strong> 5.276667Sum squared resid 609.1268 Schwarz criteri<strong>on</strong> 5.568072Log likelihood -173.0450 F-statistic 0.208248Durbin-Wats<strong>on</strong> stat 2.067766 Prob(F-statistic) 0.988332Astfel probabilitatea pentru termenul liber este de 0.09 ce nu depăşeşte pragul de 0.05şi e mai mic decât 0.8 adică se află în z<strong>on</strong>a de incertitudine. În acest interval se aflămajoritatea coeficienţilor variabilelor. De asemenea probabilitatea pentru testul F estedestul de mare p=0.98. C<strong>on</strong>siderând valoarea lui p am putea afirma că respingem ipotezanulă (prezenţa heteroscedasticităţii) cu o eroare de 98.8%, în c<strong>on</strong>secinţă, am putea acceptaipoteza nulă (prezenţa homoscedasticităţii) cu o eroare de 1.2% .Analiza autocorelării de ordinul ITestul Durbin – Wats<strong>on</strong>: cov( ,1) 0Pentru ecuaţia de regresie analizată:t t386Revista Română de Statistică – Supliment Trim II/2012