Monthly Economic Bulletin October 2010 - Banco Mercantil

Monthly Economic Bulletin October 2010 - Banco Mercantil

Monthly Economic Bulletin October 2010 - Banco Mercantil

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

ECONOMIC SITUATION<br />

Oil Market<br />

External Sector<br />

Government Finance<br />

Public Debt<br />

Monetary Market<br />

Interest Rates<br />

Real Sector<br />

Labor Market<br />

Prices<br />

NEW LEGISLATION<br />

ECONOMIC INDICATORS<br />

ECONOMIC SITUATION<br />

GEMA MURILLO *<br />

gmurillo@bancomercantil.com<br />

1<br />

CONTENT<br />

OIL MARKET<br />

The prices of the principal marker crudes increased<br />

substantially in the month of <strong>October</strong> over September,<br />

when there were only minor adjustments and, in some<br />

cases, actual declines. This development was largely<br />

explained by expectations of another round of major<br />

financial stimulus in the United States. Starting in <strong>October</strong>,<br />

petroleum prices reflected the belief that the Federal<br />

Reserve would increase the supply of money and affect the<br />

value of the dollar early in November.<br />

As a result, the average price of the WTI marker crude in<br />

<strong>October</strong> reached US$/b 81.9 for an 8.9% increase over<br />

September when this marker had fallen by 2.3%. The<br />

OCTOBER <strong>2010</strong><br />

average year-to-date (January-<strong>October</strong> <strong>2010</strong>) price of WTI<br />

came to US$/b 78.1, for a 33% increase over the same<br />

period of 2009. The average price of the Brent marker<br />

crude came to US$/b 83.5 in <strong>October</strong> for a 7% increase<br />

over September and the highest month-to-month increase<br />

since the month of April. On a year-to-date basis the price<br />

of Brent averaged US$/b 78.5, for a 31.5% rise over the<br />

same period of 2009.<br />

The prices of the OPEC crude basket and of the<br />

Venezuelan export basket followed the changes of the<br />

marker crudes. The average price of the OPEC basket in<br />

<strong>October</strong> of the current year was US$/b 79.8, for a 7.2%<br />

increase over the preceding month and for the highest<br />

month-to-month increase during last year. The average<br />

price of the OPEC basket during the first ten months of the<br />

year came to US$/b 75.7 for a 30.5% rise over the same<br />

period of 2009. The average price of the Venezuelan<br />

export basket was US$/b 74.3, up 9.4% over September<br />

and the highest month-to-month increase since June,<br />

2009. As a result, the average price of the Venezuelan oil<br />

export basket reached US$/b 70, nearly US$/b 16 higher<br />

than during the same period of 2009.<br />

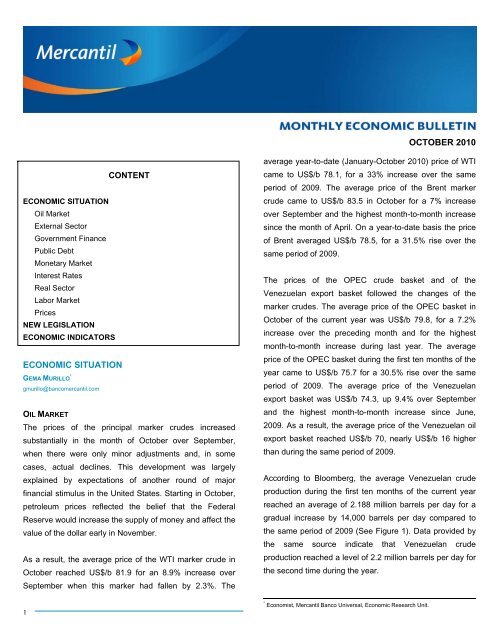

According to Bloomberg, the average Venezuelan crude<br />

production during the first ten months of the current year<br />

reached an average of 2.188 million barrels per day for a<br />

gradual increase by 14,000 barrels per day compared to<br />

the same period of 2009 (See Figure 1). Data provided by<br />

the same source indicate that Venezuelan crude<br />

production reached a level of 2.2 million barrels per day for<br />

the second time during the year.<br />

* Economist, <strong>Mercantil</strong> <strong>Banco</strong> Universal, <strong>Economic</strong> Research Unit.

Crude Oil Production<br />

2<br />

2,550<br />

2,400<br />

2,250<br />

2,100<br />

1,950<br />

1,800<br />

1,650<br />

1,500<br />

Oct-08<br />

Dec-08<br />

Feb-09<br />

Apr-09<br />

Figure 1<br />

Venezuela: Oil Price and Production<br />

Crude Oil Production<br />

Price of the Export Basket<br />

Jun-09<br />

Aug-09<br />

Oct-09<br />

Dec-09<br />

Source: Bloomberg and Ministry of the Popular Power for the Energy and Petroleum<br />

Until US$ 3,000 100% of the position<br />

Greater than US$ 6,000 US$ 5,000<br />

From US$ 3,000 to US$ 750,000 100% of the position<br />

Greater than US$ 750,000 US$ 750,000<br />

Source: PDVSA<br />

Feb-10<br />

Apr-10<br />

Jun-10<br />

Aug-10<br />

Oct-10<br />

90<br />

80<br />

70<br />

60<br />

50<br />

40<br />

30<br />

Price of the Export Basket<br />

was offered for exchange, representing a placement of<br />

US$ 618.6 of the new PDVSA 2013 bond.<br />

EXTERNAL SECTOR<br />

The BCV reported a Balance of Payments deficit of<br />

US$ 221 million in the third quarter of the current year,<br />

substantially better than the US$ 1.006 billion deficit<br />

recorded in the second quarter but still considerably worse<br />

than the US$ 2.364 billion surplus in the third quarter of<br />

2009 (See Table 2). This deficit is due to the combined<br />

effects of the deficits in the Capital and Financial accounts<br />

and in Errors and Omissions which offset the surplus in the<br />

Current account.<br />

In <strong>October</strong>, PDVSA issued the US$ 3 billion “PDVSA 2017”<br />

bond at the official exchange rate of Bs. 4.30 per US dollar.<br />

The total amount was placed. Demand by investors for this<br />

issue reached nearly US$ 7 billion. This bond matures in<br />

November 2017 and carries an 8.5% coupon. PDVSA<br />

required minimum bids of US$ 3,000 and priced the issue<br />

at 100% for a total of Bs. 12.9 billion, to be invested in<br />

PDVSA corporate projects. The procedure followed for the<br />

allocation of the bids is show on Table 1.<br />

This latter account registered a US$ 2.571 billion surplus in<br />

the third quarter of <strong>2010</strong>, similar to the second quarter but<br />

US$ 2.8 billion lower than the surplus recorded in the third<br />

quarter of 2009. This was due to the deceleration of the<br />

commercial surplus by 27.6% as a result of lower exports<br />

and higher imports. In the third quarter of the current year,<br />

petroleum exports, at US$ 14.661 billion, were down 5.4%<br />

Table 1 compared to the same quarter of 2009. This<br />

PETROBONO 2017 Bond Allocation Mechanism result was caused by lower export volumes, in<br />

INDIVIDUALS<br />

view of the fact that oil export prices actually<br />

Ranges Allocation<br />

rose by 6% during the quarter. Imports in that<br />

same third quarter increased by 13% compared<br />

LEGAL PERSONS<br />

to the same period of 2009, due to the increased<br />

Ranges Allocation<br />

purchases of material and equipment for public<br />

works principally for electricity generation. In this<br />

regard it should be noted that the share in<br />

imports by the public sector has increased<br />

PDVSA also offered to exchange the US$ 3 billion<br />

“Petrobono” maturing in 2011 for a new International Bond<br />

maturing in 2013 with an 8% coupon. Venezuelan<br />

individuals and corporations holders of the 2011<br />

considerably over the last six years, reaching 32% of the<br />

total in the third quarter of the current year, for an increase<br />

of 440 basis points (bp) over the same period of 2009<br />

when the level of public sector imports had come to 27.3%.<br />

“Petrobono” would receive an exchange incentive of<br />

US$ 1.125 of the new bond per US$ 1.000 of the<br />

“Petrobono” if they made the exchange before <strong>October</strong> 28.<br />

The incentive would be reduced to US$ 1.095 for<br />

exchanges made later than <strong>October</strong> 28. PDVSA reported<br />

that 18.3% (US$ 550 million) of the original “Petrobono”<br />

The Capital and Financial account showed a deficit of<br />

US$ 1.882 billion, similar to the previous quarter and<br />

32.1% lower than the deficit on record during the third<br />

quarter of 2009. The deficit in this account is basically the<br />

result of the deficit in the Other Investment Account of

US$ 2.0 billion (30% higher than that recorded in the same<br />

quarter of 2009), as the result of the initial disbursements<br />

under the Long-Term Financing granted to BANDES by the<br />

National Bank of China.<br />

The net result of the current capital transactions and<br />

imputations to the Errors and Omissions Account<br />

determined a level of reserves in the hands of the BCV at<br />

the close of September of US$ 28.618 billion, that is,<br />

US$ 6.382 billion less than at the close of 2009 (US$ 35<br />

billion). The most recent information about the international<br />

reserves at the close of <strong>October</strong>, showed a decline by<br />

US$ 5.967 billion compared to the month of December,<br />

mainly as the result of the transfer of US$ 6 billion from the<br />

BCV to FONDEN in the first semester of the year 1 , to reach<br />

a net of US$ 29.033 billion. To be noted is that<br />

approximately half of these reserves correspond to the<br />

BCV position in gold.<br />

In addition, the Foreign Currency Administration<br />

Commission (CADIVI – Comisión de Administración de<br />

1 Originally, the Central Bank had announced its intention of transferring US$ 7<br />

billion to FONDEN during the first semester of the year. To be noted is that, of the<br />

US$ 1 billion remaining, US$ 500 million were transferred in November.<br />

3<br />

Table 2<br />

Balance of Payments<br />

Third Quarter (Million of US$)<br />

2009 <strong>2010</strong><br />

CURRENT ACCOUNT 5,377<br />

Trade Balance 7,623<br />

Total Export 16,445<br />

Oil 15,494<br />

Non-Oil 951<br />

Total Import (8,822)<br />

Oil (1,086)<br />

Non-Oil (7,736)<br />

Services (1,765)<br />

Rent (471)<br />

Current Transfers (10)<br />

CAPITAL & FINANCIAL ACCOUNT (2,773)<br />

Direct Investment (2,143)<br />

Abroad (572)<br />

In the Country (1,571)<br />

Portfolio Investment 909<br />

Other Investment (1,539)<br />

Public Sector 3,036<br />

Private Sector (3,985)<br />

ERRORS & OMISSIONS (240)<br />

GLOBAL BALANCE 2,364<br />

Source: Central Bank of Venezuela<br />

2,571<br />

5,523<br />

15,491<br />

14,661<br />

830<br />

(9,968)<br />

(916)<br />

(9,052)<br />

(2,103)<br />

(726)<br />

(123)<br />

(1,882)<br />

(1,212)<br />

94<br />

(1,306)<br />

1,330<br />

(2,000)<br />

1,778<br />

(2,644)<br />

(910)<br />

(221)<br />

Divisas) published the statistics corresponding to the<br />

authorizations and liquidations of foreign exchange during<br />

the third quarter of the year. According to CADIVI, in the<br />

amount accumulated during the first nine months of the<br />

year, the total requests approved increased by barely 3.2%<br />

compared to the same period of last year, in spite of the<br />

higher oil prices, which stood on average 32.2% higher<br />

than in the first nine months of 2009. Likewise, currency<br />

actually liquidated by the BCV showed a year-on-year<br />

growth of 1.8%, explainable in part by the delays resulting<br />

from the establishment of the new system of multiple<br />

exchange rates at the beginning of the year. Consequently,<br />

during the first nine months of the year, the daily average<br />

of foreign exchange liquidated by the BCV came to<br />

US$ 118 million, 2.5% over the record during the first nine<br />

months of the year 2009.<br />

By type of request, according to s supplied by CADIVI, in<br />

the first three quarters of the year (US$ 20.991 billion)<br />

70.4% went for imports, 14.4% for outlays charged to the<br />

ALADI Agreement, 4.5% for airlines, 4% for credit cards<br />

and 6.7% to Others. To be noted, almost half of the types<br />

of requests for currency declined in comparison with the<br />

same period of 2009. However, the increases shown in the<br />

requests for Imports, Students, Special Cases, Airlines and<br />

Cash for Travels, as a result of their high participation in<br />

the total liquidated foreign exchange (78%), partially offset<br />

the decline in the amount actually liquidated.<br />

The total foreign exchange liquidated for imports during the<br />

period in question, not including imports under the ALADI<br />

Agreement, came to US$ 14.792 billion. Of this amount,<br />

the economic sectors receiving more currency were: Food<br />

(20.8%), Health (19.5%), Automotive (12.1%), Commerce<br />

(12%), Machinery and Equipment (6.7%) and Chemicals<br />

(6.6%). In this connection, to be noted is the significant<br />

growth by 67.4% of liquidations destined to the Health<br />

sector which explains the increase by slightly over 320<br />

basis points (bp) in the participation of the total foreign<br />

exchange for imports, which went from 16.1% in the<br />

January - September period of 2009 to 19.5% in the same

period of this year. This higher participation of the Health<br />

sector was at the expense of the Food and Automotive<br />

sectors, which declined by 252 bp and 185 bp respectively<br />

(See Figure 2).<br />

Foods<br />

Health<br />

Automobile<br />

Commerce<br />

Others<br />

Machineries and Equipment<br />

Metallurgic<br />

Chemistry<br />

Rubber and Plastic<br />

Telecommunications<br />

Services<br />

Informatic<br />

4<br />

Figure 2<br />

Sectorial distribution of FX sold for imports<br />

(Third Quarter)<br />

<strong>2010</strong><br />

2009<br />

0% 5% 10% 15% 20% 25% 30%<br />

Note: Not include imports under ALADI agreement<br />

Source: CADIVI and Own Calculations<br />

The SITME started operations in early June. Up to the end<br />

of September, the daily average of currency provided<br />

through the SITME 2 came to US$ 30.9 million at an implicit<br />

weighted average exchange rate of Bs./US$ 5.30. To be<br />

noted is that the daily average of foreign exchange<br />

delivered through this procedure increased notably during<br />

the month of <strong>October</strong> to US$ 43.2 million. Consequently, a<br />

total of US$ 3.330 billion have been provided through<br />

SITME (See Figure 3).<br />

GOVERNMENT FINANCE<br />

The financial performance of the Central<br />

Government, according to the most recent<br />

information provided by the National Treasury<br />

Office (ONT -Oficina Nacional del Tesoro)<br />

during the first ten months of the year, again<br />

showed a deficit as a result of a moderate<br />

government spending together with still low oil<br />

income on record and its notably diminished<br />

participation within the total revenues.<br />

2 In early June, the BCV approved the System of Transactions with Securities in<br />

Foreign Currency (SITME – Sistema de Transacciones con Títulos en Moneda<br />

Extranjera), by which government securities may be negotiated under the terms and<br />

conditions established by the BCV through authorized financial institutions. For this<br />

purpose, the BCV publishes daily in its web page the maxi-mum and minimum<br />

prices at which securities of the Republic and of PDVSA may be purchased and sold<br />

in bolivares. Companies and individuals may participate in the SITME with restricted<br />

quantities, whereas Commercial and Universal Banks, and Savings and Loans<br />

Entities, act both as intermediaries (ex-change operators) as well as suppliers of<br />

bonds in this new system.<br />

The ordinary revenues of the Central Government during<br />

the first ten months came to Bs. 122 billion (68.1%<br />

provided by non-oil contributions), for an increase of barely<br />

2.9% over the same period of 2009. After adjustment for<br />

the high inflation during the period, the result in real terms<br />

was a decline by 18.3%.<br />

45<br />

40<br />

35<br />

30<br />

25<br />

20<br />

15<br />

10<br />

5<br />

0<br />

Figure 3<br />

SITME<br />

Daily Average (Million of US$)<br />

Jun-10 Jul-10 Aug-10 Sep-10 Oct-10<br />

Source: Central Bank of Venezuela and Own Calculations<br />

To be noted is that the highest nominal cumulative<br />

expansion during the January to <strong>October</strong> period of this<br />

year was in non-oil income (+4.9%), while oil income<br />

declined by -1.2%. In real terms, oil income dropped by<br />

21.6%, and non-oil by 16.7%.<br />

Nominal Real<br />

Jan-Oct 2009 Jan-Oct <strong>2010</strong> Change Change<br />

I.- ORDINARY 118,534 121,965 2.9% -18.3%<br />

Oil 39,391 38,914 -1.2% -21.6%<br />

Tax Income 8,293<br />

7,179 -13.4% -31.3%<br />

PDVSA's Cash Royalties 28,034 30,044 7.2% -15.0%<br />

PDVSA's Dividends 3,064<br />

1,691 -44.8% -56.2%<br />

Non-Oil 79,143 83,051 4.9% -16.7%<br />

Primary Expenditures 135,977 152,854 12.4% -12.8%<br />

Surplus/Deficit (23,199) (30,889) 33.1% 5.7%<br />

Source: National Treasury Office, Central Bank of Venezuela and Own Calculations<br />

Table 3<br />

Central Government Financial Management<br />

Acumulated to <strong>October</strong><br />

Million of Bs.<br />

The nominal decrease of oil income was a result of the<br />

decline in payment of Income Tax (-13.4%) and of<br />

Dividends (-44.8%). This was offset in part by a 7.2%<br />

increase in payment of Royalties (See Table 3). This lower<br />

oil income occurs in a context in which the value in<br />

bolívares of the oil income increased by 100% as a result

of the exchange rate adjustment at the beginning of the<br />

year.<br />

5<br />

Payments and 4.4% to pending obligations budget of the<br />

previous year.<br />

In addition, internal tax collections under SENIAT<br />

jurisdiction came to Bs. 82.6 billion in the first ten months<br />

50%<br />

Figure 4<br />

Primary Expenditures executed by the Treasury<br />

(Accumulated to <strong>October</strong>)<br />

of the year, almost 25% over the same period of 2009.<br />

However, the high inflation rates throughout the year led to<br />

40%<br />

30%<br />

Nominal Change<br />

Real Change<br />

a decline in real terms by 3.6% (during 2009, the real de-<br />

20%<br />

cline was 13.3%). By type of contributions, the Value<br />

10%<br />

Added Tax showed a real year-to-year increase of 6.5%;<br />

0%<br />

Domestic and Customs Incomes increased by barely 0.8%<br />

-10%<br />

2007 2008 2009 <strong>2010</strong><br />

and 0.3% respectively. Income Tax (ISLR – Impuesto<br />

-20%<br />

sobre la Renta) showed a real 17.8% year-on-year decline,<br />

-30%<br />

Source: Ministry of the Popular Power for the Economy and Finances and Own Calculations<br />

930 bp more than the real decline during the same period<br />

of last year (See Table 4).<br />

As a result of the combined effect of increased public<br />

spending and lower growth of ordinary<br />

Table 4<br />

Domestic Taxes income, the Central Government’s fiscal<br />

Acumulated to <strong>October</strong> (Million of Bs.)<br />

performance (ordinary income – ordinary<br />

Income Tax<br />

Value Added Tax<br />

2009<br />

22,235.9<br />

32,692.4<br />

<strong>2010</strong><br />

23,634.7<br />

44,936.8<br />

Nominal Change<br />

6.3%<br />

37.5%<br />

Real Change<br />

-17.8%<br />

6.5%<br />

expenditures) showed a significant deficit<br />

by Bs. 30.9 billion during the first ten<br />

Wholesale Operators<br />

Imports Operators<br />

26,229.6<br />

6,462.8<br />

36,316.4<br />

8,620.4<br />

38.5%<br />

33.4%<br />

7.5%<br />

2.3%<br />

months of the year; this was 33.1% higher<br />

Customs<br />

Domestic Income<br />

Alcoholic Beverages<br />

5,352.8<br />

4,729.5<br />

951.3<br />

7,003.3<br />

6,169.1<br />

1,234.4<br />

30.8%<br />

30.4%<br />

29.8%<br />

0.3%<br />

0.8%<br />

-0.2%<br />

than the deficit during the same period of<br />

2009 (Bs. 23.2 billion), and the highest for<br />

Tabacco<br />

Fiscal Duties<br />

3,415.7<br />

49.4<br />

4,521.0<br />

43.4<br />

32.4%<br />

-12.2%<br />

2.5%<br />

-31.9%<br />

the January-<strong>October</strong> period since the<br />

Inheritance<br />

Gambling & Casinos<br />

Others<br />

145.5<br />

167.6<br />

1,328.1<br />

180.1<br />

190.2<br />

901.3<br />

23.8%<br />

13.5%<br />

-32.1%<br />

-4.7%<br />

-12.2%<br />

-46.8%<br />

monthly statistical series became available<br />

(1998) (See Figure 5). To be noted is that<br />

Total<br />

Source: SENIAT and Own Calculations<br />

66,338.7 82,645.2<br />

24.6% -3.6%<br />

this deficit was basically covered with<br />

domestic public debt.<br />

On the other side of the budget balance, primary<br />

expenditures according to the Treasury stood at Bs. 152.9 Concerning the fiscal budget of this year, the additional<br />

billion during the first ten months of the year, for a nominal credits approved by the National Assembly and decreed by<br />

increase of 12.4% compared to the same period of last the Executive stood at Bs. 66.4 billion up to <strong>October</strong>; this<br />

year. However, in real terms, this was a 12.8% contraction was 85.4% higher than the amount approved during the<br />

(See Figure 4). To be noted is that during the period, an same period of 2009. Consequently, the fiscal budget to<br />

average of 9% of the budgeted amounts of Bs. 168.1 billion date comes to Bs. 203.6 billion, that is, 27.7% higher than<br />

was not disbursed. According to the composition of the initially approved fiscal budget (Bs. 159.4 billion). By<br />

expenditures during the January-<strong>October</strong> period of this sectors, these additional credits were distributed as<br />

year, 34.3% in Other Transfers were assigned to follows: 44.1% to Other sectors, 37.3% to Social sectors,<br />

decentralized entities of the Public Administration, 30.4% 12.1% to Productive sectors, and 6.5% to General sectors.<br />

went to Remunerations, 24.4% to Legal Contributions of To be noted in this connection is that, to date this year no<br />

state governments and municipalities, 6.5% to Other additional credits have been approved for the Law of<br />

Special <strong>Economic</strong> Allocations (LAEE - Ley de

Asignaciones Económicas Especiales), nor for the<br />

Allocations to the States (Situado Constitucional), whereas<br />

during the same period of last year 17.3% of the approved<br />

credits had been assigned to these sectors (See Table 5).<br />

(Acumulated to <strong>October</strong>) Million of Bs.<br />

10,000<br />

5,000<br />

SUPERAVIT (+)<br />

0<br />

-5,0001998<br />

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 <strong>2010</strong><br />

-10,000<br />

-15,000<br />

-20,000<br />

-25,000<br />

DEFICIT (-)<br />

-30,000<br />

-35,000<br />

Note: 1/ Calculated as the difference between the Ordinary Revenues<br />

and the Ordinary Expenditures<br />

Source: Ministry of the Popular Power for the Economy and Finances, National Treasury Office<br />

and Own Calculations<br />

TOTAL 2009 20,686<br />

January -<br />

February -<br />

March 100<br />

April 479<br />

Mayo 1,491<br />

June 2,108<br />

July 304<br />

August 2,465<br />

September 5,632<br />

<strong>October</strong> 8,106<br />

TOTAL <strong>2010</strong> 24,743<br />

January -<br />

February 405<br />

March 2,182<br />

April 1,532<br />

Mayo 890<br />

June 3,588<br />

July 265<br />

August 10,219<br />

September 532<br />

<strong>October</strong> 5,131<br />

6<br />

Figure 5<br />

Central Government Fiscal Management 1/<br />

Social<br />

Sectors<br />

Productive<br />

Sectors<br />

3,847<br />

-<br />

-<br />

-<br />

-<br />

220<br />

2,126<br />

230<br />

1,009<br />

46<br />

216<br />

8,032<br />

-<br />

-<br />

3,348<br />

1,975<br />

100<br />

118<br />

48<br />

292<br />

102<br />

2,048<br />

General<br />

Sectors<br />

766<br />

-<br />

393<br />

-<br />

-<br />

-<br />

-<br />

58<br />

-<br />

220<br />

95<br />

4,319<br />

-<br />

33<br />

-<br />

-<br />

-<br />

1,013<br />

500<br />

1,322<br />

1,100<br />

352<br />

Note: 1/ Law of Special <strong>Economic</strong> Allowances.<br />

Source: Official Gazettes of the Bolivarian Republic of Venezuela and Own Calculations<br />

PUBLIC DEBT<br />

The low level of fiscal oil income recorded in the National<br />

Treasury during the first ten months of the year led to the<br />

Central Government’s increased need for further financing.<br />

Consequently, a program of weekly auctions of Treasury<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

Bills 3 was initiated in early February as a result of which a<br />

cumulative total placement of Bs. 14.6 billion was made<br />

during the January-<strong>October</strong> period of this year. This was<br />

1.1 times higher than placements on record in the same<br />

period of the previous year 4 . In terms of maturity, the award<br />

of this type of instrument was carried out as follows: 94.1%<br />

at 91- and 105-days terms, and the remaining 5.9% at<br />

terms of 182 and 364 days. However, these higher<br />

placements had an average yield almost 130 bp below that<br />

of last year to stand at 8.5% 5 .<br />

In addition, a program of weekly auctions of VEBONOS<br />

and TIF 6 was launched in the second week of February.<br />

Consequently, Bs. 31.6 billion were placed during the<br />

January-<strong>October</strong> period, 55.8% more than during the first<br />

ten months of 2009, with<br />

an effective yield of<br />

15.5%, that is 320 bp<br />

LSEA<br />

over the yield on record<br />

during the same period<br />

4,417 1,784 4,289 35,788 of last year. To be noted<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

393 is that 92% of the<br />

-<br />

-<br />

-<br />

-<br />

109<br />

30<br />

209<br />

509<br />

placement was awarded<br />

- -<br />

29 1,740 by auction and the<br />

4,417<br />

-<br />

1,784<br />

-<br />

1,240<br />

637<br />

11,675<br />

1,230 remaining 8% by direct<br />

- -<br />

450 3,924 award.<br />

1/<br />

Table 5<br />

Additional Credits by <strong>Economic</strong> Destiny<br />

Million of Bs.<br />

Other<br />

Sectors<br />

TOTAL<br />

Public Debt Constitutional<br />

Allowances<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

-<br />

38<br />

1,756<br />

29,272<br />

-<br />

-<br />

-<br />

201<br />

3,668<br />

17,507<br />

2,235<br />

3,196<br />

1,109<br />

1,355<br />

5,936<br />

10,173<br />

66,366<br />

-<br />

438<br />

5,530<br />

3,708<br />

4,658<br />

22,226<br />

3,049<br />

15,028<br />

2,843<br />

8,886<br />

Maturities of domestic<br />

public debt in the<br />

January-<strong>October</strong> <strong>2010</strong><br />

period added up to Bs.<br />

17 billion of which 76%<br />

in Treasury Bills and<br />

24% in DPN bonds. As<br />

a result, the net<br />

3 Under the issue approved in Official Gazette N° 39,349 of January 19 of this year,<br />

a maximum circulation at the close of the fiscal year <strong>2010</strong> of Bs. 5.15 billion was<br />

approved.<br />

4 When the oil price was 30% lower than the current price.<br />

5 Consequently reducing not only the financing cost of this instrument but also the<br />

cost of payment of interest of VEBONOS, which are linked to the rate of yield of<br />

Treasury Bills.<br />

6 In the framework of issues approved in Official Gazettes N° 39,362 and 39,392 of<br />

February 5 and March 23 of this year, when the issue of a maximum Bs. 45.7 billion<br />

were approved to finance Public Debt Service and Fiscal Performance.

indebtedness rose by Bs. 29.2 billion for the highest level<br />

since this statistical series became available in 1999 (See<br />

Figure 6), 62.5% higher than the net positive indebtedness<br />

of Bs. 18 billion in the same period of 2009.<br />

30,000<br />

26,000<br />

22,000<br />

18,000<br />

14,000<br />

10,000<br />

6,000<br />

2,000<br />

-2,000<br />

-6,000<br />

-10,000<br />

7<br />

1999<br />

2000<br />

Figure 6<br />

Net Domestic Borrowing Requirement<br />

(DPN Bonds + Treasury Bills) (Acumulated to <strong>October</strong>)<br />

Billions of Bs.<br />

2001<br />

2002<br />

2003<br />

2004<br />

2005<br />

2006<br />

2007<br />

2008<br />

2009<br />

<strong>2010</strong><br />

Source: Central Bank of Venezuela and Own Calculations<br />

The high awards of DPN bonds and Treasury Bills brought<br />

the total stock of debt securities held by the Central<br />

Government at the close of <strong>October</strong>, <strong>2010</strong>, to Bs. 81.1<br />

billion (93.6% of which were in DPN bonds), for a 58.4%<br />

increase in the net debt in circulation at the close of the<br />

year 2009 (Bs. 51.2 billion). The current level of domestic<br />

debt securities in stock represents 30.9% of total monetary<br />

liquidity, the highest amount since <strong>October</strong> 2006, although<br />

still well below the historical maximum of 83% in <strong>October</strong>,<br />

2003.<br />

MONETARY MARKET<br />

The performance of the monetary market to date this year<br />

showed a moderate expansion of money in circulation,<br />

resulting mostly from the domestic economic contraction,<br />

the lesser secondary creation of money by way of credits,<br />

the delivery of dollars by CADIVI at a higher exchange<br />

rate, the sterilization resulting from the various issues of<br />

Bs/US$ Bonds (International Sovereign Bonds and<br />

PETROBONOS), and to a lesser degree, through<br />

mechanisms such as SITME.<br />

In effect, Monetary Liquidity (M2) came to Bs. 262.3 billion<br />

during the week of <strong>October</strong> 29; this was a cumulative<br />

11.4% expansion compared to the close of 2009, and<br />

scarcely more than 140 bp below the 12.9% expansion<br />

during the same period of 2009 (See Figure 7). However,<br />

after discounting the effects of the higher inflation rates<br />

throughout the period, the contraction of M2 continued<br />

during this year. In effect, at the close of the first ten<br />

months of the year, the real contraction stood at 10%, 180<br />

bp over the real decline on record in the same period of<br />

2009 (-8.2%).<br />

54%<br />

46%<br />

38%<br />

30%<br />

22%<br />

14%<br />

6%<br />

-2%<br />

-10%<br />

-18%<br />

2000<br />

Monetary Liquidity<br />

Monetary Base<br />

2001<br />

2002<br />

2003<br />

2004<br />

Figure 7<br />

Liquidity & Monetary Base<br />

% Change Accumulated to <strong>October</strong><br />

2005<br />

2006<br />

2007<br />

2008<br />

2009<br />

<strong>2010</strong><br />

Source: Central Bank of Venezuela and Own Calculations<br />

By components, Money in Circulation (Coins and Bills plus<br />

Sight Deposits) caused the overall nominal development of<br />

liquidity, which grew by a cumulative 20.4%, somewhat<br />

over 1,000 bp over the cumulative increase during the<br />

same period of 2009 7 . At the same time, Quasimoney<br />

(Savings and Term Deposits) showed a cumulative<br />

decrease by 7%, in significant contrast with the 17.4%<br />

increase during the same period of last year (See Figure<br />

8). As a result, the participation of Money in Circulation<br />

rose from 62.4% at the end of <strong>October</strong> 2009 to 71.2% in<br />

the same month of this year. To be noted is that this<br />

participation of Money in Circulation is the highest since<br />

the statistical series became available (December 1968) 8<br />

(See Figure 9).<br />

7 To be noted is the quite different performance of the components of Money in<br />

Circulation. In effect, Sight Deposits grew by a cumulative 26.4%, which explains the<br />

increase of Money in Circulation. However, Coins and Bills declined by a cumulative<br />

6.5%.<br />

8 This performance of Money in Circulation may be reflecting the greater preference<br />

of the public for more liquid instruments in a scenario of high inflation rates and<br />

economic recession.

-10%<br />

-20%<br />

8<br />

50%<br />

40%<br />

30%<br />

20%<br />

10%<br />

0%<br />

Figure 8<br />

Change of Liquidity, Accumulated<br />

(by Components)<br />

Term Deposits<br />

Saving Deposits<br />

Demand Deposits<br />

Cash<br />

Monetary Liquidity<br />

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 <strong>2010</strong><br />

Source: Central Bank of Venezuela and Own Calculations<br />

The Monetary Base or high-powered money reached<br />

Bs. 100.6 billion as of <strong>October</strong> 29, representing a<br />

cumulative growth of barely 1.7% compared to the close of<br />

2009, 60 bp over the cumulative increase in the same<br />

period of last year (1.1%). To be noted is that to date this<br />

year no detailed information on the components of the<br />

Monetary Base has been published.<br />

80%<br />

70%<br />

60%<br />

50%<br />

40%<br />

30%<br />

20%<br />

1990<br />

1991<br />

Figure 9<br />

Money in Circulation (Cash + Demand Deposits)<br />

as percentage of Monetary Liquidity<br />

1992<br />

1993<br />

1994<br />

1995<br />

1996<br />

1997<br />

1998<br />

1999<br />

2000<br />

2001<br />

2002<br />

2003<br />

2004<br />

2005<br />

2006<br />

2007<br />

2008<br />

2009<br />

<strong>2010</strong><br />

Source: Central Bank of Venezuela and Own Calculations<br />

Bank liquidity surpluses came to Bs. 15.5 billion on<br />

average during the fist ten months of the year, which is 3.8<br />

times higher than the average on record for the January-<br />

<strong>October</strong> period of 2009 9 . As a result, liquidity surpluses<br />

over M2 went from 1.9% in the first ten months of 2009 to<br />

6.7% in the same period of this year.<br />

9 To be pointed out is that the strong expansion of surplus liquidity in the banking<br />

system in late 2009 and, to a lesser degree, throughout the current year, was the<br />

result of a lesser increase in loans, as well as of the limits imposed on CDs and<br />

Repos by the Central Bank since December of last year.<br />

Regarding the management of monetary policy, during the<br />

first ten months of the year the BCV showed a more lax<br />

performance than last year with respect to awarding<br />

Certificates of Deposit (CDs) and Repos. This is explained<br />

in part by the limits established on placement of CDs and<br />

Repos (the Central Bank’s main instruments to control<br />

Money in Circulation). In effect, placements of these<br />

absorption instruments during the period came to Bs. 93.6<br />

billion, which was 43.4% lower than during the January-<br />

<strong>October</strong> period of 2009.<br />

Injection operations in an amount of Bs. 27.3 billion were<br />

carried out by means of Purchase of DPN Bonds under<br />

Resale Pact (Reverse Repos) up to <strong>October</strong> at an average<br />

rate of 19.4%, while during the same period of last year<br />

placements were, 1.3 times lower (Bs. 11.7 billion).<br />

Maturities of both CDs and Repos during the January-<br />

<strong>October</strong> period came to Bs. 95.1 billion compared to<br />

Bs. 180 billion during the first ten months of 2009. As a<br />

result, open market operations, both of absorption and<br />

injection, resulted in a slight expansion of liquidity of barely<br />

Bs. 21.4 million (See Figure 10), in contrast with the strong<br />

expansion by Bs. 13.5 billion during the same period of<br />

2009. Given the lower awards of credit instruments by the<br />

BCV together with the decrease by some-what over 200<br />

bp in the average weighted yield of CDs and Repos,<br />

interest paid by the Central Bank during the first ten<br />

months of the year declined by 70.8% compared to the<br />

same period of last year, for a total Bs. 600.6 million.<br />

Figure 10<br />

Net Effect of Open Market Operations<br />

Repos+Certificates of Deposits+Reverse Repos. Million of Bs.<br />

10,000<br />

8,000<br />

6,000<br />

4,000<br />

2,000<br />

0<br />

-2,000<br />

-4,000<br />

-6,000<br />

-8,000<br />

Oct-08<br />

Dec-08<br />

Feb-09<br />

INYECTION<br />

Apr-09<br />

Jun-09<br />

ABSORPTION<br />

Aug-09<br />

Oct-09<br />

Issuance of Bonds (Bs. / US$)<br />

Jun-09: PETROBONO 2011<br />

Oct-09: Bonos Soberanos Internacionales<br />

Oct-09: PETROBONO 2014,2015 y 2016<br />

Aug-10: Bono Soberano Internacional 2022<br />

Oct-10: PETROBONO 2017<br />

Dec-09<br />

Feb-10<br />

Apr-10<br />

Jun-10<br />

Aug-10<br />

Oct-10<br />

Source: Central Bank of Venezuela and Own Calculations

As a result, the stock in circulation of CDs and Repos fell<br />

from Bs. 10.2 billion at the close of 2009 to Bs. 9.3 billion<br />

at the close of <strong>October</strong> of this year. This level is equivalent<br />

to 3.5% of M2, 120 bp less than in the same month of<br />

2009, and represented the lowest on record since May of<br />

2002, when this ratio stood at 2.7%. In addition, this level<br />

was significantly lower than the historical maximum on<br />

record, when this ratio reached 46.2% in April 2006 (See<br />

Figure 11).<br />

16%<br />

14%<br />

12%<br />

10%<br />

9<br />

8%<br />

6%<br />

4%<br />

2%<br />

Oct-08<br />

Dec-08<br />

Feb-09<br />

Figure 11<br />

BCV's Stock of Securities (Cd's+Repos)<br />

as percentage of Monetary Liquidity<br />

Apr-09<br />

Jun-09<br />

Aug-09<br />

Oct-09<br />

Dec-09<br />

Feb-10<br />

Apr-10<br />

Jun-10<br />

Aug-10<br />

Oct-10<br />

Source: Central Bank of Venezuela and Own Calculations<br />

In connection with legal matters, according to Official<br />

Gazette N° 39,538, for the second time this year,<br />

on <strong>October</strong> 26, <strong>2010</strong> the minimum legal reserve<br />

that financial institutions must maintain for the increase<br />

of their deposits with respect to the<br />

Reserves Base (July 14, 2006) was reduced from<br />

20% to 17%. This lower reserve entailed freeing<br />

bank funds by approximately Bs. 9.6 billion.<br />

INTEREST RATES<br />

To date this year, interest rates have continued<br />

their downward trend recorded throughout 2009. In<br />

effect, the nominal active rate of Commercial and<br />

Universal Banks averaged 18.3% in the first ten<br />

months of the year, equivalent to a decline by 262<br />

bp compared to the average rate during the same period of<br />

2009, and represented the lowest on record since the<br />

same period of 2007. By economic destination, the rates<br />

charged declined for all items, particularly Mortgage<br />

Loans 10 (-537 bp compared to the January-<strong>October</strong><br />

average of 2009), Communications (-325 bp), and<br />

Commerce (-278 bp) (See Table 6).<br />

The Savings Deposits rate reached an average 12.6%<br />

(vs. 13.6% during the same period of 2009), while the 90day<br />

Fixed Term Deposits rate declined by 100 bp for an<br />

average 14.7% during the first ten months of the year, both<br />

barely higher than the regulatory minimums of 12.5% and<br />

14.5% respectively. Consequently, the relative financial<br />

margin stood at 19.3% on average for the period, that is<br />

320 bp below that of the January-<strong>October</strong> period of 2009<br />

(22.5%), which also is the lowest level for a similar period<br />

since 1993 (See Figure 12).<br />

As a result of the high rates of inflation of the period, the<br />

average lending and borrowing rates continued to be<br />

negative for the fifth year running in the case of loans, and<br />

for the ninth consecutive year in the case of the deposits<br />

with highest yields. In effect, the real lending rate was<br />

-7.7% (-5.6% on average for the first ten months of 2009),<br />

Table 6<br />

Commercial and Universal Banks<br />

Average Interest Rates by <strong>Economic</strong> Destination<br />

Average until <strong>October</strong><br />

2008 2009 <strong>2010</strong><br />

AVERAGE LENDING RATE 23.4<br />

21.0<br />

18.3<br />

Agriculture 13.4<br />

12.6<br />

12.3<br />

Industrial 22.2<br />

19.6<br />

17.5<br />

Commerce 25.8<br />

23.9<br />

21.1<br />

Services 24.7<br />

23.5<br />

22.0<br />

Mortgage 21.3<br />

16.3<br />

11.0<br />

Transportation 26.3<br />

22.8<br />

22.2<br />

Tourism 19.5<br />

17.7<br />

15.5<br />

Communication 25.7<br />

23.4<br />

20.2<br />

Vehicles 26.8<br />

25.2<br />

22.8<br />

Other Private Sectors 24.8<br />

23.7<br />

22.5<br />

Mining and Quarries 26.8<br />

23.2<br />

20.9<br />

Electricity and Water 26.1<br />

24.2<br />

22.5<br />

Credit Cards 31.2<br />

30.0<br />

28.6<br />

Source: Central Bank of Venezuela and Own Calculations<br />

whereas the real borrowing rate came to -10.4% (-9.2% in<br />

the same period of last year). It is important to point out<br />

that negative real interest rates usually stimulate demand<br />

for credit and the substitution of savings by consumption<br />

10 To be pointed out is that some of the Sectors subject to measures of preferred<br />

rates, like Mortgage and Farming, stayed at the lowest level of the classification of<br />

asset yields by economic destination.

(in anticipation of future prices higher than the yields of<br />

savings).<br />

%<br />

48<br />

44<br />

40<br />

36<br />

32<br />

28<br />

24<br />

20<br />

16<br />

12<br />

10<br />

1990<br />

1992<br />

REAL SECTOR<br />

Figure 12<br />

Financial Gap<br />

Commercial and Universal Banks. Average to <strong>October</strong><br />

1994<br />

1996<br />

1998<br />

2000<br />

2002<br />

2004<br />

2006<br />

2008<br />

<strong>2010</strong><br />

Source: Central Bank of Venezuela and Own Calculations<br />

The oil product during the third quarter of the current year<br />

came to -2.1%, similar to the preceding quarter, but 750<br />

basis points less than the decline during the same period<br />

of 2009. This result was recorded in spite of the slight<br />

20,000 b/d (-0.9%) drop in oil production and of the 5.8%<br />

higher average price of the Venezuelan oil export basket.<br />

Figure 13<br />

Absolute deviation of Non Oil GDP by <strong>Economic</strong> Activity<br />

with respect to Total Non Oil GDP<br />

Government General<br />

Services<br />

Social and Common<br />

Services<br />

Real Estate and Services<br />

provided<br />

Finance & Insurance<br />

Mining<br />

12.0%<br />

8.0%<br />

4.0%<br />

0.0%<br />

-4.0%<br />

-8.0%<br />

-12.0%<br />

Manufacturing<br />

Electricity & Water<br />

Construction<br />

Commerce & Repair<br />

Services<br />

Transportation &<br />

Warehousing<br />

The Central Bank (BCV) reported that the Gross Domestic<br />

Communications<br />

Product (GDP) had declined by 0.4% in the third quarter of<br />

Non Oil GDP by <strong>Economic</strong> Activity Total Non Oil GDP<br />

<strong>2010</strong> when compared with the same period of 2009,<br />

Source: Central Bank of Venezuela and Own Calculations<br />

significantly less than the 1.9% decline of the second On the other hand, the non-oil activity fell by merely 0.2%,<br />

quarter and 420 basis points less than the reduction for the lowest decline since the second quarter of 2009.<br />

registered in that same period of last year. This means that The rate of decline has decelerated considerably from the<br />

the Venezuelan economy was in decline for the sixth high -4.9% of the first quarter of this year. An analysis of<br />

consecutive quarter. The GDP fall during the first nine the decline by type of economic activity shows that the<br />

months of <strong>2010</strong> reached 2.4%.<br />

economic activity fell in most of the sectors, particularly in<br />

Table 7 Mining (-10.6%), Construction (-7.9%) and -<br />

Gross Domestic Product 7.2% in Electricity. In the case of Construction<br />

Third Quarter (Annual % Change) the rate of decline was the highest since the<br />

fourth quarter of 2003. Communications,<br />

Communications<br />

Government General Services<br />

2008<br />

13.9<br />

4.1<br />

2009<br />

11.8<br />

2.4<br />

<strong>2010</strong><br />

9.4<br />

3.2<br />

Government Services and Transportation<br />

increased by 9.4%, 3.2% and 2.7%<br />

Transportation & Warehousing<br />

Manufacturing<br />

0.5<br />

-0.3<br />

-10.7<br />

-9.1<br />

2.7<br />

0.1 respectively. The growth of the Transportation<br />

Social and Common Services<br />

Real Estate and Services provided<br />

Non Oil Sector<br />

9.6<br />

1.6<br />

3.9<br />

3.8<br />

-2.9<br />

-3.1<br />

0.0<br />

-0.1<br />

-0.2<br />

sector was in notable contrast to the 10.7%<br />

drop in the same period of 2009 (See Table<br />

TOTAL 3.8 -4.6 -0.4 7). Figure 13 allows the differences in<br />

Others absolute terms between the non-oil activity as<br />

a whole and its component sectors.<br />

1/<br />

At 1997 Prices<br />

6.4 0.2 -1.0<br />

Oil Sector 4.4 -9.6 -2.1<br />

Commerce & Repair Services 1.9 -11.0 -4.4<br />

Finance & Insurance -5.1 -3.6 -5.0<br />

Electricity & Water 9.5 4.0 -7.8<br />

Construction 3.7 1.8 -7.9<br />

Mining 0.9 -18.3 -10.6<br />

Note: The activities were ordered in accordance with the highest growths recorded in the third quarter of <strong>2010</strong>. 1/ Private<br />

Agriculture, Restaurants & Hotels and Public Activities.<br />

Source: Central Bank of Venezuela and Own Calculations<br />

On an institutional basis, the BCV reported<br />

that the product of the public sector fell for the<br />

fifth consecutive quarter, although only by<br />

0.1%, 140 basis points less than in the<br />

preceding quarter and 30 basis points lower than in the

same quarter of the previous year. In the case of the<br />

private sector, it fell 0.7% compared to the same period of<br />

2009, for the lowest such fall in the last six quarters.<br />

The notable decrease in the rate of decline of the non-oil<br />

activity can be explained in part by the performance of the<br />

Aggregate Internal Demand (AID) which grew by 4.1%<br />

after falling for five consecutive quarters, in contrast with<br />

the 0.9% fall in the preceding quarter and with the 10.9%<br />

decline in the same quarter of last year. The rise in the<br />

Aggregate Internal Demand is the result of the increases in<br />

the Gross Formation of Fixed Capital and of Government<br />

Consumption.<br />

Private Consumption represented 57,1% of AID but<br />

declined by 2.1% for 30 basis points less than the<br />

contraction in the second quarter and 240 basis points<br />

lower than the decline in the third quarter of 2009. The<br />

Gross Formation of Fixed Capital represents 25% of AID<br />

but after the five consecutive quarters of decrease it rose<br />

by 4.4% while in the same period of 2009 it dropped by<br />

13.6%. Government Consumption continued to rise,<br />

currently at the highest rate in the last seven quarters<br />

when it reached 3.4%, the highest increase from fourth<br />

quarter in 2008.<br />

On the other hand, External Demand (ED) contracted by<br />

17.6%, down to its minimum in real terms and – excluding<br />

the first quarter of 2003 – the lowest level on record since<br />

this series became available in 1998 (See Table 8).<br />

Table 8<br />

Aggregate Demand and Gross Domestic Product<br />

Third Quarter (Annual % Change)<br />

2009 <strong>2010</strong><br />

1. Final Consumption -3.3% -1.1%<br />

Public Sector 2.6% 3.4%<br />

Private Sector -4.5% -2.1%<br />

2. Gross Fixed Capital Formation -13.6% 4.4%<br />

3. Domestic Aggregate Demand 1/<br />

At 1997 Prices<br />

-10.9% 4.1%<br />

4. Exports -15.0% -17.6%<br />

5. Minus: Imports -25.5% 6.3%<br />

6. Gross Domestic Product (3+4+5)<br />

Note: 1/ includes the variation of stocks.<br />

Source: Central Bank of Venezuela and Own Calculations<br />

-4.6% -0.4%<br />

11<br />

LABOR MARKET<br />

The National Statistical Institute reported that the average<br />

rate of un-employment in the first nine months of <strong>2010</strong> was<br />

8.8%, 80 basis points higher than in the same period of<br />

2009 (8%) and the highest since the comparable period of<br />

2007.<br />

This result is due to the 10.8% increase in the unemployed<br />

population during the first nine months of this year, nearly<br />

400 basis points higher than the 6.9% increase during the<br />

same period of last year and the highest since 2003. The<br />

average number of unemployed persons during the current<br />

year came to 1,146,170 while the economically active<br />

population only increased by 1.6% during the same period.<br />

On the other hand, the average number of employed<br />

persons during the first nine months of this year rose only<br />

by 0.8%, 130 basis points below the increase recorded in<br />

the same period of 2009 and the lowest since the same<br />

period in 2003, indicating the depth of the economic<br />

recession.<br />

Employment in the public sector during the same period<br />

increased merely by 59,391 (2.6%) for the lowest rise<br />

since 2003 and 530 basis points less than the growth<br />

recorded in the first nine months of 2009. Employment in<br />

the private sector increased by a mere 38,048 (0.4%), 40<br />

basis points less than the increase of the first nine months<br />

of 2009 (0.8%), again the lowest since 2003. The<br />

participation of the public sector in the total employed<br />

population has grown every year for the last seven years,<br />

moving from 14.1% in the first nine months of 2003 to<br />

19.3% in the same period of the present year.<br />

The informal sector of the economy provided the strongest<br />

growth within the employed population, for a 1.6%<br />

increase compared to the same period of 2009. During the<br />

same period employment in the formal sector of the<br />

economy only increased by 0.2%. However, the

participation in the formal sector remained relatively stable,<br />

falling only by 30 basis points - to a total of 56.1%<br />

compared again to the same nine month period of 2009.<br />

The Central Bank reported that the Index of<br />

Remunerations in the formal sector of the economy for the<br />

third quarter of the current year increased by 21.7%,<br />

similar to the second quarter. However, after adjusting for<br />

inflation the Index in real terms discloses a 6.3% fall in<br />

average remunerations which have declined for eleven<br />

consecutive quarters, the level registered in the third<br />

quarter of the current year being the lowest ever in real<br />

terms for any third quarter.<br />

25%<br />

20%<br />

15%<br />

10%<br />

5%<br />

0%<br />

-5%<br />

-10%<br />

-15%<br />

-20%<br />

-25%<br />

-30%<br />

12<br />

III-02<br />

I03<br />

III-03<br />

I04<br />

III-04<br />

I05<br />

III-05<br />

I06<br />

III-06<br />

I07<br />

III-07<br />

I08<br />

Figure 14<br />

Wage Index<br />

Annual % Change<br />

III-08<br />

I09<br />

General<br />

Private<br />

Public<br />

III-09<br />

I10<br />

III-10<br />

Source: Central Bank of Venezuela and Own Calculations<br />

The highest increase of the Remunerations Index took<br />

place in the private sector, by 27.4%. However, in real<br />

terms this adjustment translates into a negative 1.8%.<br />

Remunerations in the public sector were up 9.9%, for the<br />

lowest rate of increase since the third quarter of 2003.<br />

After adjusting for inflation, it is found that in this case<br />

there has been a year-to-year quarterly decline for the<br />

eighth consecutive quarter. Specifically, the Index fell by<br />

15.3% in real terms in the third quarter of <strong>2010</strong> compared<br />

to the same period of 2009 (See Figure 14). When<br />

remunerations are compared between the public and the<br />

private sector, it is found that remunerations in the public<br />

sector continue at higher levels than in the private sector. It<br />

should be noted however that after nearly a decade (1998-<br />

2007) of higher salary increases in the public sector this<br />

tendency started to revert at the end of 2007. At that time<br />

average remunerations in the public sector were 38.3%<br />

higher than in the private sector, but the difference is now<br />

down to 11.4%.<br />

PRICES<br />

In <strong>October</strong> <strong>2010</strong> the National Consumer Price Index (CPI)<br />

accelerated after the slowdown recorded in September. In<br />

<strong>October</strong> <strong>2010</strong> the CPI rose by 1.5%, i.e. by 40 basis points<br />

over September, although it was 40 basis points lower<br />

than in <strong>October</strong> 2009. On a year-to-date basis, inflation<br />

rose by 23%, 270 basis points above the level recorded in<br />

the first ten months of 2009. A number of factors<br />

contributed to inflation during the first ten months of <strong>2010</strong>:<br />

the modification of the exchange rate, lower supply of local<br />

products, a slower rate of CADIVI authorizations for the<br />

acquisition of foreign exchange, and the eventual complete<br />

shutdown of the parallel exchange market, etc.<br />

The rate of inflation speeded up in all of the eleven cities<br />

included in the monthly survey. On a year-to-date basis, in<br />

only three cities was inflation found to exceed the national<br />

average, namely Valencia (24.4%), Caracas (23.7%) and<br />

Maturin (23.4%). The lowest prices were found in San<br />

Cristóbal and Mérida (20.5% and 22.1%) respectively, but<br />

never much below the national average of 23%. Figure 15<br />

shows the differences between the rates of inflation in the<br />

various cities compared with the national average.<br />

Figure 15<br />

Absolute deviation of cumulated inflation up to <strong>October</strong><br />

with respect to the national average<br />

National Rest<br />

San Cristóbal<br />

Maturín<br />

Mérida<br />

Maracaibo<br />

Caracas<br />

1.5%<br />

0.9%<br />

0.3%<br />

-0.3%<br />

-0.9%<br />

-1.5%<br />

-2.1%<br />

-2.7%<br />

Maracay<br />

Ciudad Guayana<br />

Valencia<br />

Barquisimeto<br />

Pto La Cruz / Barcelona<br />

Cumulated Inflation by Cities National Cumulated Inflation<br />

Source: Central Bank of Venezuela and Own Calculations

Inflation increased in six of the thirteen groups considered<br />

for the monthly study. The highest rates of increase<br />

occurred in Alcoholic Beverages and Tobacco (2.9% vs.<br />

1%), Food and Non-Alcoholic Beverages (1.6% vs. 0.3%)<br />

and Home Rentals (1.1 vs. 0.8%). During the first ten<br />

months of the current year the prices of five of the 13 items<br />

used for the Index increased at higher rates than the<br />

national average. These items represent about 54% of the<br />

total, as follows: Alcoholic Beverages and Tobacco<br />

(33.6%), Food and Non-Alcoholic Beverages (29.2%),<br />

Entertainment and Culture (25.6%), Diverse Goods and<br />

Services (24.4%) and Restaurants and Hotels (23.7%)<br />

(See Table 9).<br />

Core Inflation, which excludes seasonal changes and<br />

price-controlled items, increased by 1.7% in <strong>October</strong> <strong>2010</strong>,<br />

for a total increase during the first ten months of 22.6%,<br />

only 40 basis points below the 23% of the National Index.<br />

To be noted is that during the same period of 2009 the<br />

National Inflation Index was considerably higher – by 410<br />

basis points - than the Core Inflation.<br />

The CPI in the Caracas area rose by 1.5% in <strong>October</strong> after<br />

five consecutive months of deceleration, for an increase of<br />

20 basis points over September and reaching 23.7% for<br />

the first ten months of the year and 70 basis points above<br />

the level in the same period of last year.<br />

Five of the 13 groups used to compile the price index had<br />

higher prices than the national index of 1.5%, namely<br />

13<br />

Alcoholic Beverages and Tobacco (2.4%), Various Goods<br />

and Services (2.1%), Food and Non-Alcoholic Beverages<br />

(1.9%), Clothing and Footwear (1.8%), and Health (1.6%).<br />

It is of interest that the increase of prices for Food and<br />

Non-Alcoholic Beverages registered in <strong>October</strong> followed a<br />

0.1% price decrease in September.<br />

Core Inflation at 1.6% exceeded the national CPI for the<br />

sixth consecutive month, although barely 10 basis points<br />

over the level of September. The rates of Core Inflation<br />

have been gradually approaching the national index. In<br />

<strong>October</strong> <strong>2010</strong> the difference between the CPI and the Core<br />

Inflation was down to 60 basis points, compared to 662<br />

basis points of difference in <strong>October</strong> 2009.<br />

26%<br />

24%<br />

22%<br />

20%<br />

18%<br />

16%<br />

14%<br />

12%<br />

10%<br />

Figure 16<br />

CPI-Metropolitan Area of Caracas by Income levels<br />

% Change Accumulated to <strong>October</strong><br />

2003<br />

2004<br />

2005<br />

Level I<br />

Level IV<br />

2006<br />

Table 9<br />

Inflation by Sector<br />

% Change Accumulated to <strong>October</strong><br />

National Barquisimeto Barcelona Caracas Ciudad Guayana Maracaibo Maracay Maturín Mérida San Cristóbal Valencia Rest 1/<br />

GENERAL INDEX 23.0 22.4 22.8 23.7 22.5 23.0 22.8 23.4 22.1 20.5 24.4 22.9<br />

Foodstuffs & Non-Alcoholic Beverages 29.2 27.0 27.8 30.1 28.5 30.3 30.2 30.1 30.2 26.7 30.9 28.8<br />

Alcoholic Beverages & Tobacco 33.6 34.8 34.3 39.3 33.3 34.4 34.2 33.1 35.2 31.9 31.6 31.5<br />

Clothing & Footwear 12.1 12.7 11.2 14.7 10.5 13.6 10.1 11.9 13.3 10.2 16.0 11.0<br />

Housing Rent 9.7 9.6 12.3 9.7 11.0 9.2 9.7 10.6 12.0 11.7 11.5 9.3<br />

House Services (excluding Phone Services) 8.3 9.9 10.3 4.7 10.1 -0.3 13.8 13.3 11.5 15.2 13.7 11.1<br />

Home Equipment 20.9 19.6 20.4 26.2 19.7 24.8 19.6 18.7 14.9 17.3 18.2 18.6<br />

Health 21.6 18.4 24.0 22.3 21.5 26.8 18.4 29.4 28.0 18.8 23.3 18.9<br />

Transportation 22.7 25.4 26.6 24.1 21.8 16.3 25.4 19.6 23.8 20.6 29.8 22.1<br />

Communications 5.9 6.7 6.4 6.0 6.2 6.5 5.4 6.8 5.1 4.6 5.9 5.5<br />

Culture 25.6 28.5 19.1 24.3 19.6 20.4 20.5 19.4 23.1 17.3 21.8 29.5<br />

Education Services 21.7 20.3 20.3 23.9 24.0 24.1 17.9 19.5 20.9 20.0 19.7 18.9<br />

Restaurants & Hotels 23.7 21.0 21.0 25.5 18.4 22.4 19.7 25.4 21.2 22.1 22.5 24.4<br />

Other Good and Services 24.4 23.6 25.7 25.3 24.6 26.1 24.8 25.0 25.7 20.4 25.1 23.4<br />

Note: 1/ Include a representative sample of 74 localities (cities small medians and, as well as rural areas).<br />

Source: Central Bank of Venezuela and Own Calculations<br />

2007<br />

2008<br />

2009<br />

<strong>2010</strong><br />

Note: Levels I and IV correspond to households<br />

with lower and higher income, respectively.<br />

Source: Central Bank of Venezuela and Own Calculations<br />

In terms of level of income, the key item is Food and Non-<br />

Alcoholic Beverages which is not only the principal<br />

component of the price index but also causes the greatest<br />

impact on the low-income sectors. Inflation in <strong>October</strong> on<br />

Level 1 (the quartile of homes with the lowest incomes)<br />

was 1.8% while the effect on Level 4 the quartile of homes

with the highest incomes was only 1.4%. Cumulative<br />

inflation during the first ten months in Level 1 was 22.4%,<br />

223 basis points higher than the same quarter in 2009 and<br />

the highest rate of year-to-date inflation since 2008, when<br />

it reached 24.9% (See Figure 16). On the other hand, the<br />

effect of inflation on Level 4 for the ten-month period of<br />

<strong>2010</strong> was only 20.6%, 170 basis points lower than during<br />

the same period of 2009.<br />

The Diversity Index measures<br />

the availability of certain brands,<br />

forms of presentation or varieties<br />

of merchandise in Caracas.<br />

14<br />

In <strong>October</strong> of the current year this index came to a level of<br />

161, indicating only a minor improvement of 3.9% in<br />

diversity since the close of 2009 and well below the 8.8%<br />

increase in diversity in the first ten months of 2009.<br />

Finally, the government increased the prices for sale to the<br />

public of a number of price-controlled items. The principal<br />

changes are listed on Table 10.<br />

Date Official Gazettes Measures<br />

November 5, <strong>2010</strong><br />

Source: Official Gazettes of the Bolivarian Republic of Venezuela<br />

Table 10<br />

Principal price adjustments in goods under control<br />

N° 39,546<br />

NEW LEGISLATION IN THE ECONOMIC AND SECTORIAL FIELD<br />

MONTH OF OCTOBER <strong>2010</strong><br />

* An upward adjustment in the Maximum Sale Price of the<br />

following goods: White Rice Type I, II and III (1 kg) (average<br />

21.1%) and corn flour (1 kg) (23.9%).<br />

OFFICIAL GAZETTE N° DATE SUMMARY<br />

39.522 10/01/10 Regulations of Foreign Exchange transactions.<br />

39.526 10/07/10 Regulation extending by 30 banking days the period during which financial institutions are allowed to charge commissions, fees, etc.<br />

39.527 10/08/10<br />

Law approving a joint venture between Venezuela and China to develop Block Junin 4 of the Orinoco Oil Belt Law approving a joint venture between<br />

Venezuela and China to develop Block Junin 4 of the Orinoco Oil Belt.<br />

39.533 10/19/10 Regulation of mandatory deposits (encaje legal) in the Central Bank.<br />

39.538 10/26/10 Regulation of mandatory deposits in the Central Bank.<br />

Source: Official Gazettes of the Bolivarian Republic of Venezuela<br />

This bulletin has been prepared by the <strong>Economic</strong> Research Management, by <strong>Mercantil</strong> C.A., (<strong>Banco</strong> Universal), coordinated by<br />

Francisco Vivancos Cabello.<br />

<strong>Economic</strong> Research team: Inés Fasanaro, Andreas Faust, Gema Murillo, Carmen J. Noguera, Leonardo Vera.<br />

The opinions expressed in this bulletin are responsibility of the authors and do not necessarily express the opinion of the institution.<br />

Edificio <strong>Mercantil</strong>, Av. Andrés Bello, N° 1-Zip Code N°789 - Caracas 1010A. Venezuela.<br />

Legal Deposit: 83-0181. Vol 32, N° 07.

15<br />

ECONOMIC INDICATORS 2007 2008 2009 Jul-10 Aug-10 Sep-10 Oct-10 Nov-10 % Change % Change<br />

EXTERNAL SECTOR Accumulated 12 Months<br />

Volume of Production of Crude (thousands of barrels) 2,413<br />

2,353<br />

2,181<br />

2,195<br />

2,200<br />

2,190<br />

2,200<br />

2,180<br />

-1.8% -1.8%<br />

Price West Texas Intermediate (WTI) (US$/bl) 72.2<br />

99.9<br />

61.7<br />

76.1 77.0 75.2 81.9 84.1 12.8 % 7.7 %<br />

Venezuelan Oil Basket Price (US$/bl) 64.6<br />

86.4<br />

56.9<br />

67.3 68.9 68.0 74.3 77.0 11.6 % 6.3 %<br />

OPEC Price (US$/bl) 69.1<br />

94.4<br />

60.7<br />

72.4 74.3 74.4 79.8 82.6 11.7% 8.4%<br />

Non Traditional Exports (Million of US$) 16,964<br />

5,426<br />

2,380<br />

200<br />

150 221 -3.5% -3.5%<br />

Imports 1/ (Million of US$) 41,911 45,128 36,908<br />

2,942<br />

2,998<br />

3,075<br />

18.1% -6.2%<br />

Gross International Reserves (Million of US$) 33,477 42,299 35,000 27,389 28,234 28,618 29,033<br />

27,135 -22.5% -16.6%<br />

Priority Imports Exchange Rate (Bs./US$) 2.15<br />

2.60<br />

2.60<br />

2.60<br />

2.60<br />

2.60<br />

20.9% 20.9%<br />

Non-Priority Imports "Oil Dollar" Exchange Rate (Bs./US$) 2.15<br />

2.15<br />

2.15<br />

4.30<br />

4.30<br />

4.30<br />

4.30<br />

4.30<br />

REAL SECTOR<br />

Sales Volume Index 196.0<br />

216.6<br />

192.6<br />

171.6<br />

174.1<br />

174.6<br />

-30.3% -5.3%<br />

Wholesale 140.5<br />

143.3<br />

122.1<br />

131.9<br />

136.6<br />

143.0<br />

18.7% 13.4%<br />

Detail 233.2<br />

265.7<br />

239.8<br />

198.3<br />

199.2<br />

195.8<br />

-42.0% -12.3%<br />

Automotive Vehicles 245.3<br />

189.8<br />

127.4<br />

75.4<br />

80.1<br />

79.9<br />

-30.5% -14.8%<br />

Parts, Pieces & Accessories of Automotive Vehicles 142.1<br />

171.7<br />

149.5<br />

144.6<br />

163.7<br />

150.2<br />

-0.5% 2.6%<br />

Fuels for Automotive Vehicles 116.3<br />

128.9<br />

180.7<br />

167.4<br />

169.5<br />

167.0<br />

-42.1% 10.1%<br />

Foods, Beverages & Tobacco in Non-Specialized Storehouses 312.4<br />

337.0<br />

324.2<br />

260.6<br />

246.7<br />

237.0<br />

-43.5% -19.8%<br />

Other Products in Non-Specialized Storehouses 105.6<br />

159.1<br />

247.7<br />

176.8<br />

175.6<br />

164.6<br />

-54.2% -24.2%<br />

Foods, Beverages & Tobacco in Specialized Storehouses 229.6<br />

248.7<br />

217.4<br />

201.9<br />

208.0<br />

195.6<br />

-3.6% -9.5%<br />

Pharmaceutical & Medicinal Products, Cosmetic & Toiletries 302.4<br />

401.7<br />

409.3<br />

303.7<br />

307.6<br />

294.1<br />

-23.1% -30.2%<br />

Textile Products, Apparel, Footwear & Leather's Articles 327.2<br />

490.8<br />

394.4<br />

316.6<br />

332.8<br />

360.3<br />

-55.9% -4.6%<br />

Articles & Equipment of Domestic Use 433.5<br />

608.1<br />

490.7<br />

379.6<br />

408.9<br />

308.2<br />

-60.6% -30.8%<br />

Articles of Ironworks, Paintings & Products of Glass 97.7<br />

107.2<br />

99.8<br />

82.3<br />

82.8<br />

92.6<br />

2.3% -13.4%<br />

Other Products in Specialized Storehouses 83.5<br />

85.8<br />

90.0<br />

100.0<br />

102.1<br />

110.6<br />

-31.6% 20.0%<br />

Volume Index of Private Manufacturing Industry 123.9<br />

125.6<br />

110.7<br />

109.7<br />

117.0<br />

118.1<br />

28.5 % 3.2 %<br />

MONETARY AGGREGATES<br />

Liquidity (M2) 153,225 194,275 235,401 257,084 258,811 261,114 262,272 278.006 *****/ 18.1% 20.0%<br />

Currency & Demand Deposits (M1) 98,069 124,036 155,269 180,929 183,150 184,581 187,281 198.405 *****/ 27.8% 33.4%<br />

Monetary Base 64,177 83,787 98,903 107.264 */ 104.679 **/ 107.505 ***/ 100.567 ****/ 108.272 *****/ 9.5% 22.4%<br />

Net International Reserves 70,524 89,048 74,544<br />

Net National Treasury Agency (13,879) (9,474) (3,488)<br />

PDVSA (1,181)<br />

(351) (6,091)<br />

Other Net Public Sector Accounts (10,132) 2,624<br />

919<br />

Financial Sector 2<br />

161<br />

3<br />

Credit Instruments Placed by BCV (12,663) (23,041) (7,563)<br />

Capital & Other Net Accounts 13,989 17,477 38,354<br />

MONETARY MARKET<br />

Awarded Repos 27,531<br />

795 12,190<br />

3,600 3,118 2,481 2,910 1,909 149.2 % 22.5 %<br />

Awarded CDs 281,332 179,520 168,813<br />

6,433 6,525 6,669 4,887 6,051 -59.0% -20.0%<br />

Awarded Repos+CDs (Average Weekly) 5,940<br />

3,468<br />

3,481<br />

2,389 2,192 2,080 2,052 1,895 -36.9% 3.9%<br />

Purchases DPN (Average Weekly) 101<br />

586<br />

461<br />

872 998 798 839 977 59.7% -7.1%<br />

Outstanding Repos -<br />

-<br />

2,653<br />

3,204 3,284 2,829 2,725 3,130 18.0% 61.9%<br />

Outstanding CDs 12,613 22,715<br />

7,584<br />

9,318 7,887 8,876 6,572 6,653 -12.3% -25.3%<br />

Average Effective Returns Repos 7.70<br />

6.50<br />

6.27<br />

6.1 6.3 6.0 6.4 6.1 (3.9)<br />

0.1<br />

Average Effective Returns CDs 9.79<br />

12.34<br />

8.97<br />

6.3 6.4 6.2 6.3 6.2 (4.8) (17.1)<br />

COMMERCIAL & UNIVERSAL BANKS<br />

Credit Portfolio 102,542 101,171 139,067 150,307 155,058 156,211 158,679 161.471 ******/ 16.1 % 13.8 %<br />

Investments 47,192 59,049 59,445 81,855 80,291 87,831 58,213 59.283 ******/ -0.3% -13.0%<br />

Total Deposits 141,969 175,984 184,977 218,575 221,043 222,576 213,338 208.561 ******/ 12.7% 7.6%<br />

Demand Deposits 88,210 106,763 115,498 151,607 154,109 154,748 151,135 146.534 ******/ 26.9% 23.5%<br />

Saving Deposits 35,289 45,777 47,996 53,755 53,399 54,081 50,550 50.889 ******/ 6.0% 6.1%<br />

Term Deposits 18,469 23,444 21,483 13,213 13,534 13,747 11,653 11.138 ******/ -48.2% -59.1%<br />

INTEREST RATES<br />

Overnight (Min - Max) 0,1-121,0 0,01-56,0 0,01-38,0 0,2-3,5 0,1-10,0 0,5-20,0 0,1-18,0 3,0-16,0 - -<br />

Overnight (Average) 7.74<br />

10.15<br />

9.30<br />

2.16 2.59 10.09 12.83 11.53 (60)<br />

(728)<br />

Loans (6 Main Banks) 16.77<br />

22.77<br />

20.61<br />

17.73 17.97 17.43 17.70 18,02 *****/ (92)<br />

(82)<br />

90 Days Deposits (6 Main Banks) 10.89<br />

16.55<br />

15.57<br />

14.95 14.58 14.77 15.05 14,91 *****/ (9)<br />

(34)<br />

Libor 90 Days 5.26<br />

2.79<br />

0.65<br />

0.45 0.30 0.29 0.29 0.30 5<br />

4<br />

CENTRAL GOVERNMENT 2/<br />

Ordinary Revenues 141,333 166,098 151,525 10,410 12,923 17,243 11,973<br />

19,206 16.3 % 96.2 %<br />

Oil Ordinary Revenues 71,569 82,432 53,231<br />

2,524<br />

6,103<br />

7,376<br />

1,697<br />

9,445<br />

1.1% 356.7%<br />

Tax Income 19,945 17,834 12,944<br />

574<br />

783<br />

856<br />

1,059<br />

775 -17.8% -13.7%<br />

Royalties 46,093 60,298 35,987<br />

1,107<br />

4,501<br />

3,585<br />

522<br />

8,484<br />

24.3% 624.8%<br />