Kalman Filtering Tutorial

Kalman Filtering Tutorial

Kalman Filtering Tutorial

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

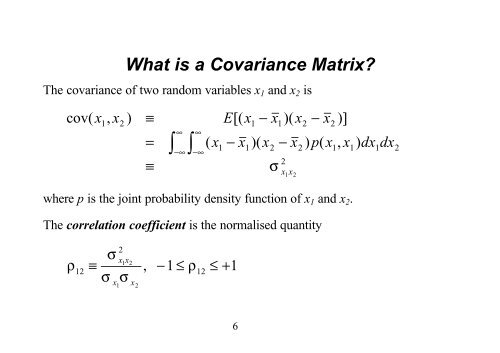

What is a Covariance Matrix?<br />

The covariance of two random variables x1 and x2 is<br />

cov( x , x ) ≡ E[( x − x )( x − x )]<br />

1 2 1 1 2 2<br />

∞ ∞<br />

= ( x − x )( x − x ) p( x , x ) dx dx<br />

≡<br />

∫<br />

−∞<br />

∫<br />

−∞<br />

1 1 2 2 1 1 1 2<br />

where p is the joint probability density function of x1 and x2.<br />

6<br />

σ<br />

2<br />

x x<br />

The correlation coefficient is the normalised quantity<br />

ρ<br />

12<br />

2<br />

σ x1x2 ≡ ,<br />

−1 ≤ ρ12<br />

≤ + 1<br />

σ σ<br />

x x<br />

1 2<br />

1 2